Finance

10 Financial Steps to Take Before Having Kids

According to the U.S. Department of Agriculture (USDA), raising a child to the age of 18 sets families back an average of $233,610, and that’s for each child. This figure doesn’t even include the cost of college, which is growing faster than inflation.

CollegeBoard data found that for the 2019-2020 school year, the average in-state, four-year school costs $21,950 per year including tuition, fees, and room and board.

Kids can add meaning to your life, and most parents would say they’re well worth the cost. But having your financial ducks in a row — before having kids — can help you spend more time with your new family instead of worrying about paying the bills.

10 Financial Moves to Make Before Having Kids

If you want to have kids and reach your long-term financial goals, you’ll need to make some strategic moves early on. There are plenty of ways to set yourself up for success, but here are the most important ones.

1. Start Using a Monthly Budget

When you’re young and child-free, it’s easy to spend more than you planned on fun activities and nonessentials. But having kids has a way of ruining your carefree spending habits, and that’s especially true if you’ve spent most of your adult life buying whatever catches your eye.

That’s why it’s smart to start using a monthly budget before having kids. It helps you prioritize each dollar you earn every month so you’re tracking your family’s short- and long-term goals.

You can create a simple budget with a pen and paper. Each month, list your income and recurring monthly expenses in separate columns, and then log your purchases throughout the month. This gives you a high-level perspective about money going in and out of your budget. You can also use a digital budgeting tool, like Mint, Qube Money, or You Need a Budget (YNAB) to get a handle on your finances.

Regardless of which budgeting tool you choose, create categories for savings (e.g. an emergency fund, vacation fund, etc.) and investments. Treat these expense categories just like regular bills as a way to commit to your family’s money goals. Your budget should provide a rough guide that helps you cover household expenses and save for the future while leaving some money for fun.

2. Build an Emergency Fund

Most experts suggest keeping three- to six-months of expenses in an emergency fund. Having an emergency fund is even more crucial when you have kids. You never know when you’ll face a broken arm, requiring you to cover your entire health care deductible in one fell swoop.

It’s also possible your child could be born with a critical medical condition that requires you to take time away from work. And don’t forget about the other emergencies you can face, from a roof that needs replacing to a job loss or income reduction.

Your best bet is opening a high-yield savings account and saving up at least three months of expenses before becoming a parent. You’ll never regret having this money set aside, but you’ll easily regret not having savings in an emergency.

3. Boost Your Retirement Savings Percentage

Your retirement might be decades away, but making retirement savings a priority is a lot easier when you don’t have kids. And with the magic of compound interest that lets your money grow exponentially over time, you’ll want to get started ASAP.

By boosting your retirement savings percentage before having kids, you’ll also learn how to live on a lower amount of take-home pay. Try boosting your retirement savings percentage a little each year until you have kids.

Go from 6% to 7%, then from 8% to 9%, for example. Ideally, you’ll get to the point where you’re saving 15% of your income or more before becoming a parent. If you’re already enrolled in an employer-sponsored retirement plan, this change can be done with a simple form. Ask your employer or your HR department for more information.

If you’re self-employed, you can still open a retirement account like a SEP IRA or Solo 401(k) and begin saving on your own. You can also consider a traditional IRA or a Roth IRA, both of which let you contribute up to $6,000 per year, or $7,000 if you’re ages 50 or older.

4. Start a Parental Leave Fund

Since the U.S. doesn’t mandate paid leave for new parents, check with your employer to find out how much paid time off you might receive. The average amount of paid leave in the U.S. is 4.1 weeks, according to a study by WorldatWork, which means you might face partial pay or no pay for some weeks of your parental leave period. It all depends on your employer’s policy and how flexible it is.

Your best bet is figuring out how much time you can take off with pay, and then creating a plan to save up the income you’ll need to cover the rest of your leave. Let’s say you have four weeks of paid time off, but plan on taking 10 weeks of parental leave, for example. Open a new savings account and save weekly or monthly until you have six weeks of pay saved up.

If you have six months to wait for the baby to arrive and you need $6,000 saved for parental leave, you could strive to set aside $1,000 per month for those ten weeks off. If you’re able to plan earlier, up to 12 months before the baby arrives, then you can cut your monthly savings amount and set aside just $500 per month.

5. Open a Health Savings Account (HSA)

A health savings account (HSA) is a tax-advantaged way to save up for health care expenses, including the cost of a hospital stay. This type of account is available to Americans who have a designated high-deductible health insurance plan (HDHP), meaning a deductible of at least $1,400 for individuals and at least $2,800 for families. HDHPs must also have maximum out-of-pocket limits below $6,900 for individuals and $13,800 for families.

In 2020, individuals can contribute up to $3,550 to an HSA while families can save up to $7,100. This money is tax-advantaged in that it grows tax-free until you’re ready to use it. Moreover, you’ll never pay taxes or a penalty on your HSA funds if you use your distributions for qualified health care expenses. At the age of 65, you can even deduct money from your HSA and use it however you want without a penalty.

6. Start Saving for College

The price of college will only get worse over time. To get a handle on it early and plan for your future child’s college tuition, start saving for their education in a separate account. Once your child is born, you can open a 529 college savings account and list your child as its beneficiary.

Some states offer tax benefits for those who contribute to a 529 account. For example, Indiana offers a 20% tax credit on up to $5,000 in 529 contributions each year, which gets you up to $1,000 back from the state at tax time. Many plans also let you invest in underlying investments to help your money grow faster than a traditional savings account.

7. Pay Off Unsecured Debt

If you have credit card debt, pay it off before having kids. You’re not helping yourself by spending years lugging high-interest debt around. Paying off debt can free-up cash and save you thousands of dollars in interest every year.

