Finance

Socially Responsible Investing: Is It Also More Profitable?

Since the Dawn of Mustachianism in 2011, the same question has come up over and over again:

I see your point that index fund investing is the best option. But when you buy the index, you’re getting oil companies, factory farm slaughterhouses and a million other dirty stories.

How can I get the benefits of investing for early retirement without contributing to the decline of humanity?”

And in these nine years since then, the movement towards socially responsible investing has only grown. Public pension funds have started to “divest” from oil company stocks, and various social issues like human rights, child labor, climate change or corporate corruption have bubbled to the surface at different times.

And all of this has led to the exploding new field of Socially Responsible Investing (SRI), and a growing array of new ways to do it.

So it seems that this is not just a passing trend - people just might be starting to care a bit more. And since capitalism is just an expression of human behavior, the nature of capitalism itself may be starting to change.

This leads us naturally to the question:

What can I do with my money to help fix the world? And even better, is there a way I can make money in the process of fixing it?

The answer is a good, solid “Probably.”

As long as you don’t get too hung up on getting every last detail perfect, because just like real life, investing is a haphazard and approximate and unpredictable thing. But by understanding the big picture, you can make slightly better decisions on average, which lead to slightly better results. And slightly better results, stacked up consistently over time, can lead to a much better life, or even a much better world.

This is true in all of the main areas we care about - personal wealth, fitness and health, even relationships and happiness. And while your money and investments are certainly not the most important thing in life, they are still worthy of a bit of easy and effective optimization.

So anyway, the first thing to understand with SRI is, “what problem am I trying to solve?”

The answer is, “You are trying to make your investing (especially index fund investing) have a better impact on the world.”

On its own, index fund investing is ridiculously simple. You just get an account at any brokerage like Vanguard, Etrade, Schwab or whatever, and dump all your money into one exchange-traded fund: VTI.

When you do this, you are buying a stake in 3500 companies at once(!), which is both impressive and overwhelming. How do you even know what you are holding?

