Finance

Here’s What You Should Do Before You Refinance Your Home

Now could be one of the best times to refinance your mortgage over the next ten or twenty years. Mortgage rates are nearing record lows thanks to “declining inflationary pressures,” according to Freddie Mac’s chief economist Sam Khater. At the same time housing prices are not suffering like other parts of the economy right now, mostly due to demand.

These factors have created a situation where you can potentially refinance your home using its new, higher value and get cash out in the process. You can also refinance to save money on interest, move into a lower monthly payment, or both.

Should you refinance the mortgage on your home? The answer depends on an array of factors as well as whether you have the time and energy to devote to the process. But if you do decide to refinance your home, you should also keep in mind that the steps you take now could leave you in a better position later on.

What You Need to Know About Refinancing Right Now

- As of July 2020, mortgage rates for a 30-year home loan can be as low as 2.75% APR. This makes refinancing your mortgage an attractive proposition if your current interest rate is at least half a percentage point higher than that.

- Approval requirements for a mortgage can vary from lender to lender, but an array of sources seem to indicate that lenders are making it slightly more difficult to qualify. This can mean tightened credit requirements and more money down. For example, Chase now requires 20% down and a credit score of at least 700 to qualify for one of their mortgage loans, per a news release from HousingWire.

- While requirements may be somewhat tighter overall, technology has made it easier than ever to shop around for a mortgage. You can compare quotes online and complete the entire refinancing process from the comfort of your home. Some mortgage refinance companies will even send a representative to close your home loan in person.

Steps to Take Before You Refinance Your Mortgage

If you believe you may be eligible to refinance your mortgage right now, there are steps you can take to prepare your finances and make sure you can qualify for the best rates and terms. Here’s everything you need to do before you move forward and apply.

Step 1: Check your credit score.

With many lenders tightening their credit requirements for mortgage refinancing, having an idea of your credit score can help you prepare. You may find your score is better than you think, or you may find that it needs some work. Either way, you’ll never know unless you check.

If you don’t have a credit card that offers a free credit score on your monthly statement, you can sign up for a free account with Credit Karma or Credit Sesame to see where you stand. Both require some basic personal information to get started, but you’ll get access to at least one version of your credit score as well as credit-tracking tools.

Step 2: Get your finances in order.

When you apply for a new mortgage or a refinance, several aspects of your personal situation are considered. For the most part, this includes your credit score, your history of employment, your income, your down payment amount, and the amount of debt you have in relation to your income.

Saving up a considerable down payment may not matter as much for a refinance, but you may be able to qualify for better mortgage rates and terms if you keep your credit in great shape and keep your debt-to-income ratio on the lower end.

Generally speaking, lenders prefer to approve borrowers with a debt-to-income ratio of 43 percent or below, meaning your monthly debt payments make up less than 43 percent of your gross monthly income. If you earn $10,000 per month, for example, your monthly debt obligations would be less than $4,300 each month if you hoped to meet this standard.

Step 3: Compare mortgage rates.

The mortgage refinancing business is highly competitive, but that doesn’t mean all lenders can offer the best rates to every consumer. Your best bet is shopping around among several different lenders to see which one might offer you the lowest rate based on your credit profile, your income, and where you live.

Step 4: Choose a lender and start the process.

Once you’ve found a lender who appears to offer the best rates and terms based on your situation, you can move forward with them by filling out a full loan application.

However, you may want to spend time comparing estimates from more than one lender, and potentially getting a Loan Estimate from each. This simple document includes the loan terms, how much you’ll owe each month, and the estimated closing costs you’ll be expected to pay to refinance. Getting a Loan Estimate from multiple lenders is the best way to shop around and make sure you’re not overpaying for fees or settling for a new loan with inferior terms.

Once you decide to move forward with a lender, you’ll want to lock your interest rate so you are no longer at the mercy of the market. The goal at that point will be closing your loan before your locked rate expires, which should be doable since mortgage mortgage refinance loans take 30 to 45 days to complete.

Once you fill out a loan application, you’ll typically need to supply your lender with information required for your home loan. This usually includes two years of tax returns, at least one month of pay stubs, further proof employment or an explanation for any employment gaps, 60 days of bank statements, and proof of any other income you have.

Step 5: Prepare your home for the appraisal.

Part of the refinance process involves getting an appraisal for your home. After all, you need to be able to prove how much your property is worth before a lender will let you trade out your current home loan for another.

Whether your goal is refinancing to get a lower monthly payment or to get cash out, you’ll want to make sure your home is in tip top shape for appraisal purposes. Steps you should take include repairing any obvious damage to your home, sprucing up the indoors and outdoors for a clean, updated look, and cleaning your entire property inside and out. Also make a list of updates you’ve made to your home that could help an appraiser reach a higher value. If you’ve replaced your HVAC system or your roof, for example, you should tell your appraiser about these improvements.