If you’re struggling to pay off your unsecured debt, there are several strategies to consider. Here are a few approaches:

Debt Snowball

This debt repayment approach requires you to make a large payment on your smallest account balance and only the minimum amount that’s due on other debt. As the months tick by, you’ll focus on paying off your smallest debt first, only to “snowball” the payments from fully paid accounts toward the next smallest debt. Eventually, the debt snowball should leave you with only your largest debts, then one debt, and then none.

Debt Avalanche

The debt avalanche is the opposite of the debt snowball, asking you to pay off the debt with the highest interest rate first, while paying the minimum payment on other debt. Once that account is fully paid, you’ll “avalanche” those payments to the next highest-rate debt. Eventually, you’ll only be left with your lowest-interest account until you’ve paid off all of your debt.

Balance Transfer Credit Card

Another popular strategy involves transferring high-interest balances to a balance transfer credit card that offers 0% APR for a limited time. You might have to pay a balance transfer fee (often 3% to 5%), but the interest savings can make this strategy worth it.

If you try this strategy, make sure you have a plan to pay off your debt before your introductory offer ends. If you have 15 months at 0% APR, for example, calculate how much you need to pay each month for 15 months to repay your entire balance during that time. Any debt remaining after your introductory APR period ends will start accruing interest at the regular, variable interest rate.

8. Consider Refinancing Other Debt

Ditching credit card debt is a no-brainer, but debt like student loans or your home mortgage can also weigh on your future family’s budget.

If you have student loan debt, look into refinancing your student loans with a private lender. A student loan refinance can help you lower the interest rate on your loans, find a manageable monthly payment, and simplify your repayment into one loan.

Private student loan rates are often considerably lower than rates you can get with federal loans — sometimes by half. The caveat with refinancing federal loans is that you’ll lose out on government protections, like deferment and forbearance, and loan forgiveness programs. Before refinancing your student loans, make sure you won’t need these benefits in the future.

Also look into the prospect of refinancing your mortgage to secure a shorter repayment timeline, a lower monthly payment, or both. Today’s low interest rates have made mortgage refinancing a good deal for anyone who took out a mortgage several years ago. Compare today’s mortgage refinancing rates to see how much you can save.

9. Buy Life Insurance

You should also buy life insurance before having kids. Don’t worry about picking up an expensive whole life policy. All you need is a term life insurance policy that covers at least 10 years of your salary, and hopefully more.

Term life insurance is extremely affordable and easy to buy. Many providers don’t even require a medical exam if you’re young and healthy.

Once you start comparing life insurance quotes, you’ll be shocked at how affordable term coverage can be. With Bestow, for example, a thirty-year-old woman in good health can buy a 20-year term policy for $500,000 for as little as $20.41 per month.

10. Create a Will

A last will and testament lets you write down what should happen to your major assets upon your death. You can also state personal requests in writing, like whether you want to be kept on life support, and how you want your final arrangements handled.

A will can also formally define who you’d like to take over custody of your kids, if both parents die. If you don’t formally make this decision ahead of time, these deeply personal decisions might be left to the courts.

Fortunately, it’s not overly expensive to create a last will and testament. You can meet with a lawyer who can draw one up, or you can create your own using a platform like LegalZoom.

The Bottom Line

Having kids can be the most rewarding part of your life, but parenthood is far from cheap. You’ll need money for expenses you might’ve never considered before — and the cost of raising a family only goes up over time.

That’s why getting your money straightened out is essential before kids enter the picture. With a financial plan and savings built up, you can experience the joys of parenthood without financial stress.

The post 10 Financial Steps to Take Before Having Kids appeared first on Good Financial Cents®.

Right now, the market is at all time highs, and at some point in the future, it will inevitably pull back. While investing is long term, you might have short-er term goals that require short term investments.

If you’re a young investor and don’t want to see an immediate decline in your portfolio, now’s a good time to consider short term investment options. Short term investments typically don’t see the growth of longer term investments, but that’s because they are designed with safety and a short amount of time in mind.

However, millennials honestly haven’t experienced a prolonged bear or flat market. While the Great Recession was tough, millennials have seen their net worth’s grow. However, in periods of uncertainty, it can make sense to invest in short term investments.

Also, for millennials who may be looking at life events in the near future (such as buying a house or having a baby), having short term investments that are much less likely to lose value could make a lot of sense.

If you’re a young investor looking for a place to stash some cash for the short term, here are ten of the best ways to do it.

1. Online Checking and Savings Accounts

Online checking and savings accounts are one of the best short term investments for several reasons:

- They have higher interest rates than traditional accounts

- They are completely safe: your accounts are FDIC insured up to $250,000

- You can access your money any time and don’t have to worry about losing interest as a result

However, to get the very best rates from online checking and savings account, you typically have to do one of the following:

- Contribute a certain amount to the account (say $10,000 minimum)

- Sign up for direct deposit into the account

- Use your debit card for a certain number of transactions each month

If you’re going to be doing those types of transactions anyway, signing up for one of these accounts can make a lot of sense. And to make these accounts even more attractive, interest rates have been rising the last few months making yields go higher.

Our favorite online savings account right now is CIT Bank. They offer 0.60% APY online savings accounts with just a $100 minimum deposit! Check out CIT Bank here.

Check out the other best high yield savings accounts here.

2. Money Market Accounts

Money market accounts are very similar to online savings accounts, with one exception. Money market accounts typically aren’t FDIC insured. As a result, you actually can earn a little higher interest rate on the account versus a typical savings account.

Money market accounts typically have account minimums that you have to consider as well, especially if you want to earn the best rate.

Our favorite money market account right now is CIT Bank. They offer 0.60% APY money market accounts with just a $100 minimum deposit! Check out CIT Bank here.

Check out our list of the best online bank accounts for your money.