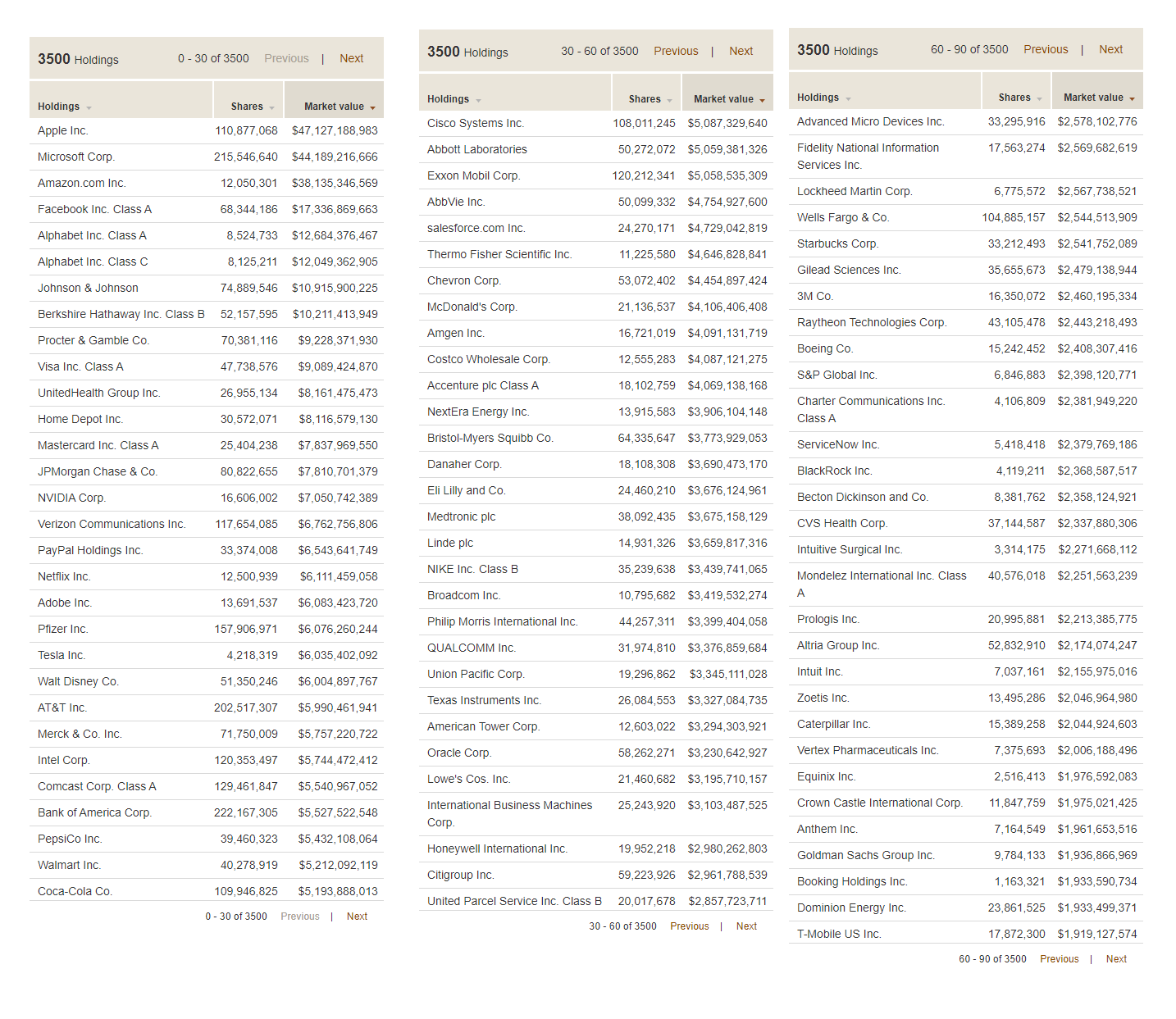

Well, this is all public information, and easily available with a quick Google search. For example, here’s a list of the top 90 holdings in VTI (click for larger):

As you can see, the biggest chunk of money is allocated to today’s tech darlings, because this index fund is weighted according to market value, and these are the most valuable companies in the US today.

Through a convenient coincidence, the total value of the VTI fund happens to be just under $1 trillion dollars, which means you can just throw a decimal point after the ten billions digit of market value to get a percentage. In other words, about 4.7% of your money will go towards Apple stock, 4.4 towards Microsoft, and so on. Together, these top 90 companies are worth more than the remaining 3,410 companies combined, so these are what really drive your retirement account.

And within this list, you will see some of the usual suspects: Exxon and Chevron (oil), Philip Morris (tobacco), Raytheon and Lockheed (bombs), and so on.

But what about the less-usual suspects? For example, I happen to think that sugar, and especially sugar-packed beverages like Coke, is the biggest killer in the developed world - a major contributor to 2 million of the 2.8 million deaths each year in the US alone. Should I exclude that from my portfolio too?

And what about drug and insurance companies - aren’t they behind the political stalemate and high costs of the US healthcare system? Comcast funded some election disinformation campaigns here in my home town in the early 2010s, should I exclude them too? And if you’re part of a religion that is against charging interest on loans, or in favor of pasta and Pirate costumes, or against a spherical Earth, or any number of additional ornate rules, you may have still more preferences.

The higher your desire for perfection, the more difficult this exercise will become. However, if you are like me and you just want to get most of the desired result with minimal effort, you might simply have a look at the Vanguard fund called ESGV.

ESG stands for “Environmental, Social and Governance”, and in practice it just means “We have tried to avoid some of the shittier companies according to some fairly simple rules.”