Refinancing Your Home: Frequently Asked Questions (FAQs)

Refinancing the home you love? These frequently asked questions can help you learn more about the process.

The purpose of refinancing your home varies from borrower to borrower. However, many consumers refinance their home loans in order to secure a lower interest rate that will help them save money. Others want to get a new loan with a lower monthly payment, and homeowners also refinance in order to switch up the term of their home loan — for example, moving from a 30-year loan to a 15-year mortgage.

You typically need to wind up with at least 20 percent equity in your home after a refinance if you hope to avoid paying private mortgage insurance, or PMI. Many lenders will allow you to refinance with less than 20 percent equity, however, although equity requirements can vary depending on the bank.

You can apply for a mortgage online and from the comfort of your home, and this is also true if you plan to refinance a mortgage you already have. Many lenders allow you to upload the mortgage refinance documents online, and some will even close the loan at your home address or any other place of your choosing.

Generally speaking, you’ll need a credit score of 620 or higher for a conventional mortgage refinance. However, COVID-19 has left many individual lenders with no choice but to tighten up their standards, which means some lenders may require a score of 700 or more. Government programs like VA home loans and FHA loans tend to come with more lenient credit score requirements, so make sure to check on these options if you believe you could qualify.

When you close on your mortgage refinance, you’ll pay many of the same fees you paid when you took out your mortgage to begin with. Fees you’ll need to pay include credit report fees, title fees, escrow fees, notary fees, and recording fees. You will also need to pay an appraisal fee and lender fees that cover processing and underwriting. If you’re paying points on your mortgage in order to secure a lower rate, the cost of each point is typically equal to 1% of your new loan amount.

The Bottom Line

If you’re paying a higher rate than the lowest rates advertised right now and your finances are in relatively good shape, you really have nothing to lose by checking mortgage rates to see if refinancing could be worth it. If you were willing to put in the effort to apply and gather all the documentation required, you could easily save thousands of dollars in interest payments on your loan, pay off your mortgage faster, or both.

But it all starts with shopping around among mortgage lenders online and in your area. Since interest rates may not stay this low forever, the time to start shopping around is now.

The post Here’s What You Should Do Before You Refinance Your Home appeared first on Good Financial Cents®.

Updated. I’m still collecting points and miles and maximizing the value of my credit card spending. Things are more quiet as credit card issuers get conservative, but that just means picking up some bonuses that I passed over previously.

That space in your wallet or purse is still valuable, and you should be the one to get that value. Selected banks are offering strong perks and $500+ value for a single card during the first year to encourage you to apply and try it out. These are the top 10 credit card offers that I would personally apply for right now, if I didn’t already have most of them. Notable recent changes:

- Added Southwest, United, Marriott, US Bank Altitude

- Added COVID Sapphire benefits.

- Removed IHG, NavyFed.

If you pay off your balances every month, then you can join me and many others in funding a huge chunk of your annual travel budget with cash credits, points, and miles. You don’t need to be a “I only fly business class” world traveler. I mostly use my rewards points on domestic economy flights, mid-range hotels, and cheap car rentals. If you have credit card debt, you should focus on paying that off first as the interest charges could offset most of the perks.

This is a companion post to my Top 10 Best Business Card Offers. Small business bonuses are on average even higher than those on consumer cards.

Note: Certain Chase cards have a “5/24 rule” which is an unofficial rule that they will automatically deny approval on new credit cards if you have 5 or more new credit cards from any issuer on your credit report within the past 2 years. This rule applies on a per-person basis, so if you are new, you might want to start with those Chase cards.

- 60,000 Ultimate Rewards points (worth $750 towards travel) after $4,000 in purchases within the first 3 months. See link for details.

- Short-term COVID-related benefits.

- 2X points on Travel and Dining at restaurants worldwide.

- $95 annual fee.

- Subject to 5/24 rule.

- Alternative: Chase Sapphire Reserve Card. 3X on Travel and Dining, Priority Pass airport lounge access, $550 annual fee, $300 annual travel credit, 1-year Lyft Pink membership.

Southwest Rapid Rewards Plus Card

- 65,000 Rapid Rewards points. Earn 65,000 points after $2,000 in purchases in first 3 months.

- Southwest still gives everyone two free checked bags.

- More than halfway to Companion Pass. If you can sign up for this one and also the small business version, you can qualify for a Companion Pass in 2020/2021.

- $69 annual fee.

- Subject to 5/24 rule.