3. Certificates Of Deposit (CDs)

Certificate of deposits (CDs) are the next best place that you can stash money as a short term investment. CDs are bank products that require you to keep the money in the account for the term listed - anywhere from 90 days to 5 years. In exchange for locking your money up for that time, the bank will pay you a higher interest rate than you would normally receive in a savings account.

The great thing about CDs is that they are also FDIC insured to the current limit of $250,000. If you want to get fancy and you have more than $250,000, you can also sign up for CDARS, which allows you to save millions in CDs and have them insured.

Our favorite CD of the moment is the CIT Bank 11-Month Penalty Free CD! Yes, penalty free! Check it out.

We maintain a list of the best CD rates daily if you want to explore other options.

4. Short Term Bond Funds

Moving away from banking products and into investment products, another area that you may consider is investing in short term bonds. These are bonds that have maturities of less than one year, which makes them less susceptible to interest rate hikes and stock market events. It doesn’t mean they won’t lose value, but they typically move less in price than longer maturity bonds.

There are three key categories for bonds:

- U.S. Government Issued Bonds

- Corporate Bonds

- Municipal Bonds

With government bonds, your repayment is backed by the U.S. government, so your risk is minimal. However, with corporate bonds and municipal bonds, the bonds are backed by local cities and companies, which increased the risk significantly.

However, it’s important to note that investing in a bond fund is different than investing in a single bond, and if you invest in a bond fund, your principal can go up or down significantly. Here’s a detailed breakdown of why this happens: Buying a Bond Fund vs. Buying A Single Bond.

If you do want to invest in bonds, you have to do this through a brokerage. The best brokerage I’ve found for both buying individual bonds and bond funds is TD Ameritrade. TD Ameritrade has a bond screener built into it’s platform that makes it really easy to search for individual bonds to buy, and gives you a breakdown of all aspects of the bond.

Also, TD Ameritrade offers a $0 minimum IRA and hundreds of commission-free ETFs.

5. Treasury Inflation Protected Securities (TIPS)

Treasury Inflation Protected Securities (TIPS) are a type of government bond that merits their own section. These are specially designed bonds that adjust for inflation, which makes them suitable for short term investments as well as long term investments. TIPS automatically increase what they pay out in interest based on the current rate of inflation, so if it rises, so does the payout.

What this does for bondholders is protect the price of the bond. In a traditional bond, if interest rates rise, the price of the bond drops, because new investors can buy new bonds at a higher interest rate. But since TIPS adjust for inflation, the price of the bond will not drop as much - giving investors more safety in the short term.

You can invest in TIPS at a discount brokerage like TD Ameritrade. Some of the most common ETFs that invest in TIPs (and are commission-free at TD Ameritrade):

- STPZ - PIMCO 1-5 Year U.S. TIPS Index

- TIP - iShares TIPS Bond ETF

6. Floating Rate Funds

Floating rate funds are a very interesting investment that don’t get discussed very often - but they are a really good (albeit risky) short term investment. Floating rate funds are mutual funds and ETFs that invest in bonds and other debt that have variable interest rates. Most of these funds are invested in short term debt - usually 60 to 90 days - and most of the debt is issued by banks and corporations.

In times when interest rates are rising, floating rate funds are poised to take advantage of it since they are consistently rolling over bonds in their portfolio every 2-3 months. These funds also tend to pay out good dividends as a result of the underlying bonds in their portfolios.

However, these funds are risky, because many invest via leverage, which means they take on debt to invest in other debt. And most funds also invest in higher risk bonds, seeking higher returns.

If you want to invest in a floating rate fund, you have to do this at a brokerage as well. TD Ameritrade is a great choice for this as well. The most common floating rate funds are:

- FLOT - iShares Floating Rate Bond ETF

- FLRN - Barclay’s Capital Investment Grade Floating Rate ETF

- FLTR - VanEck Vectors Floating Rate ETF

- FLRT - Pacific Asset Enhanced Floating Rate ETF

7. Selling Covered Calls

The last “true” investment strategy that you can use in the short term is to sell covered calls on stocks that you already own. When you sell a call on a stock you own, another investor pays you a premium for the right to buy your stock at a given price. If the stock never reaches that price by expiration, you simply keep the premium and move on. However, if the stock does reach that price, you’re forced to sell your shares at that price.

In flat or declining markets, selling covered calls can make sense because you can potentially earn extra cash, while having little risk that you’ll have to sell your shares. Even if you do sell, you may be happy with the price received anyway.

To invest in options, you need a discount brokerage that supports this. TD Ameritrade has some of the best options trading tools available through their ThinkorSwim platform.

Related: Best Options Trading Platforms

8. Pay Off Student Loan Debt

Do you want a guaranteed return on your money over the short run? Well, the best guaranteed return you can get is paying off your student loan debt. Typical student loan debt interest rates vary from 4-8%, with many Federal loans at 6.8%. If you simply pay off your debt, you can see an instant return on your money of 6.8% or more, depending on your interest rate.

Maybe you can’t afford to pay it all off right now. Well, you could still look at refinancing your student loan debt to get a lower interest rate and save some money.

We recommend Credible to refinance your student loan debt. You can get up to a $750 bonus when you refinance by using our special link: Credible >>

9. Pay Off Credit Card Debt

Similar to getting out of student loan debt, if you pay off your credit card debt you can see an instant return on your money. This is a great way to use some cash to help yourself in the short term.

There are very few investments that can equal the return of paying off credit card debt. With the average interest rate on credit card debt over 12%, you’ll be lucky to match that in the stock market once in your life. So, if you have the cash to spare, pay down your credit card debt as quickly as possible.

If you’re struggling to figure out a way out of credit card debt, we recommend first deciding on an approach, and then using the right tool to get out of debt.

For the approach, you can choose between the debt snowball and debt avalanche. Once you have a method, you can look at tools.

First, you need to get financially organized. Use a free tool like Personal Capital to get started. You can link all your accounts and see where you stand financially.

