Economy

Nominal Income Targeting and Measurement Issues

Nominal GDP targeting has been advocated in a recent Joint Economic Committee report “Stable Monetary Policy to Connect More Americans to Work”.

The best anchor for monetary policy decisions is nominal income or nominal spending—the amount of money people receive or pay out, which more or less equal out economy-wide. Under an ideal monetary regime, spending should not be too scarce (characterized by low investment and employment), but nor should it be too plentiful (characterized by high and increasing inflation). While this balance may be easier to imagine than to achieve, this report argues that stabilizing general expectations about the level of nominal income or nominal spending in the economy best allows the private sector to value individual goods and services in the context of that anchored expectation, and build long-term contracts with a reasonable degree of certainty. This target could also be understood as steady growth in the money supply, adjusted for the private sector’s ability to circulate that money supply faster or slower.

One challenge to implementation is the relatively large revisions in the growth rate of this variable (and don’t get me started on the level). Here’s an example from our last recession.

Figure 1: Q/Q nominal GDP growth, SAAR, from various vintages. NBER defined recession dates shaded gray. Source: ALFRED.

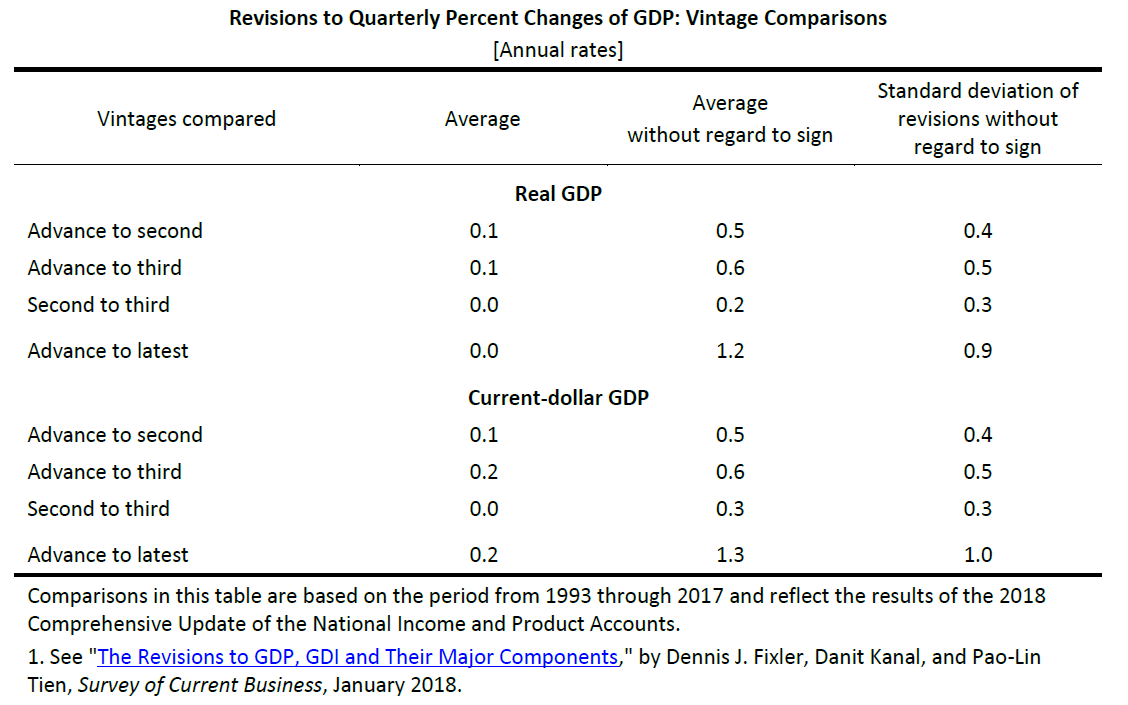

How big are the revisions? The BEA provides a detailed description. This table summarizes the results.

The standard deviation of revisions going from Advance to Latest is one percent (annualized), mean absolute revision is 1.3 percent. Now, the Latest Vintage might not be entirely relevant for policy, so lets look at Advance to Third revision standard deviation of 0.5 percent (0.6 percent mean absolute).