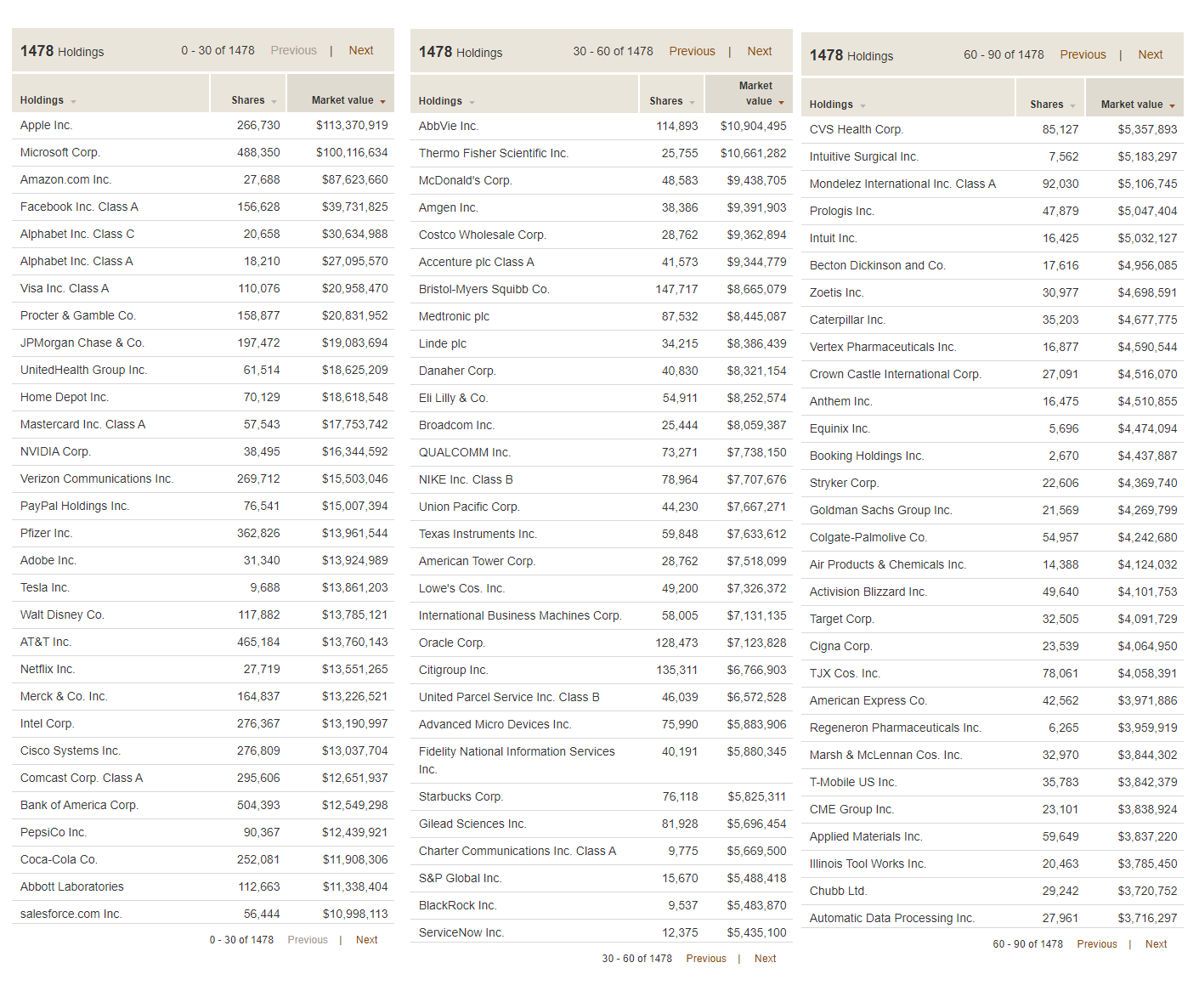

And the result is this:

The first thing you’ll notice is that it’s almost the same. In fact, the top five holdings - Apple, Microsoft, Amazon, Facebook, Alphabet (Google) and Netflix not far behind, collectively referred to as the FAANG stocks - are completely unchanged - and this means that there will be plenty of correlation between these funds.

It’s also the reason that the stock market as a whole has recovered so quickly from this COVID-era recession: small businesses like restaurants and hair salons have been destroyed by the shutdowns, but big companies that benefit from people staying at home and using computers and phones are making more money than ever. The stock market isn’t the whole economy, it’s just the publicly traded companies, which are the big ones.

But let’s look at the biggest differences between the normal index fund versus the social version.

The following large companies listed on the left are missing in the ESGV fund, in order of size. And to make up the difference, the stake in the companies on the right have been boosted up to take their place in your portfolio.