Next, consider either:

- Balance Transfer: If you can qualify for a balance transfer credit card, you have the potential to save money. Many cards offer a promotional 0% balance transfer for a set period of time, so this can save you interest on your credit card debt while you work to pay it off.

- Personal Loan: This may sound counter-intuitive, but most personal loans are actually used to consolidate and manage credit card debt. By getting a new personal loan at a low rate, you can use that money to pay off all your other cards. Now you have just one payment to make. Compare personal loans at Credible here.

10. Peer To Peer Lending

Finally, you could invest in peer to peer loans through companies like LendingClub and Prosper. These aren’t completely short term investments - many loans are for 1-3 years, with some longer loans now available. However, that is shorter than what you’d traditionally want to invest for in the stock market.

With peer to peer lending, you get a higher return on your investment, but there is the risk that the borrower won’t pay back the loan, causing you to lose money. Many smart peer to peer lenders spread out their money across a large amount of loans. Instead of investing $1,000 in just one loan, they many invest $50 per loan across 20 different loans. That way, if one loan fails, they still have 19 other loans to make up the difference.

One of the great aspects of peer to peer lending is that you get paid monthly on these loans, and the payments are a combination of principal and interest. So, after several months, you’ll typically have enough to invest in more loans immediately, thereby increasing your potential return.

We are huge fans of LendingClub as a CD alternative, and you can sign up for LendingClub here.

Frequently Asked Questions

Here are some common questions about short term investments.

What makes a short term investment?

A short term investment is one that has a time frame of less than 5 years. Typically, short term investments are done to be more stable - but at the end of the day, it’s all about time frame.

Are short term investments risky?

They can be. The duration of the investment does not imply less risk. While some short term investments are risk-free (like savings accounts), others are extremely risky (like peer to peer lending).

Who should consider short term investments?

Anyone who is looking for an investment duration of less than 5 years. While it’s common to think people nearing retirement may need a short term investment, any age - including young adults - can benefit.

Is debt payoff an investment?

We think so! Paying off debt is a guaranteed return, especially in the short term.

{"@context":"https://schema.org","@type":"FAQPage","mainEntity":[{"@type":"Question","name":"What makes a short term investment?","acceptedAnswer":{"@type":"Answer","text":"A short term investment is one that has a time frame of less than 5 years. Typically, short term investments are done to be more stable - but at the end of the day, it's all about time frame."}},{"@type":"Question","name":"Are short term investments risky?","acceptedAnswer":{"@type":"Answer","text":"They can be. The duration of the investment does not imply less risk. While some short term investments are risk-free (like savings accounts), others are extremely risky (like peer to peer lending)."}},{"@type":"Question","name":"Who should consider short term investments?","acceptedAnswer":{"@type":"Answer","text":"Anyone who is looking for an investment duration of less than 5 years. While it's common to think people nearing retirement may need a short term investment, any age - including young adults - can benefit."}},{"@type":"Question","name":"Is debt payoff an investment?","acceptedAnswer":{"@type":"Answer","text":"We think so! Paying off debt is a guaranteed return, especially in the short term."}}]}Final Thoughts

Finding short term investments can be tough. It’s a bit counter intuitive to invest, but only for a short period of time. As a result, you’ll typically see investments with lower returns, but also have lower risk of loss.

What are your favorite short term investments?

The post The 10 Best Short Term Investments appeared first on The College Investor.

Since the Dawn of Mustachianism in 2011, the same question has come up over and over again:

I see your point that index fund investing is the best option. But when you buy the index, you’re getting oil companies, factory farm slaughterhouses and a million other dirty stories.

How can I get the benefits of investing for early retirement without contributing to the decline of humanity?”

And in these nine years since then, the movement towards socially responsible investing has only grown. Public pension funds have started to “divest” from oil company stocks, and various social issues like human rights, child labor, climate change or corporate corruption have bubbled to the surface at different times.

And all of this has led to the exploding new field of Socially Responsible Investing (SRI), and a growing array of new ways to do it.

So it seems that this is not just a passing trend - people just might be starting to care a bit more. And since capitalism is just an expression of human behavior, the nature of capitalism itself may be starting to change.

This leads us naturally to the question:

What can I do with my money to help fix the world? And even better, is there a way I can make money in the process of fixing it?

The answer is a good, solid “Probably.”

As long as you don’t get too hung up on getting every last detail perfect, because just like real life, investing is a haphazard and approximate and unpredictable thing. But by understanding the big picture, you can make slightly better decisions on average, which lead to slightly better results. And slightly better results, stacked up consistently over time, can lead to a much better life, or even a much better world.

This is true in all of the main areas we care about - personal wealth, fitness and health, even relationships and happiness. And while your money and investments are certainly not the most important thing in life, they are still worthy of a bit of easy and effective optimization.

So anyway, the first thing to understand with SRI is, “what problem am I trying to solve?”

The answer is, “You are trying to make your investing (especially index fund investing) have a better impact on the world.”

On its own, index fund investing is ridiculously simple. You just get an account at any brokerage like Vanguard, Etrade, Schwab or whatever, and dump all your money into one exchange-traded fund: VTI.