Compare against the personal consumption expenditure deflator, at the monthly — not quarterly — frequency; the mean absolute revision is 0.5 percent going from Advance to Third. The corresponding figure for Core PCE is 0.35 percent. Perhaps this is why the Fed focused more on price/inflation targets, i.e.:

…variants of so-called makeup strategies, “so called” because they at times require the Committee to deliberately target rates of inflation that deviate from 2 percent on one side so as to make up for times that inflation deviated from 2 percent on the other side. Price-level targeting (PLT) is a useful benchmark among makeup policies but also represents a more significant and perhaps undesirable departure from the flexible inflation-targeting framework compared with other alternatives. “Nearer neighbors” to flexible inflation targeting are more flexible variants of PLT, which include temporary PLT—that is, use of PLT only around ELB episodes to offset persistently low inflation—and average inflation targeting (AIT), including one-sided AIT, which only restores inflation to a 2 percent average when it has been below 2 percent, and AIT that limits the degree of reversal for overshooting and undershooting the inflation target.10

Admittedly, the estimation of output gap is fraught with much larger (in my opinion) measurement challenges than the trend in nominal GDP, as it compounds the problems of real GDP measurement and potential GDP estimation; this is a point made by Beckworth and Hendrickson (JMCB, 2019). Even use of the unemployment rate, which can be substituted for the output gap in the Taylor principle by way of Okun’s Law, encounters a problem. As Aruoba (2008) notes, the unemployment rate is not subject to large and/or biased revisions; however the estimated natural rate of unemployment, on the other hand, does change over time, as estimated by CBO by Fed, and others, so there is going to be revision to the implied unemployment gap (this point occupies a substantial portion of JEC report). Partly for this reason, the recently announced modification of the Fed’s policy framework stresses shortfalls rather than deviations, discussed in this post.

One interesting aspect of the debate over nominal GDP targeting relates to growth rates vs. levels. If it’s growth rates (as in Beckworth and Hendrickson (JMCB, 2019), there is generally a “fire and forget” approach to setting rates. An actual nominal GDP target of the level implies that past errors are not forgotten (McCallum, 2001) (this is not a distinction specific to GDP as we know from the inflation vs. price level debate). Targeting the level of nominal GDP faces another — perhaps even more problematic — challenge, as suggested by Figure 2.

{kind=link}

Figure 2: Nominal GDP in billions of current dollars, SAAR, from various vintages. NBER defined recession dates shaded gray. Dashed red line at annual benchmark revisions. Red arrows denote implied revisions to last overlapping observation between two benchmarked series. Source: ALFRED.

Revisions can be large at benchmark revisions, shown as dashed lines in the above Figure. But even nonbenchmark revision can be large, as in 2009Q3. ( Beckworth (2019) suggests using a Survey of Professional Forecasters forecast relative to target and a level gap as means of addressing this issue — I think — insofar as the target can be moved relative to current vintage.)

None of the foregoing should be construed as a comprehensive case against some form of nominal GDP targeting — after all Frankel with Chinn (JMCB, 1995) provides some arguments in favor. But it suggests that the issue of data revisions in the conduct of monetary policy is not inconsequential.

Fear.

It is a key driver of behavior, whether in markets (Fear & Greed), politics (Tribalism), Health care (Anti-Vaxxers) or whatever (FOMO).

Fear is a great memory aid. For most of human history, people communicated not via the written word, but by oral storytelling. Hence, we are primed for emotional, memorable narratives. Looking at data and performing cold, calculated analyses is a learned, not innate, skill.

Social media understands this. Is it any surprise the algorithms of Facebook surfaces the most extreme views and claims? Look at what plays directly into that evolutionary trait, via clickbait and manufactured outrage. With our perfect hindsight bias, isn’t it obvious how inevitable this was?

Irrational fear is a driver of much of what we think and do. Often reflexively, frequently without thought. Contemplate what this means as you process new pandemic information, relying on mental models, performing data analysis.

How often do we react to a headline we disagree with, but after diving into the data underneath, it changes our mind? Not often enough, but on those rare occasions when that happens, it is a sign that you are doing this correctly. Our first reaction is the thoughtless programmed emotional response; the second is the more complex analytical result. It is your lizard brain (basal ganglia and brainstem) versus developed frontal lobe (neocortex).