The omission of Berkshire Hathaway was a bit of a shocker, as it is run with solid ethical principles by Warren Buffett, one of the worlds most generous philanthropists. And in fact the modern day nerd-saint Bill Gates is on the Berkshire board of directors, another person whose work I follow and respect greatly.

(side note: Apparently the company fails on the “independent governance” category. And Buffett disputes this category, but in his characteristic way has decided to say, “Fuck it, I’ma just keep doing my own thing with my half-trillion dollar empire over here and you can have fun with your little committee” - I’m paraphrasing a bit but he totally did say that.)

Furthermore, both funds hold the factory meat king Tyson foods, while neither holds Roundup-happy Monsanto, because it was bought by the German conglomerate Bayer AG a while back. Nextera is a giant electric utility in the Southeastern US that claims to be the world’s largest generator of renewable energy. Some do-gooders are against nuclear power, while others (including me) think it’s the Bee’s Knees and we should keep advancing it. And all this just goes to show how nobody will agree 100% on what makes a good socially responsible fund.

But What About The Performance?

In the past, some investors were nervous about giving up oil companies in their portfolio, because while it was a dirty substance, it was also what made the world go round - which meant it was a cash cow.

Now, however, oil is on its way out as renewable energy and battery storage have crossed the cost parity threshold - meaning it’s cheaper to make power (and vehicles) that don’t use oil. In its place, technology is the new cash cow, and tech is heavily represented in the ESG funds. The result:

As you can see, the performance has been similar but the ESG fund has done significantly better in the (admittedly short) time since it was introduced at Vanguard.

Of course, we have no idea if this will continue, but the point is that at least our thesis is not a ridiculous one - environmentally sustainable companies do have an advantage, if the world gradually starts to care more about these things. And if you look at the share price of Tesla and other companies that surround it in electric transportation and energy storage, you will see that there are many trillions of dollars already lining up to benefit from this transition. And the very presence of so much investment money creates a self-fulfilling prophecy, as Tesla is now building or expanding five of the world’s largest factories on three continents simultaneously.

So What Should You Do? (and what I do myself)

First of all, it helps to remember a fundamental piece of economics: your spending dollars will probably have a much bigger impact than your investment dollars. This is because you are sending a direct message to the world rather than an indirect one:

When you buy a new gasoline-powered Subaru (or a tank of gas for your existing guzzler) or a steak at the grocery store, or a plane ticket, you are telling those companies directly that consumers want more of these products, so they will produce more of them immediately.

When you buy shares in Exxon, you are only subtly raising the demand for those shares, which raises the average price, making it ever-so-slightly easier for Exxon to maybe issue more shares in the future. In other words, you are making it easier for them to access capital. But capital is only useful if there is demand for their products. And with oil there is a nearly constant surplus, which is why OPEC and other cartels need to work together to artificially restrict supply, just to keep prices up.

Plus, as a shareholder you are theoretically eligible to place votes and influence the future direction of companies - even companies that you don’t like. If you look up the field of “shareholder activism”, you’ll see this is a tradition that goes way back.

So I have tried to take a few simple steps on the consumer side myself, and I find it quite satisfying: Insulating the shit out of all of my properties, building a DIY solar electric array on one of them, and buying one electric car so far to eliminate local gas burning. And a few electric bikes including a super fast one I made myself.

Each one of these steps has provided a very high economic return, percentage-wise, but that still leaves a lot of money to account for, which brings us back to stock investing.

As someone who loves simplicity, I have done this:

- Bought almost entirely VTI (or similar Vanguard funds) from 2000-2015

- Started experimenting with Betterment in 2015, liked it, and have been adding a percentage of my ongoing savings to that account to that since then. (Note that Betterment now also offers a socially responsible portfolio option.)

- Switched the dividend re-investing of my old Vanguard VTI over to Vanguard ESGV, to avoid “wash sales” in making the most of Betterment’s tax loss harvesting feature.

- Bought some shares of Berkshire Hathaway separately, and also make a few sentimental investments in local businesses, including the MMM HQ Coworking space.

But you could choose to be more hardcore in your ESG/SRI investing:

- Buy your own basket of stocks based on the index, but with different weighting based on your own values

- Spend more money on other things that generate or save money (a bigger solar array on your house, better insulation, electric car, an ebike to reduce car trips, etc.)