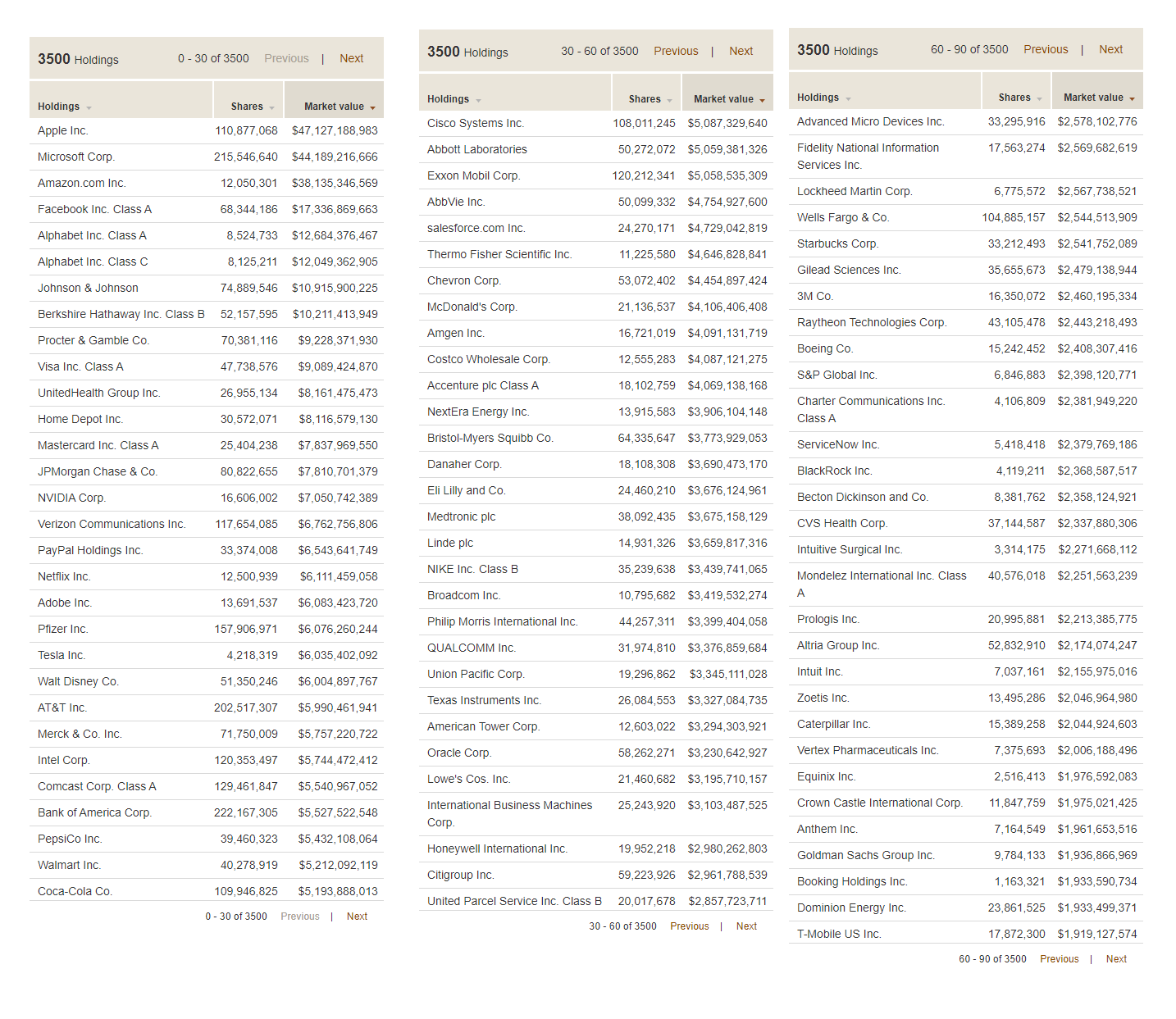

When you do this, you are buying a stake in 3500 companies at once(!), which is both impressive and overwhelming. How do you even know what you are holding?

Well, this is all public information, and easily available with a quick Google search. For example, here’s a list of the top 90 holdings in VTI (click for larger):

As you can see, the biggest chunk of money is allocated to today’s tech darlings, because this index fund is weighted according to market value, and these are the most valuable companies in the US today.

Through a convenient coincidence, the total value of the VTI fund happens to be just under $1 trillion dollars, which means you can just throw a decimal point after the ten billions digit of market value to get a percentage. In other words, about 4.7% of your money will go towards Apple stock, 4.4 towards Microsoft, and so on. Together, these top 90 companies are worth more than the remaining 3,410 companies combined, so these are what really drive your retirement account.

And within this list, you will see some of the usual suspects: Exxon and Chevron (oil), Philip Morris (tobacco), Raytheon and Lockheed (bombs), and so on.

But what about the less-usual suspects? For example, I happen to think that sugar, and especially sugar-packed beverages like Coke, is the biggest killer in the developed world - a major contributor to 2 million of the 2.8 million deaths each year in the US alone. Should I exclude that from my portfolio too?

And what about drug and insurance companies - aren’t they behind the political stalemate and high costs of the US healthcare system? Comcast funded some election disinformation campaigns here in my home town in the early 2010s, should I exclude them too? And if you’re part of a religion that is against charging interest on loans, or in favor of pasta and Pirate costumes, or against a spherical Earth, or any number of additional ornate rules, you may have still more preferences.