Which brings us back to Covid-19. The probability of anyone of person getting this disease and then suffering a fatality is exceedingly low. I don’t want to suggest things are statistically normal, and you should definitely do things to stay safe: wear masks, socially distance, wash your hands frequently, and not touch your face. You can be (relatively) safe by doing these simple things.

But excess fear is driving all sorts of negative consequences, including stress, psychoses, economic damage, relationship issues, and health problems. This is counter-productive.

One day, this pandemic will end. Then we can all go back to worrying about cholesterol, high blood pressure and sugar.

Previously:

Over/Under Represented: Causes of Death in the Media (June 13, 2020)

Fearing the Dramatic, Complacent for the Mundane (April 29, 2020)

Denominator Blindness, Shark Attack edition (February 5, 2020)

Shark Attacks Illustrate an Investing Problem (February 4, 2020)

MiB: Danny Kahneman (February 11, 2020)

Crashes & Terrorists & Sharks – Oh, My! (November 9, 2020)

How’s Your MetaCognition? (August 16, 2020)

Source: Our World In Data

The post Fear & Data appeared first on The Big Picture.

COMMENT: Mart, this is tearing my family apart. I can no longer even speak to my son. He is against Trump simply because he does not like him personally or his tweets. I try to explain this should not turn on those issues. This is a war for your future. My son will not listen and he will vote against himself and is too brainwashed to see the bigger picture.

GA

ANSWER: I know of many people in the same boat. Even two of my business partners had ended all communication with their children. My partner, who died about 20 years ago, insisted I make sure everything went to his second wife and nothing to his children in the event of his death. These things are sad, but the brainwashing that has been taking place is thicker than even blood. It is very sad. But this is precisely what was carried out in East Germany. They deliberately tried to turn the children against their parents. That was a strategic tool of the left. This entire COVID-19 scheme is dividing the country. One father wrote in and said his son said all he cared about was taxes. They have no idea what their vote will mean in this election.

This is an agenda that is well organized, and it is a major effort as was the Communist Revolution of 1848 and then 1917/1918. People know about the Weimar Republic and the hyperinflation of the 20s, but it was a revolution in Germany in 1918 that overthrew the government, even boldly asked Russia to come to absorb Germany so they could enjoy the Communist Utopia, that led to the chaos. People hoarded all wealth and converted to foreign currencies.

This is an agenda that is well organized, and it is a major effort as was the Communist Revolution of 1848 and then 1917/1918. People know about the Weimar Republic and the hyperinflation of the 20s, but it was a revolution in Germany in 1918 that overthrew the government, even boldly asked Russia to come to absorb Germany so they could enjoy the Communist Utopia, that led to the chaos. People hoarded all wealth and converted to foreign currencies.

The idealistic fools who were brainwashed were left penniless. This is the fate of your son, sad to say. Those with any wealth, the older people, understood what was at stake. They prepared. The youth, believing in Utopia, suffered from hyperinflation. When the new currency was finally created in 1925, it was backed by real estate — not gold which had vanished thanks to hoarding.

Unfortunately, the youth are blind. Biden is a puppet. He will surrender the sovereignty to the United Nations and this is why they are fighting so hard. Michael Bloomberg is very evil. He is trying to pay all the fines, $20 million, of felons in Florida with the implication they will vote for Biden. I really do not want to live in a world where Bloomberg has any power whatsoever. The nice things will be to see Gates, Zuckerberg, and Bloomberg, among a long list of others supporting this new tyranny, will then become the targets are stripped of their wealth as the final phase takes place — nationalization of companies.

There is nothing you can do. They have been brainwashed. It is hard to bear. But we simply must understand that they are creating this new world and they will ONLY learn from experience. We cannot shelter them. To walk, they have to fall many times. This can be irreversible. Unless they see the error of their ways soon, then the split becomes permanent. The more you try to show them, the more they will not listen. That’s why it is so important to pay attention to what they are being told in school.

To understand my story, you first need to understand Friedman’s basic point. Here it is in a nutshell: Managers are employees of corporations. In the decisions they make with corporate resources, they should be responsible to the corporation. That means being responsible to the stockholders, who, after all, are the corporation’s owners. The vast majority of stockholders want the corporation to, in Friedman’s words, “make as much money as possible.” Thus Friedman’s claim that the social responsibility of a corporation is to make money. Friedman was clear that he wasn’t advocating breaking the rules. He stated that the managers should conform “to the basic rules of the society, both those embodied in law and those embodied in ethical custom.”