- Invest in local businesses of your choice, rental real estate, community solar projects, or other things which generate passive income - publicly traded stocks are just one of many ways to fund an early retirement!

Like most areas of life, investing is not something you have to do perfectly in order to succeed - even socially responsible investing. If you apply the 80/20 rule to get the big picture right, you have probably found the Sweet Spot and you can move on to the next area of life to optimize.

In the Comments:

What is your own investment strategy? Have you thought at all about this ESG / SRI stuff? Did this article bring anything new to the table?

Finance

Advice needed. I’m a cheapskate and I have a compulsive tendency to NOT SPEND any money at all.

I am 22M, single, and just recently finished college. I don't have a job yet, but I do have a part-time online gig that pays decently (compared to our country's minimum wage). I don't have a credit card, only a bank savings account and a prepaid debit card. Our family's socio-economic status is a little below middle-class for our country's standard, but we don't have any crippling debts and we have a comfortable savings.

I have this urge to avoid spending money at all costs. I only now realized that during my 5 years in college, I have never spent anything outside of the most critical necessities. I'm too cheap to even treat myself to a nice restaurant or some material items. It's not even about spending on "luxury" items like a brand new phone, laptop etc. Sometimes, I feel the need to not spend even on necessities like shoes, clothes, etc.

I only have two pairs of sneakers, one is my daily beater which I bought for like $40 and have worn for virtually every single day of my entire college life. By the time I finished college, it's already all beat up, the soles have already cracked and water is already able to seep in. Up to this day, I'm still wearing it and I'm determined to keep on wearing it until it splits into two (to be fair, I'm a small guy, so there's not much wear and tear happening). The other pair of sneakers I have, is something I received from my bigger cousin because his feet has outgrown it. It is still a little too big for me, so I only really wear it when my main beater is unavailable.

Same goes with my backpack. Until now, I'm still using the same Jansport that I had from high school. It has accumulated some lacerations throughout the years, but I just stiched and patched them up. The zipper failed at some point, which I brought to a seamstress for repair. I'm pretty sure people might mistake me for a homeless guy because of how beaten up my wardrobe is, but I don't give a care.

The laptop that we bought way back in 2011 is still my main daily driver up until now. It's replacement battery has long gone to shit and barely holds 30 minutes of charge, but it still does all the workload that I throw at it.

It's not only in real life that I have this compulsive need to avoid spending, even in free to play video games, I tend to hoard the in-game currency. I don't like seeing my gold numbers drop below an imaginary threshold that I have in mind.

During the past 6 months, the only thing that I have bought outside of necessities is a $20 headphone. Before I graduated college, family and some friends asked me what I want as a gift, I just told them "cash or anything would do".

I realize that I might have a problem and I need advice.

submitted by /u/seagullofwhite

[comments]

Source link

The following is a sponsored partnership with Aflac. All opinions are 100% my own.

Lately, I have received many emails from readers about life insurance.

One of the most common questions I hear is, “Should I consider a life insurance policy before I have children?”

No matter your age, the necessity of life insurance can be a hard topic to consider. However, while the subject might be difficult to reflect on, it is also an insurance option that can benefit your loved ones significantly, regardless of whether you have started a family.

Whenever I am asked the above question, my answer is always the same. Regardless of your family situation, life insurance is still a product to consider.

However, I understand the hesitation — you might think there is no reason to take out a life insurance policy if you don’t have children. September is Life Insurance Awareness Month, so it is the perfect time to talk about Aflac life insurance and why you may want it!

What is life insurance?

Before we begin, you may be wondering what exactly life insurance is.

Life insurance is a policy that pays money to a beneficiary you designate in the event of death. Naturally, if you are the sole or primary wage earner in your family, then there are a lot of people who rely on you financially, meaning life insurance may be a necessity.

The cash benefits can be used to help pay for funeral costs, personal expenses, payment of debt and so on.

The primary reason to get life insurance is to help your loved ones or anyone who depends on you in the event of a sudden loss of income after a death.

This way, they still have help paying the bills and grieve without having to worry about their immediate source of money.

When do you need life insurance?