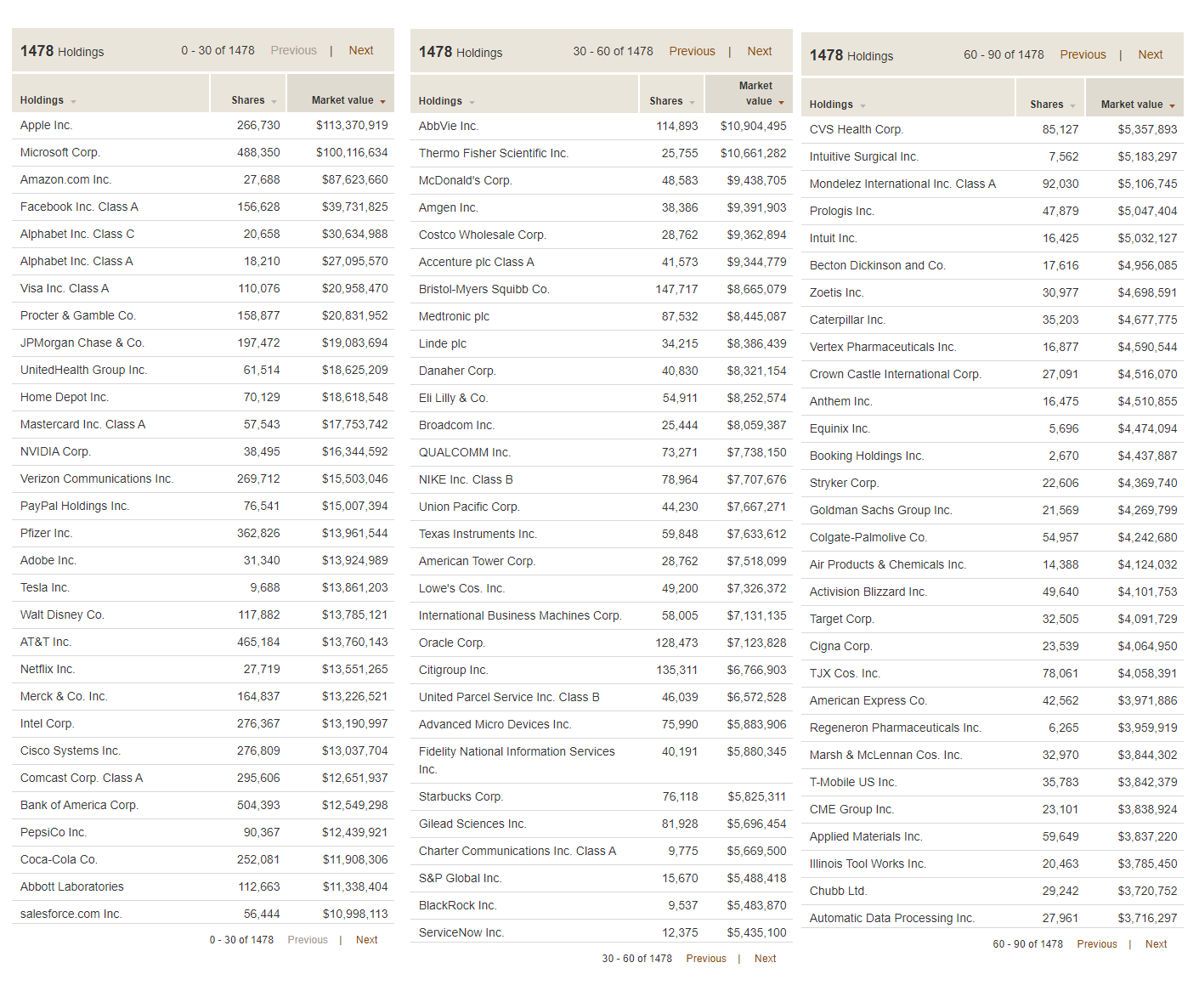

The higher your desire for perfection, the more difficult this exercise will become. However, if you are like me and you just want to get most of the desired result with minimal effort, you might simply have a look at the Vanguard fund called ESGV.

ESG stands for “Environmental, Social and Governance”, and in practice it just means “We have tried to avoid some of the shittier companies according to some fairly simple rules.”

And the result is this:

The first thing you’ll notice is that it’s almost the same. In fact, the top five holdings - Apple, Microsoft, Amazon, Facebook, Alphabet (Google) and Netflix not far behind, collectively referred to as the FAANG stocks - are completely unchanged - and this means that there will be plenty of correlation between these funds.

It’s also the reason that the stock market as a whole has recovered so quickly from this COVID-era recession: small businesses like restaurants and hair salons have been destroyed by the shutdowns, but big companies that benefit from people staying at home and using computers and phones are making more money than ever. The stock market isn’t the whole economy, it’s just the publicly traded companies, which are the big ones.

But let’s look at the biggest differences between the normal index fund versus the social version.

The following large companies listed on the left are missing in the ESGV fund, in order of size. And to make up the difference, the stake in the companies on the right have been boosted up to take their place in your portfolio.

The omission of Berkshire Hathaway was a bit of a shocker, as it is run with solid ethical principles by Warren Buffett, one of the worlds most generous philanthropists. And in fact the modern day nerd-saint Bill Gates is on the Berkshire board of directors, another person whose work I follow and respect greatly.

(side note: Apparently the company fails on the “independent governance” category. And Buffett disputes this category, but in his characteristic way has decided to say, “Fuck it, I’ma just keep doing my own thing with my half-trillion dollar empire over here and you can have fun with your little committee” - I’m paraphrasing a bit but he totally did say that.)

Furthermore, both funds hold the factory meat king Tyson foods, while neither holds Roundup-happy Monsanto, because it was bought by the German conglomerate Bayer AG a while back. Nextera is a giant electric utility in the Southeastern US that claims to be the world’s largest generator of renewable energy. Some do-gooders are against nuclear power, while others (including me) think it’s the Bee’s Knees and we should keep advancing it. And all this just goes to show how nobody will agree 100% on what makes a good socially responsible fund.

But What About The Performance?

In the past, some investors were nervous about giving up oil companies in their portfolio, because while it was a dirty substance, it was also what made the world go round - which meant it was a cash cow.

Now, however, oil is on its way out as renewable energy and battery storage have crossed the cost parity threshold - meaning it’s cheaper to make power (and vehicles) that don’t use oil. In its place, technology is the new cash cow, and tech is heavily represented in the ESG funds. The result:

As you can see, the performance has been similar but the ESG fund has done significantly better in the (admittedly short) time since it was introduced at Vanguard.