- 60,000 bonus United miles. 60,000 miles after $3,000 in purchases within 3 months. Limited-time offer. See link for details.

- Free first checked bag for both you and a companion (a savings of up to $120 per roundtrip) when you use your Card to purchase your United ticket.

- Expanded award availability. Having this card makes it easier to find that saver award economy ticket.

- Up to $100 Global Entry or TSA PreCheck fee credit.

- $0 annual fee for the first year, then $95.

- Subject to 5/24 rule.

Gold Delta Skymiles Card from American Express

- Bonus varies. Enter your Delta Skymiles number and last name to see if you are targeted for a special offer.

- 50,000 Skymiles are worth at least $500 in Delta airfare with “Pay with Miles” option.

- First checked bag free on Delta flights ($60 value per roundtrip, per person). Main Cabin 1 Priority Boarding.

Citi / AAdvantage Platinum Mastercard

- 60,000 American Airlines miles after $3,000 in purchases in the first 3 months. See link for details.

- First checked bag free on domestic AA flights ($60 value per roundtrip, per person).

- $0 annual fee for the first year, then $99.

Marriott Bonvoy Boundless Card

- 100,000 Marriott Bonvoy points after $3,000 in purchases within the first 3 months. Limited-time offer. See link for details.

- Free Night after each account anniversary year (valued up to 35,000 Marriott points).

- $95 annual fee.

- Subject to 5/24 rule.

- 60,000 TrueBlue points after $1,000 in purchases within the first 90 days. Limited-time offer. See link for details.

- Free first checked bag for you and up to 3 companions when you use your JetBlue Plus Card.

- $99 annual fee.

Barclays AAdvantage Aviator Red World Elite Mastercard

- 60,000 American Airlines miles after any purchase in the first 90 days and paying the $99 annual fee. See link for details.

- $99 Companion certificate offer. Earn a certificate good for 1 guest at $99 (plus taxes and fees) after making your first purchase and paying the $99 annual fee in the first 90 days.

- First checked bag free on domestic AA flights ($60 value per roundtrip, per person).

- $99 annual fee.

- 60,000 points (worth $750 towards travel booked at ThankYou.com) after $4,000 in purchases in the first 3 months. See link for details.

- 3X points for every $1 spent on travel including gas stations.

- Must not have gotten bonus from or closed a Citi Rewards+, ThankYou Preferred, Premier, or Prestige card in the past 24 months.

- $95 annual fee.

Bank of America Premium Rewards Card

- 50,000 points (worth $500 towards travel) after $3,000 in purchases within the first 90 days. See link for details.

- 2 points for every $1 spent on travel and dining purchases and 1.5 points for every $1 spent on all other purchases.

- $100 annual Airline Incidental Statement Credit.

- Up to $100 credit towards TSA PreCheck or Global Entry application fee.

- $95 annual fee.

Hawaiian Airlines World Elite MasterCard

- 50,000 Hawaiian miles after $2,000 in purchases within 90 days. See link for details.

- Free first checked bag for primary cardmember when using your card to purchase eligible tickets directly from Hawaiian Airlines.

- Receive a one-time 50% off companion discount for roundtrip coach travel between Hawaii and The Mainland on Hawaiian Airlines.

- $99 annual fee.

U.S. Bank Altitude Reserve Credit Card

- 50,000 bonus points ($750 value towards airfare) after $4,500 in purchases within 90 days. See link for details.

- $325 in annual statement credits towards travel per Cardmember year (based on account opening date)

- Up to $100 statement credit for Global Entry or TSA PreCheck.

- Priority Pass Select membership for airport lounge access.

- $400 annual fee. (Bigger bonus, big annual fee.)

- Up to 50,000 Hyatt points. 25,000 Bonus Points after $3,000 in purchases in the first 3 months. Plus an additional 25,000 Bonus Points after a total of $6,000 in purchases within the first 6 months. See link for details and rough valuation of points.

- $95 annual fee, free night award upon card anniversary.

- Subject to 5/24 rule.

“The editorial content here is not provided by any of the companies mentioned, and has not been reviewed, approved or otherwise endorsed by any of these entities. Opinions expressed here are the author’s alone. This email may contain links through which we are compensated when you click on or are approved for offers.”

Top 10 Best Credit Card Bonus Offers - August 2020 (Updated) from My Money Blog.

Copyright © 2019 MyMoneyBlog.com. All Rights Reserved. Do not re-syndicate without permission.

A PAN Card is a 10-digit alpha-numeric unique code issued by the Income Tax Department of India to file the Income Tax Returns or to make banking transactions exceeding Rs. 50,000. Moreover, a PAN Card is also considered as one of the important identification documents for opening a bank account, purchasing a property, investing in mutual funds, applying for a debit/credit card and more.