Life insurance is not only for individuals who are the primary income earners of their household. Even if you are young, single and have no children, life insurance can still help support your loved ones. For example, a life insurance policy can support your family if you have co-signed loans with your parents (such as student loans), taken out a loan to start a small business or if you are financially responsible for another family member.

If you have co-signers on your debt, you should consider getting life insurance.

If something were to happen to you, you don’t want your co-signer (your parents, partner, siblings, friend, etc.) to be responsible for paying off your personal debt unexpectedly.

I can’t help but think of an article I read about a young adult who did not have life insurance. They passed away suddenly, leaving behind their student loan debt to their parents who co-signed the loan. They were suddenly responsible for monthly student loan payments of around $2,000 and had to entirely restructure their finances as a result.

If you have a partner, it is also important to consider the benefits of life insurance. If you have credit card debt, student loans, or if your partner relies on your income for rent or mortgage payment, a life insurance plan can help relieve those you care about from unnecessary financial burden.

Perhaps most importantly to note, life insurance is often cheaper while one is younger. By enrolling in a life insurance policy before you have children, you can typically secure a policy with lower premiums than when you are older.

If you plan on getting life insurance anyway, enroll early to ensure a more affordable rate.

Where do I find life insurance?

One popular life insurance company to look into is Aflac.

Aflac is a Fortune 500 company that provides supplemental insurance, including life insurance, to more than 50 million people through its subsidiaries in Japan and the U.S., where it is a leading supplemental insurer, by paying cash fast to help with the expenses health insurance doesn’t cover.

For consumers who place a premium on corporate ethics, Aflac is also a socially responsible company. For 25 years, Aflac has contributed over $146 million to help children facing cancer and their families, including establishing the Aflac Cancer and Blood Disorders Center in Atlanta.* If this interests you, then you can go to ESG.Aflac.com to explore how Aflac is dedicated to being a good and decent company.

If you are interested in learning more about insurance options that are available to you, I recommend heading to Aflac’s life insurance calculator, which allows you to identify how much coverage you need. You can see a screenshot of some of the questions below. It only took me about two minutes to answer the questions, and it offered a holistic overview of my personal benefit options.

Once you’ve answered the questions, it is easy to request a life insurance quote.

According to a 2019 Insurance Barometer Study by LIMRA, a worldwide research, consulting and professional development trade association, consumers think that life insurance is more costly than what it actually is. The study asked people to guess how much a $250,000 term life insurance policy costs for a healthy 30-year-old.

More than 50% estimated that it would be over $500 per year.

However, that’s very far from the truth.

The average cost of a life insurance plan is actually only around $160 a year, or $13 a month.

If you are interested in opting into a life insurance plan, $13 a month may make it an easy choice.

There are a lot of reasons why you may want to apply for life insurance, but remember that it makes sense to take one out early and save money in the long term.

I’d love to hear from you. Do you have life insurance? Why or why not?

*Aflac company statistic, 2020.

This is a brief product overview only. Coverage may not be available in all states. Benefits/premium rates may vary based on plan selected. Optional riders may be available at an additional cost. The policy/rider has limitations and exclusions that may affect benefits payable. Refer to the specified policy/rider form(s) for complete details, benefits, limitations, and exclusions. For availability and costs, please contact your local Aflac agent

Coverage is underwritten by Aflac | WWHQ | 1932 Wynnton Road | Columbus, GA 31999 | In New York, coverage is underwritten by Aflac New York | 22 Corporate Woods Blvd, Suite 2 | Albany, NY 12211

Z200625 Exp. 9/21

The post Should You Have Life Insurance If You Don’t Have Children? appeared first on Making Sense Of Cents.

Credit scores aren’t just a tool to determine loan and mortgage eligibility. Monthly point differences could define whether you’re offered better interest rates or stay in the shadows of less than ideal credit-based products. And checking your credit score periodically could improve not only your chances at landing a great mortgage rate or personal loan, but improve your long term financial health. Yet, 51% of Americans never check their credit score, according to a new survey conducted by The Simple Dollar.

Survey results

- We surveyed 879 American adults and found that over half say they never check their credit score.