Of course, we have no idea if this will continue, but the point is that at least our thesis is not a ridiculous one - environmentally sustainable companies do have an advantage, if the world gradually starts to care more about these things. And if you look at the share price of Tesla and other companies that surround it in electric transportation and energy storage, you will see that there are many trillions of dollars already lining up to benefit from this transition. And the very presence of so much investment money creates a self-fulfilling prophecy, as Tesla is now building or expanding five of the world’s largest factories on three continents simultaneously.

So What Should You Do? (and what I do myself)

First of all, it helps to remember a fundamental piece of economics: your spending dollars will probably have a much bigger impact than your investment dollars. This is because you are sending a direct message to the world rather than an indirect one:

When you buy a new gasoline-powered Subaru (or a tank of gas for your existing guzzler) or a steak at the grocery store, or a plane ticket, you are telling those companies directly that consumers want more of these products, so they will produce more of them immediately.

When you buy shares in Exxon, you are only subtly raising the demand for those shares, which raises the average price, making it ever-so-slightly easier for Exxon to maybe issue more shares in the future. In other words, you are making it easier for them to access capital. But capital is only useful if there is demand for their products. And with oil there is a nearly constant surplus, which is why OPEC and other cartels need to work together to artificially restrict supply, just to keep prices up.

Plus, as a shareholder you are theoretically eligible to place votes and influence the future direction of companies - even companies that you don’t like. If you look up the field of “shareholder activism”, you’ll see this is a tradition that goes way back.

So I have tried to take a few simple steps on the consumer side myself, and I find it quite satisfying: Insulating the shit out of all of my properties, building a DIY solar electric array on one of them, and buying one electric car so far to eliminate local gas burning. And a few electric bikes including a super fast one I made myself.

Each one of these steps has provided a very high economic return, percentage-wise, but that still leaves a lot of money to account for, which brings us back to stock investing.

As someone who loves simplicity, I have done this:

- Bought almost entirely VTI (or similar Vanguard funds) from 2000-2015

- Started experimenting with Betterment in 2015, liked it, and have been adding a percentage of my ongoing savings to that account to that since then. (Note that Betterment now also offers a socially responsible portfolio option.)

- Switched the dividend re-investing of my old Vanguard VTI over to Vanguard ESGV, to avoid “wash sales” in making the most of Betterment’s tax loss harvesting feature.

- Bought some shares of Berkshire Hathaway separately, and also make a few sentimental investments in local businesses, including the MMM HQ Coworking space.

But you could choose to be more hardcore in your ESG/SRI investing:

- Buy your own basket of stocks based on the index, but with different weighting based on your own values

- Spend more money on other things that generate or save money (a bigger solar array on your house, better insulation, electric car, an ebike to reduce car trips, etc.)

- Invest in local businesses of your choice, rental real estate, community solar projects, or other things which generate passive income - publicly traded stocks are just one of many ways to fund an early retirement!

Like most areas of life, investing is not something you have to do perfectly in order to succeed - even socially responsible investing. If you apply the 80/20 rule to get the big picture right, you have probably found the Sweet Spot and you can move on to the next area of life to optimize.

In the Comments:

What is your own investment strategy? Have you thought at all about this ESG / SRI stuff? Did this article bring anything new to the table?

Given what we have seen in broad North American stock market indexes over the past six months, you could make the statement that COVID-19 doesn’t affect markets.

From the bottom in late March until recently, markets have risen steadily despite a backdrop of increasing global COVID cases. The explanation offered repeatedly along the way has been that the economy and the stock market are two different things. Besides, with lower interest rates investors would be foolish to bet against the Federal Reserve. On top of that, all of the significant government financial intervention would protect us from the worst impacts.

All of these comments are and have been true. I have said them myself and believe them. The question is can stock markets continue to rise when COVID-19 isn’t slowing down and may very well be getting worse? The answer is that it is increasingly unlikely.

Back in July, we hosted a webinar with an epidemiologist. At the time, they said it was “almost inevitable” that there would be a second wave of COVID-19. The rationale was threefold:

First, COVID-19 is an active virus with no vaccine or significant treatment, so it is unlikely to just “go away.”

Second, while a first wave saw new cases slow meaningfully, it wasn’t eliminated. Reopening happened while there were still new cases every day. This almost guarantees a second wave, as behaviours returned that increase the spread of COVID-19.

Third, the history of past pandemics shows that a second wave is almost always the case.