I learned Friedman’s point in a personal way when I was eleven. My mother had raised us to help others. I liked doing that and didn’t see it as a heavy obligation. But when I was eleven, my brother, Paul, who was fourteen, bought a cheap set of golf clubs and hired me to caddy for him. When we were on the eighth hole of a nine-hole course near our summer cottage in Minaki, Ontario, we saw a golfer hunting in the rough for his lost golf ball. I thought I should stop and help, so I did.

Paul had a different view: he wanted to play through and I was working for him and so I should do what he asked. We had a big argument and I finally gave in. When we got home, my brother complained to my mother that I hadn’t kept my side of the bargain. I was sure my mother would support me. She didn’t. “When Paul hired you,” she said, “you were working for him. When you’re on your own you can stop and help someone find his ball, but when you’re working for someone, he has the right to decide whether to let you.”

The lesson stung, but I ended up agreeing. That’s why the most important part of Friedman’s essay spoke to me. It’s simply wrong, when you’re working for someone, to use his resources for your ends when they don’t promote his ends. In the case with my brother, I was using my time to help others but my time was really his time: he was paying for it. In the case of corporations, managers might be using both their time and the corporation’s resources to help others even though shareholders own those resources and own the manager’s time that they are paying for.

This is from David R. Henderson, “Friedman’s Critics Miss the Mark,” Defining Ideas, September 24, 2020.

I was one of the 20 people asked to comment on passages of Friedman’s famous 1970 NY Times essay, “The Social Responsibility of Business Is to Increase Its Profits. Hoover colleague and EconTalk host Russ Roberts was another.

One of the strangest comments was by Felicia Wong. I write:

Commenter Felicia Wong, president and CEO of the Roosevelt Institute, notes that Friedman wrote when America’s “overwhelmingly white” fears were about Watts, Detroit, Vietnam, Kent State, Jackson State, and the assassinations of Martin Luther King Jr. and Robert Kennedy. Hmm. I recall that when King and Kennedy were murdered a lot of black people were upset, too, particularly by King’s murder.

I did note an irony in Friedman’s original essay though:

I’ll end by noting an ironic argument in Friedman’s essay that I don’t agree with and I wonder if even he would agree with today. Fortunately, it doesn’t undercut his case against corporate social responsibility. In stating that managers shouldn’t use corporate resources at the expense of shareholders, even for purposes that a huge percentage of us would agree are good, Friedman argued that we should leave those functions to the government. He wrote:

On the level of political principle, the imposition of taxes and the expenditure of tax proceeds are governmental functions. We have established elaborate constitutional, parliamentary, and judicial provisions to assure that taxes are imposed so far as possible in accordance with the desires of the public—after all, “taxation without representation” was one of the battle cries of the American Revolution.

That ignores what we have learned, and Friedman learned, from the “Public Choice” school of economics, led by James Buchanan and Gordon Tullock. Government’s incentives are usually perverse and we see the bad results almost daily. There’s much more hope, and I think Friedman shared that hope, for private voluntary activity.

Read the whole thing.

(2 COMMENTS)

Source link

-

Business2 months ago

Business2 months agoBernice King, Ava DuVernay reflect on the legacy of John Lewis

-

World News2 months ago

Heavy rain threatens flood-weary Japan, Korean Peninsula

-

Technology2 months ago

Technology2 months agoEverything New On Netflix This Weekend: July 25, 2020

-

Finance4 months ago

Will Equal Weighted Index Funds Outperform Their Benchmark Indexes?

-

Marketing Strategies9 months ago

Top 20 Workers’ Compensation Law Blogs & Websites To Follow in 2020

-

World News8 months ago

World News8 months agoThe West Blames the Wuhan Coronavirus on China’s Love of Eating Wild Animals. The Truth Is More Complex

-

Economy11 months ago

Newsletter: Jobs, Consumers and Wages

-

Finance10 months ago

Finance10 months ago$95 Grocery Budget + Weekly Menu Plan for 8