According to the Union Government of India, it is now mandatory for all the individuals to link their Aadhaar Card with a PAN Card and failure to do the same will result in an inoperative PAN Card. You will also be fined Rs. 10,000 for using an inoperative PAN Card under the Section 272B of the Income Tax Act. The deadline for linking PAN with Aadhaar has been extended to 31st March 2021.

However, getting a PAN Card has now become quite easy as compared to the offline procedure which was lengthy, paper-heavy and tedious. You can instantly get your PAN Card Application through an Aadhaar Card. It is worth mentioning that in order to avail this facility of getting an instant PAN Card through Aadhaar Card, your mobile number must be registered with Aadhaar to generate One Time Password(OTP) for the verification.

This facility of instant and free PAN Card through Aadhaar based e-KYC has been recently launched by the Finance Minister of India , Nirmala Sitharam on 25th June 2020.

Let us now understand what are those five important things for instant PAN Card Application using Aadhaar Card.

Process of Instant PAN Card through Aadhaar Card

You must know the steps involved for availing Instant PAN through Aadhar Card. The steps are as follows:

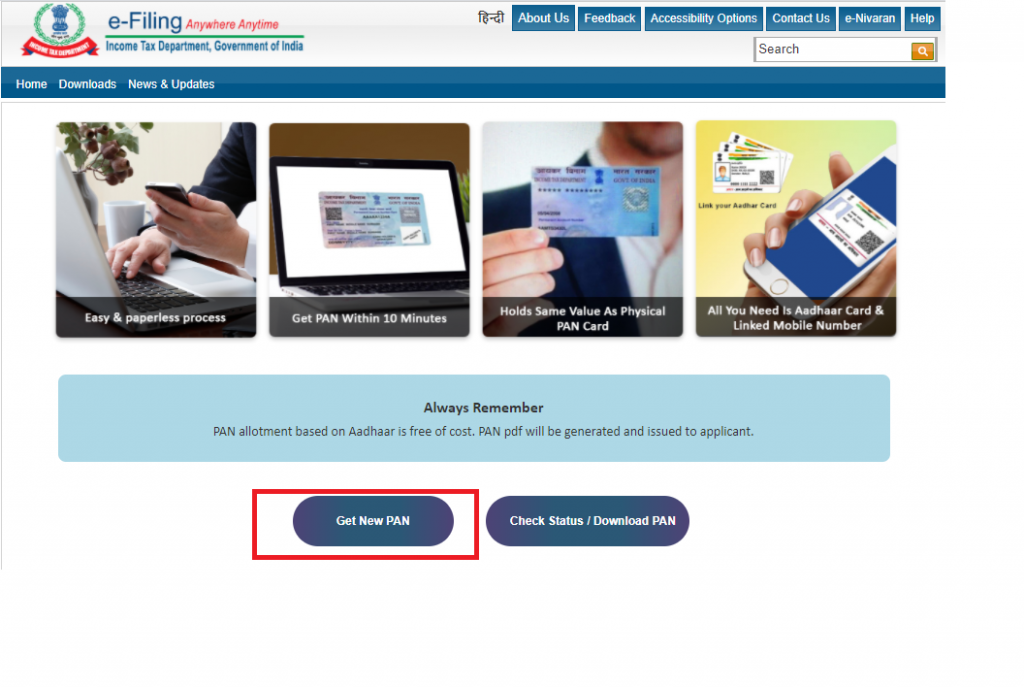

Step 1: You have to visit the official website of the Income Tax Department at https://www.incometaxindiaefiling.gov.in/e-PAN/