- 39.7% of respondents say they periodically check their credit score (once a month or so)

- Credit checkers are rare in America, with only 8.6% of respondents saying they check their score more than once per month.

How often do you check your credit score?

!function(e,i,n,s){var t=”InfogramEmbeds”,d=e.getElementsByTagName(“script”)[0];if(window[t]&&window[t].initialized)window[t].process&&window[t].process();else if(!e.getElementById(n)){var o=e.createElement(“script”);o.async=1,o.id=n,o.src=”https://e.infogram.com/js/dist/embed-loader-min.js”,d.parentNode.insertBefore(o,d)}}(document,0,”infogram-async”);

The benefits of knowing your credit score

There are several benefits of knowing your credit score, mainly if you use credit frequently in your financial life (personal loans, credit cards, etc).

Saves you time on loan shopping

If you search for “personal loans,” you’ll find a deluge of financial products and websites promoting themselves. It’s tough to know what you’re actually qualified for without knowing the nature of your current credit score. Are those advertised rates only for very qualified buyers? Are you one of those?

Helps you prevent frauds

A credit report is often the first place fraud victims notice unusual activity being conducted in their name. With data breaches on the rise, the average American has had their data stolen at least four times in the past year. This means keeping an eye on the accounts opened in your name is more important than ever.

Creates a course for the future

If you have a low credit score or no credit history, checking your credit score periodically is a great way to stay on course for the future. You can set goals for yourself and watch as specific actions you take affect the score. When the time comes to get that business loan or student loan, you’ll know where you’re at now and where you need to be to qualify.

Allows you to qualify for emergency or personal loans

Sometimes we don’t know what the future will hold for our financial lives. You may not think you’ll need a personal loan in an emergency, but if you do, you’ll want to make sure your credit is in good shape. There could be fraud or inaccuracies on your record that prevent you from obtaining that loan in an emergency. Knowing your credit score can help make sure you have access to those types of loans at any time. That being said, even if you have poor credit, you could still obtain a loan.

Possible reasons for not checking your credit score

We spoke to several office mates, friends and family members about how they check their credit score. Anecdotally, the 51% non-checkers number held up within our circles. When asked why they don’t check their credit scores, here were some of the answers:

- “I don’t use credit cards or plan on taking on loans anytime soon.”

- “I already know I have horrible credit.”

- “Didn’t know it was that important”

- “My spouse does that stuff.”

Survey methodology

We surveyed 879 Americans over the age of 24 (conducted Aug. 26-31, 2020). Respondent’s age, location and gender data was also collected at the time, but we found no statistically significant differences worth noting in our report. The survey was conducted in conjunction with Google Surveys.

We welcome your feedback on this article. Contact us at [email protected] with comments or questions.

Image credit: Pavel Bezkorovainyi / Getty Images

The post Survey: Half of America Doesn’t Check Their Credit Score at All appeared first on The Simple Dollar.

Advice needed. I’m a cheapskate and I have a compulsive tendency to NOT SPEND any money at all.

How Do Delivery Robots Work? How They Safely Deliver Your Packages

6 Crucial Races That Will Flip the SenateThis November, we have…

Bernice King, Ava DuVernay reflect on the legacy of John Lewis

Heavy rain threatens flood-weary Japan, Korean Peninsula

Everything New On Netflix This Weekend: July 25, 2020

-

Business2 months ago

Business2 months agoBernice King, Ava DuVernay reflect on the legacy of John Lewis

-

World News2 months ago

Heavy rain threatens flood-weary Japan, Korean Peninsula

-

Technology2 months ago

Technology2 months agoEverything New On Netflix This Weekend: July 25, 2020

-

Finance4 months ago

Will Equal Weighted Index Funds Outperform Their Benchmark Indexes?

-

Marketing Strategies9 months ago

Top 20 Workers’ Compensation Law Blogs & Websites To Follow in 2020

-

World News8 months ago

World News8 months agoThe West Blames the Wuhan Coronavirus on China’s Love of Eating Wild Animals. The Truth Is More Complex

-

Economy11 months ago

Newsletter: Jobs, Consumers and Wages

-

Finance10 months ago

Finance10 months ago$95 Grocery Budget + Weekly Menu Plan for 8