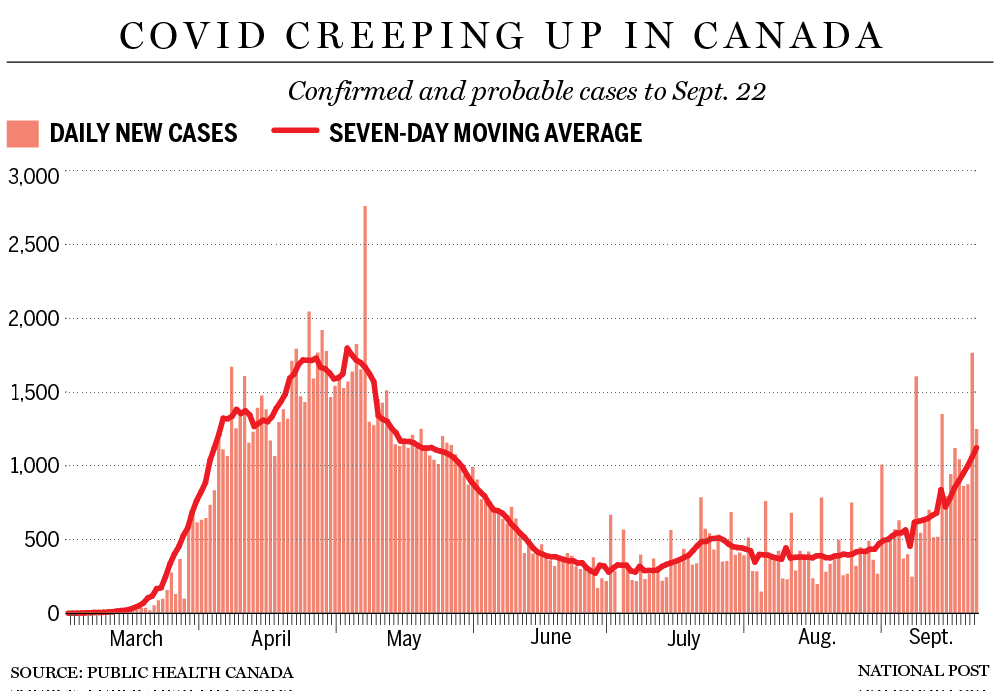

If we look globally, the number of new cases has continued to grow, with daily new cases regularly in the 250,000 to 300,000 range. Globally, there isn’t a second wave because the first wave never ended. Having said this, on a regional basis we are definitely seeing examples of second waves.

To get some sense of what we might face in Canada, it can be instructive to look at Europe, where numbers have meaningfully increased in the past month. If you look at Spain, they went from 10,000 new cases a day in March, to 400 new cases a day in June. Earlier this month they were back at 10,000 new cases a day. There can be no better definition of a second wave than those numbers. The good news is that the death rates have been much lower in this second wave (so far), with numbers 10 per cent to 20 per cent of what they were during the very dark days of March.

The policy response in Spain has been much more muted than the first time around. There is definitely a strong reluctance to shutting down the economy again. There is also a strong reluctance from some citizens and local governments to follow tough rules after going through such a hard time earlier in the year.

In Canada, the number of new COVID-19 cases has grown meaningfully this month. The chart is looking more and more like Spain, although we never had as many cases at the top. Hopefully death rates in Canada will remain much lower than at their peak. How will Canada react to this second wave? Time will tell, but based on our culture and reaction to date, there will probably be a little more willingness to accept tough measures from the government, and to shut some parts of the economy down if deemed necessary.

So what does this all mean for stock markets?

We still have exceptionally low interest rates, which have been a significant driver of strong stock markets. We still have major government spending (which seems to have no end in sight) to help backstop individuals and many companies as they deal with economic challenges. The one thing that we have today that is of concern is that stock markets are currently trading at very high historic valuations. This doesn’t leave you with a lot of room for error. A second wave of COVID-19 in major economic markets could certainly be cause for error. Global trade fights could be cause for error. U.S. political and social battles could be a cause for error. This all makes us cautious even after a dip in markets, like the one we saw on Monday.

When we talk about expensive or cheap stock market valuations, it is usually a form of price-earnings ratio. Essentially, this means that a company’s overall value is a multiple of its earnings or profitability. A more refined version called the Shiller P/E Ratio was developed by economist Robert Shiller.

Historically, a Shiller P/E ratio of 30 or higher has been a very expensive number. In times with very low interest rates, it would make sense that these numbers would get higher, but even over the past three years, this ratio has ranged between 25 and 33. It exceeded 32 at the beginning of September. At the same time, there is concern that corporate earnings growth cannot be maintained if we have more slowdowns caused by COVID-19 around the world. The Shiller P/E ratio is now back just under 30, but in this overall environment, we believe there is room for it to fall a little further.

After Monday’s sell-off, the U.S. tech-heavy Nasdaq was down 13.8 per cent from its level on Sept. 2. The broader-based S&P500 is down 10.6 per cent. The Dow Jones Industrial Average is down 8.2 per cent and the TSX is down 5.3 per cent.

We do not believe the declines are over. For markets to get back to where they were on June 1, the TSX would have to pull back another four per cent, while the Nasdaq would have to tumble another 11 per cent.

It is certainly possible that the declines don’t go that far, but we think there is a decent possibility that they will in the coming weeks. Indices are now back very close to the mid-July levels that we believed were expensive at that time.

As a firm, we do have some cash to invest at the moment, but we are now only dipping our toe in the pool in certain sectors. We are buying a little in utilities and consumer discretionary that we believe are cheap at these prices, but mostly staying on hold. Overall, we will likely be spending a meaningful amount of this cash between now and the end of the year, but mostly as we see some further declines.

We do see some good homes for cash in private credit investments that can take advantage of the high borrowing costs for corporations. Our focus for these investments is through the TriDelta Alternative Performance Fund, where we are aiming for returns in the eight per cent to 10 per cent range. Private credit investments have been quite solid throughout 2020.

We also see some opportunities in fixed-rate preferred shares, with Canadian dividend yields over five per cent and some price stability, and in gold as an alternative asset class given that cash is paying almost nothing and there are increasing concerns about the valuations and even stability of many major currencies.

As for stocks, we are getting a little closer, but mostly still keeping our powder dry.

Ted Rechtshaffen, MBA, CFP, CIM, is president and wealth adviser at TriDelta Financial, a boutique wealth management firm focusing on investment counselling and estate planning. You can contact Ted directly at

.

-

Business2 months ago

Business2 months agoBernice King, Ava DuVernay reflect on the legacy of John Lewis

-

World News2 months ago

Heavy rain threatens flood-weary Japan, Korean Peninsula

-

Technology2 months ago

Technology2 months agoEverything New On Netflix This Weekend: July 25, 2020

-

Finance4 months ago

Will Equal Weighted Index Funds Outperform Their Benchmark Indexes?

-

Marketing Strategies9 months ago

Top 20 Workers’ Compensation Law Blogs & Websites To Follow in 2020

-

World News8 months ago

World News8 months agoThe West Blames the Wuhan Coronavirus on China’s Love of Eating Wild Animals. The Truth Is More Complex

-

Economy11 months ago

Newsletter: Jobs, Consumers and Wages

-

Finance9 months ago

Finance9 months ago$95 Grocery Budget + Weekly Menu Plan for 8