Step 2: Click on the ‘ Get New PAN’ option

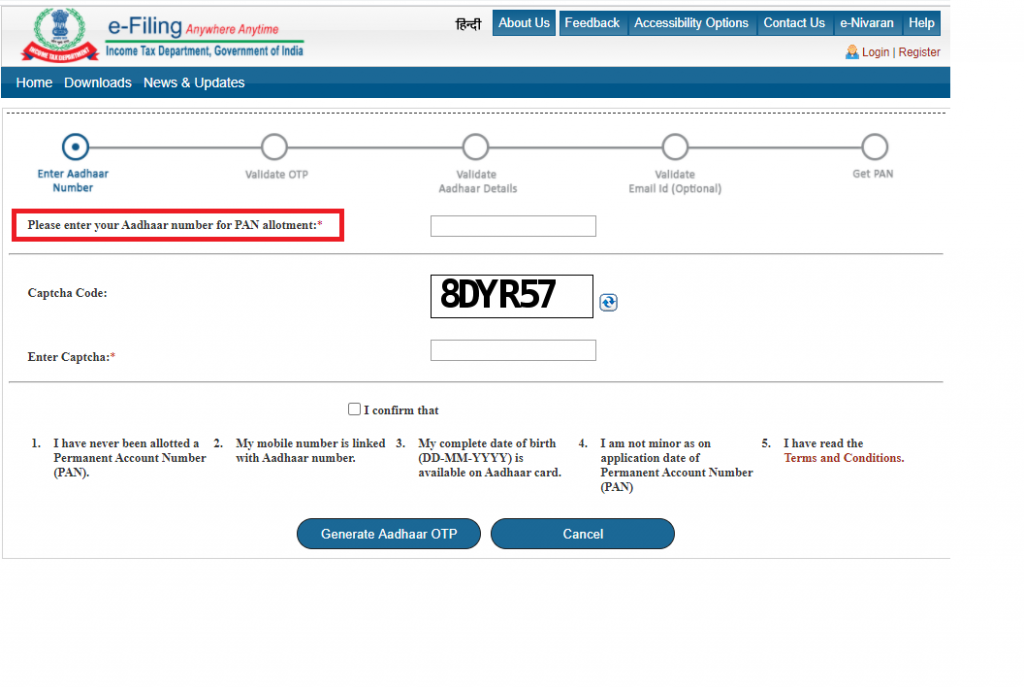

Step 3: You will be redirected to a new page. Enter your 12-digit Aadhaar Number for PAN allotment

Step 4: Enter the ‘Captcha Code’ for verification

Step 5: Now, you need to confirm the following details:

-

- I have never been allotted a PAN Card

- My mobile number is linked with Aadhaar number

- My complete date of birth is available on the Aadhaar Card (DD/MM/YY)

- I am not minor as on application date of Permanent Account Number (PAN)

- I have read the Terms and Conditions

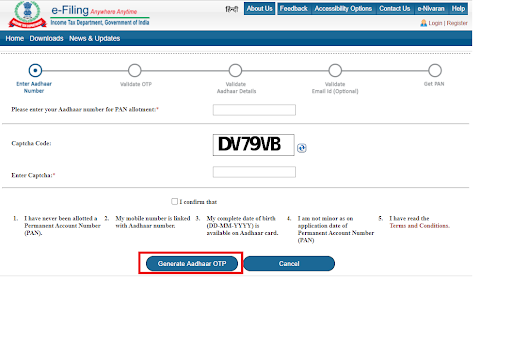

Step 6: Once done, click on the ‘Generate Aadhaar OTP’ button

Step 7: You have to enter the OTP be sent on your registered mobile number

Step 7: You have to enter the OTP be sent on your registered mobile number

Step 8: You have to validate your Aadhaar details, your email address (optional)

Step 9: Once all the details will be validated from the database UIDAI, your e-PAN will also be sent if the email ID of the applicant is registered with Aadhaar

Note: You will receive a 15-digit acknowledgement number for further tracking of PAN Card Status

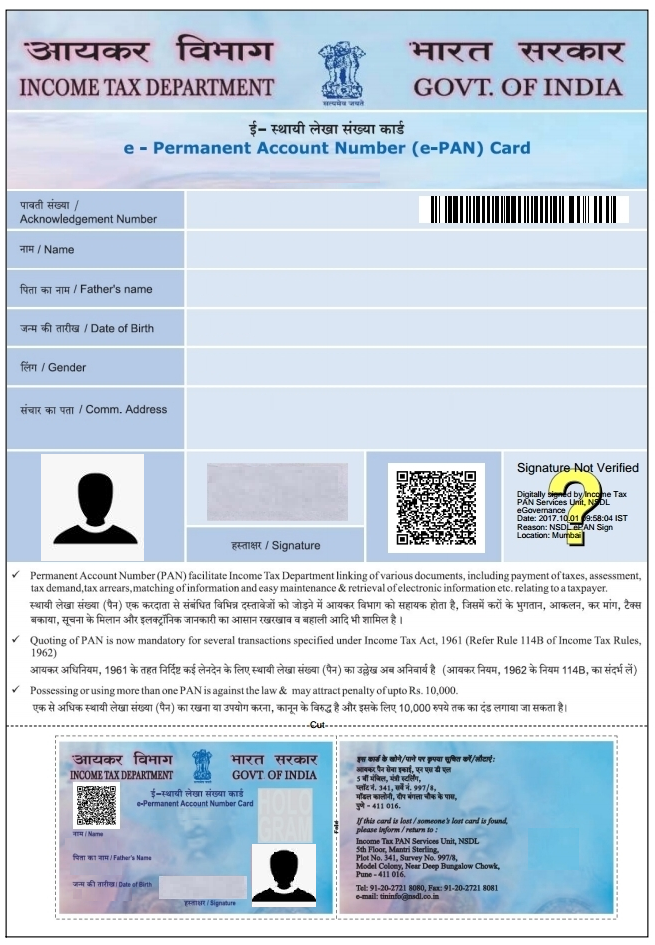

Format of of Instant PAN Card facility through Aadhaar based e-KYC

The issued instant PAN Card is in the format of pdf which also has a QR code containing all the demographic information such as your name, date of birth, gender and the photograph too. Morerver, this instant e-PAN can be downloaded through the 15-digit acknowledgement number sent to you once the process of PAN Card application is completed on your registered mobile number and email address. Moreover, you will also be sent a soft copy of your PAN Card on your email address (if registered with Aadhaar Card).

Note: Sometimes, the applicants get confused whether the e-PAN is considered equally valid or not, but as per the recent rules of the Income Tax Department of India, the e-PAN is equivalent to a laminated PAN Card.

Charges for Instant PAN Card through Aadhaar Card

You can also get your PAN Card through the official website of NSDL and UTIITSL, but both these PAN Card issuing authorities charge for the PAN Card application whereas the issuing of a 10-digit alphanumeric number is free of cost at the Income Tax Department’s portal.

Read more at: PAN Card Fees and Charges

Documents Required for Instant PAN Application

There is no documentation required for the Instant PAN Application facility through Aadhaar Card as the data will be automatically fetched from the database of the Unique Identification Authority of India (UIDAI) once you enter your Aadhaar number.

The income tax department says the turnaround time for issuing an instant PAN is just about 10 minutes. So far more than 6.7 lakh such instant PAN cards have been issued.

How to Check Status of Instant PAN Application

You can also check the status of your Instant PAN Application by following the steps mentioned below:

Step 1: Go to the official e-filing home page of the Income Tax Department (https://www.incometaxindiaefiling.gov.in/home)

Step 2: Click on the ‘Instant PAN through Aadhaar’ option under the ‘Quick Links’ section on the homepage which will redirect you to the instant PAN allotment webpage

Step 3: Now, you need to select the ‘Check Status/Download PAN’ option

Step 4: Enter your Aadhar number and captcha code

Step 5: Click on the ‘Submit’ button

Step 6: You have to validate the OTP which will be sent to your registered mobile number. Once again click on the ‘Submit’ button

Step 7: A new page will appear on your screen to check the status of your Instant PAN Card Application

Step 8: Upon successful approval of your PAN Application, you will receive a PDF link within ten minutes to download the PAN

Note: The PDF which will be generated will be password protected and you need to use your date of birth in the format ‘DDMMYYYY’ as the password to open the PDF file.

The post Instant ePAN Card using Aadhaar Card: 5 Things to Know appeared first on Compare & Apply Loans & Credit Cards in India- Paisabazaar.com.

(The following is a transcription from a video Linda and I recorded. Please excuse any typos or errors.)

All right. Today, we’re talking about 10 incredibly useful hacks to stick with your budgets. And, I’m really excited to share them with you.

We have really honed in on what it takes to have a budget that you can enjoy, that makes you feel good about life.

We’ve done it wrong so much that we’ve just learned how to do it right, and how to have fun in the process.

If you haven’t gotten Our Free Budgeting Worksheet, I’ve spent a lot of time making this thing and I think it’s awesome.

It’s a good first step to see how your income and expenses stack up. It’s just a good way to get started with your budget.

You can just pick that up by clicking here, and you’ll be on your way to starting your budget!

Now let’s get to these 10 amazing hacks to help you stick with your budget…

10. Make Savings Automatic

Bob: One of the biggest mistakes that most people make is they spend their money and then they try to save or give afterwards. You have to do it the opposite way, the things that are most important to you: giving money, savings, whatever those are, that needs to come first. If you don’t do it that way, if you don’t have some automatic thing in place, the reality is, we all know this.

Linda: It’s not going to happen.

Bob: We all know this, it’s probably not going to happen. You’re going to get to the end of the month, there’s not anything there. And so, that’s why making it automatic is incredibly important.

9. Reward Yourself

Bob: Or if you’re a Parks and Recreation fan, we could call it, treat yo self.

Linda: Treat yo self. This comes across though, as like, “I’m just going to treat myself all the time,” which is something I would do, but we’re not talking about that. Right?

Bob: Yeah. But the key in terms of sticking to your budget, you need rewards. You need incentives to stay the course. And so, yeah, when we were paying off our debt, this was a big part of that. Our budget was a big piece of us being able to pay off our debt. But in order to reach that goal, we had to have milestones. It was too big of a thing, it was too much, it was too long of a road for us to walk without some rewards. And so, we made sure to keep them in there and because we did, we were able to stick with it. Right?

Linda: Yeah. And I think this was especially key for me because he was watching the numbers of our debt go down, down, down. And he was really, really involved. But for me, I was more on the sidelines. And if I wouldn’t have had this incentive, it would have been really difficult for me to keep going. I think I would have just gotten discouraged and given up. So, I think this was extremely key for me since I was not as involved.

Bob: Yeah. Definitely.

8. Budget With Accountability

Bob: I’ve had the unique advantage of being able to try out and test out a whole bunch of different budgeting methods, budgeting softwares and tools and spreadsheets, and all this stuff over the years. I’ve been a financial blogger for almost 13 years, and I have reviewed almost everything out there, and I’ve tried out so much of the stuff. Because we’ve actually tried it ourselves.

The thing that I’ve come to realize is that most budgeting methods don’t actually hold you accountable. There’s this false sense of accountability. And so, the only tool that I’m aware of that ever actually hold you accountable are cash envelopes, if you do that and put cash in envelopes and do that type of budgeting.

Linda: Yeah. And that wasn’t going to work for us because we use plastic sometimes because we online shop or whatever.

Bob: Yeah. Then the other option is The Real Money Method. And this is kind of our hack to do that, to have a budgeting method that actually holds you accountable. So, we have an entire course teaching this method in which you’re welcome to check out if you’re interested. But the bottom line is that for most of us to stick with a budget, we need accountability. We need a budget that’ll hold us accountable. And so, if you’ve ever failed with budgeting, this might be the reason why. So, just find something that will hold you accountable.

7. Don’t Save Your Credit Card Info On Any Site Where You Shop

Bob: This is a good hack. This, yeah, because adding that friction, I think that would definitely, yeah. It just doesn’t seem like much, but having to spend the extra minute or two to go through with the purchase to type all that in, it just slows you down.

Linda: All right. So, I think you’ve told me about this before, where there’s something almost physical that happens in your body when you pay for something and you have to hand over cash.

Bob: Because it’s just real money and you get to feel it.

Linda: Yeah. And you’re like, “There’s my money and it’s leaving.”

Bob: It’s disappearing, yeah.

Linda: But when you write a check, you told me it’s less, but it’s still more of a process that you still feel like…

Bob: A little bit less real, yeah.

Linda: And then, less when you are swiping your credit card.

Bob: Yeah.

Linda: I think you told me this years ago, really before online shopping was as big as it is now. And I can only imagine how little you feel that when it’s like click, click, and it’s, “I bought it.”

Bob: Yeah.

Linda: It’s done.

Bob: I mean, that’s what Amazon has done. It’s like literally-

Linda: Oh, my gosh.

Bob: Add To Cart, boom. Done.

Linda: Well, and you can even hit Buy It Now. And it’s like click, you’re done.

Bob: Yeah. You’re right. It’s one click. So, it’s brilliant on their part. But the point is, is that adding that friction will overall reduce the spending that we make. So yeah, it’s an important move to make.

6. Only Use Gift Cards To Shop On Amazon

Linda: Number six ties right into what we were just talking about. Only use gift cards to shop on Amazon.

Bob: This is an interesting idea that the author had to basically go to the grocery store, buy an Amazon gift card for $100 or whatever, and then load that on your account and then make purchases with that. And so, this kind of takes that friction to a whole new level in that you need to go to the store and buy an Amazon gift card. But at the same time, it kind of undoes the previous thing we were just talking about because the gift card is loaded in there and it’s still pretty easy to buy. So, it’s kind of like, yeah, I don’t know. It might work for some people, but something to consider.

5. Never Buy Anything That You Put In An Online Shopping Cart Until The Next Day

Linda: Number five, never buy anything that you put in an online shopping cart until the next day.

Bob: This is a good idea. I can’t tell you how many times I’m struggling with some annoying problem around the house and I need to go buy this. I’m like, “I need to go buy this thing to fix it,” whatever it is. And I’ll put the thing in a cart and just because I forget to go buy it and I’ll come back a couple of days later, I’m like, I actually solved that problem already. Or it’s not even that big of a problem. It seemed like a big problem in the moment, but it really isn’t that big of a problem. And it is amazing. We’ve all heard this, just sit on a purchase for a little bit and then, half the time, you don’t want to make it later on. But I like this idea of throwing it in the cart. That way, you won’t forget about it. And you can check in a couple of days.

Linda: Yeah.

Bob: And see.

Linda: Well, and I think this is really key for stuff that you just want.

Bob: Yeah, especially.

Linda: Because I mean, so many times, you’re just trying to numb yourself. You’re like, “I’ve had a bad day, so I’m going to go online shop.” And I know that’s what I do. So, just sitting on that, having it in your cart kind of gives you a little bit of satisfaction, and then being able to sit on it for a little bit, I think really helps. And then you can make a decision when you’re a little bit more clearheaded.

Bob: Yeah.

4. Read The One-Star Reviews For The Products Before You Buy Them

Linda: Okay, I really like this one. Read the one-star reviews for the products before you buy them.

Bob: This is a great idea. Because it definitely gives you a whole different perspective on the product.

Linda: Yeah.

Bob: And yeah, and you just might not be as interested when you see all the negative things about it.

Linda: Right.

Bob: Now, I do this for really, most products I buy, because I want to see what people are saying the bad is.

Linda: Yeah. You don’t want to buy a product that’s going to be terrible and it’s not what you want.

Bob: Well, yeah, if you have 20 people in a row saying that whatever, “it stopped working after three months,” it’s like, all right, there might be a trend here. So, just from a smart shopping perspective, I think this is good, but it also will help you. Yeah, I think it will deter you from buying more things if you’re looking at the bad.

3. Don’t Go To The Grocery Store Hungry

Linda: All right. Number three, this one is classic.

Bob: But it works. It works.

Linda: Don’t go to the grocery store hungry.

Bob: Yeah. It just really, really works. It’s such a big difference when you, yeah, when you’re…

Linda: When you’re full and you’re not hungry.

Bob: Yeah.

Linda: You should go to the grocery store only full. It’s where you’re just like, “None of this sounds good.”

Bob: No, this is what you should do. You should go to the grocery store after a Thanksgiving meal, when you’re so bloated and just be like, “I don’t want any food.” You’re tired. That’s when you go to the grocery store.

Linda: You won’t be buying much. But then, you’ll regret it later because you’ll be like, “Why is there no food in the house?”

2. Only Make Major Purchases In The Morning

Linda: Number two, only make major purchases in the morning.

Bob: Yeah. I think this is really interesting. I remember, I think Tim Ferriss was talking about decision fatigue, and this idea that we only have a limited number of decisions that we can make any given day. And after that point, we’re just tapped out and we can’t actually make any more decisions.

Linda: Yeah.

Bob: And so, what happens is, so many of us in busy lives, we get to the end of the day and we’re just worn down and we don’t have good decision-making abilities. Whereas at the beginning of the day, we’re fresher. And we have, if you think of it in terms of a bank account, we have a lot more decisions sitting there that we can tap into. So, making these purchases, especially big purchases in the morning when we’re stronger, it’s just a better approach.

1. Choose A Major Category Each Month To Attack

Linda: Okay. Number one, choose a major category each month to attack.

Bob: I think this is a good idea. I think too many people try to solve 10 problems at once. And I think focusing your energy on just one, find one category in your budget that you’re struggling with, even though you might be struggling with four or five of them, find one, focus your energy on solving that particular one, whatever that is. If it’s groceries, if it’s household goods, whatever that category is, try to solve that one.

Linda: Yeah. And we’ve talked about this before, where you should not base your budget around what your personal goals are. You need to base it around where you actually are in your life. So, if you were going to Starbucks every day and you want to change that, do that one month. And then, once you’ve got that down, work on the next habit. Don’t try and do it all at once, because you’re going to blow your budget. It’s not going to work. And you’re just going to be mad.

What Budgeting Tip Would You Add To This List?

Yeah. So, those are our top 10. I’d love to hear yours in the comments.

Don’t Forget The Free Budgeting Worksheet!

Like I mentioned at the beginning, if you are new to budgeting, or if you just need a little help, be sure to get our free budgeting worksheet.

Source article that inspired this video/article: 13 incredibly useful budgeting hacks to help you stick to your budget.

-

Business4 weeks ago

Business4 weeks agoBernice King, Ava DuVernay reflect on the legacy of John Lewis

-

World News3 weeks ago

Heavy rain threatens flood-weary Japan, Korean Peninsula

-

Technology3 weeks ago

Technology3 weeks agoEverything New On Netflix This Weekend: July 25, 2020

-

Finance3 months ago

Will Equal Weighted Index Funds Outperform Their Benchmark Indexes?

-

Marketing Strategies7 months ago

Top 20 Workers’ Compensation Law Blogs & Websites To Follow in 2020

-

World News7 months ago

World News7 months agoThe West Blames the Wuhan Coronavirus on China’s Love of Eating Wild Animals. The Truth Is More Complex

-

Economy10 months ago

Newsletter: Jobs, Consumers and Wages

-

Finance8 months ago

Finance8 months ago$95 Grocery Budget + Weekly Menu Plan for 8