Finance

Introducing Coverage Critic: Time to Kill the $80 Mobile Phone Bill Forever

A Quick Foreword: Although the world is still in Pandemic mode, we are shifting gears back to personal finance mode here at MMM. Partly because we could all use a distraction right now, and even more important because forced time off like this is the ideal time to re-invest in optimizing parts of your life such as your fitness, food and finances.

Canadian Readers - we have also collected some recommendations for you at a new Canadian Mobile Phone recommendations page.

—

Every now and then, I learn to my horror that some people are still paying preposterous amounts for mobile phone service, so I write another article about it.

If we are lucky, a solid number of people make the switch and enjoy increased prosperity, but everyone who didn’t happen to read that article goes on paying and paying, and I see it in the case studies that people email me when looking for advice. Lines like this in their budget:

- mobile phone service (2 people): $160

“NO!!!!”

… is all I can say, when I see such unnecessary expenditure. These days, a great nationwide phone service plan costs between and $10-40 per month, depending on how many frills you need.

Why is this a big deal? Just because of this simple fact:

- Cutting $100 per month from your budget becomes a $17,000 boost to your wealth every ten years.

And today’s $10-40 phone plans are just great. Anything more than that is just a plain old ripoff, end of story. Just as any phone more expensive than $200* (yes, that includes all new iPhones), is probably a waste of money too.

So today, we are going to take the next step: assigning a permanent inner-circle Mustachian expert to monitor the ever-improving cell phone market, and dispense the latest advice as appropriate. And I happen to know just the guy:

My first contact with Chris was in 2016 when he was working with GiveWell, a super-efficient charitable organization that often tops the list for people looking to maximize the impact of their giving.

But much to my surprise, he showed up in my own HQ coworking space in 2018, and I noticed he was a bit of a mobile phone research addict. He had started an intriguing website called Coverage Critic, and started methodically reviewing every phone plan (and even many handsets) he could get his hands on, and I liked the thorough and open way in which he did it.

This was ideal for me, because frankly I don’t have time to keep pace with ongoing changes in the marketplace. I may be an expert on construction and energy consumption, but I defer to my friend Ben when I have questions about fixing cars, Brandon when I need advice on credit cards, HQ member Dr. D for insider perspectives on the life of a doctor and the medical industry, and now Chris can take on the mobile phone world.

So we decided to team up: Chris will maintain his own list of the best cheap mobile phone plans on a new Coverage Critic page here on MMM. He gets the benefit of more people enjoying his work, and I get the benefit of more useful information on my site. And if it goes well, it will generate savings for you and eventual referral income for us (more on that at the bottom of this article).

So to complete this introduction, I will hand the keyboard over to the man himself.

Meet The Coverage Critic

I started my professional life working on cost-effectiveness models for the charity evaluator GiveWell. (The organization is awesome; see MMM’s earlier post.) When I was ready for a career change, I figured I’d like to combine my analytical nature with my knack for cutting through bullshit. That quickly led me to the cell phone industry.

So about a year ago, I created a site called Coverage Critic in the hopes of meeting a need that was being overlooked: detailed mobile phone service reviews, without the common problem of bias due to undisclosed financial arrangements between the phone company and the reviewer.

What’s the Problem with the Cell Phone Industry?

Somehow, every mobile phone network in the U.S. claims to offer the best service. And each network can back up its claims by referencing third-party evaluations.

How is that possible? Bad financial incentives.

Each network wants to claim it is great. Network operators are willing to pay to license reviewers’ “awards”. Consequently, money-hungry reviewers give awards to undeserving, mediocre networks.

On top of this, many phone companies have whipped up combinations of confusing plans, convoluted prices, and misleading claims. Just a few examples:

- Coverage maps continue to be wildly inaccurate.

- Many carriers offer “unlimited” plans that have limits.

- All of the major U.S. network operators are overhyping next-generation, 5G technologies. AT&T has even started tricking its subscribers by renaming some of its 4G service “5GE.”

However, with enough research and shoveling, I believe it becomes clear which phone companies and plans offer the best bang for the buck. So going forward, MMM and I will be collaborating to share recommended phone plans right here on his website, and adding an automated plan finder tool soon afterwards. I think you’ll find that there are a lot of great, budget-friendly options on the market.

A Few Quick Examples:

Mint Mobile: unlimited minutes, unlimited texts, and 8GB of data for as low as $20 per month (runs over T-Mobile’s network).

T-Mobile Connect: unlimited minutes and texts with 2GB of data for $15 per month.

Xfinity Mobile: 5 lines with unlimited minutes, unlimited texts, and 10GB of shared data over Verizon’s network for about $12 per line each month (heads up: only Xfinity Internet customers are eligible, and the bring-your-own-device program is somewhat restrictive).

Cricket Wireless: 4 lines in a combined family plan with unlimited calling, unlimited texting, and unlimited data for as low as $100 per month (runs on AT&T’s network).

Ting: Limited use family plans for under $15 per line each month.

[MMM note - even as a frequent traveler, serious techie and a “professional blogger”, I rarely use more than 1GB each month on my own Google Fi plan ($20 base cost plus data, then $15 for each additional family member). So some of these are indeed generous plans]

Okay, What About Phones?

With the above carriers, you may be able to bring your existing phone. But if you need a new one, there are some damn good, low-cost options these days. The Moto G7 Play is only $130 and offers outstanding performance despite the low price point. I use it as my personal phone and love it.

If you really want something fancy, consider the Google Pixel 3a or the recently released, second-generation iPhone SE. Both of these are amazing phones and about half as expensive as an iPhone 11.

——————————————-

Mobile Phone Service 101

If you’re looking to save on cell phone service, it’s helpful to have a basic understanding of the industry. For the sake of brevity, I’m going to skip over a lot of nuances in the rest of this post. If you’re a nerd like me and want more technical details, check out my longer, drier article that goes into more depth.

The Wireless Market

There are only four nationwide networks in the U.S. (soon to be three thanks to a merger between T-Mobile and Sprint). They vary in the extent of their coverage:

- Verizon (most coverage)

- AT&T (2nd best coverage)

- T-Mobile (3rd best coverage)

- Sprint (worst coverage)

Not everyone needs the most coverage. All four nationwide networks typically offer solid coverage in densely populated areas. Coverage should be a bigger concern for people who regularly find themselves deep in the mountains or cornfields.

While there are only four nationwide networks, there are dozens of carriers offering cell phone service to consumers - offering vastly different pricing and customer service experiences.

Expensive services running over a given network will tend to offer better customer service, more roaming coverage, and better priority during periods of congestion than low-cost carriers using the same network. That said, many people won’t even notice a difference between low-cost and high-cost carriers using the same network.

For most people, the easiest way to figure out whether a low-cost carrier will provide a good experience is to just try one. You can typically sign up for these services without a long-term commitment. If you have a good initial experience with a budget-friendly carrier, you can stick with it and save substantially month after month.

With a good carrier, a budget-friendly phone, and a bit of effort to limit data use, most people can have a great cellular experience while saving a bunch of money.

MMM’s Conclusion

From now on, you can check in on the Coverage Critic’s recommendations at mrmoneymustache.com/coveragecritic, and he will also be issuing occasional clever or wry commentary on Twitter at @Coverage_Critic.

Thanks for joining the team, Chris!

*okay, special exception if you use it for work in video or photography. I paid $299 a year ago for my stupendously fancy Google Pixel 3a phone.. but only because I run this blog and the extra spending is justified by the better camera.

The Full Disclosure: whenever possible, we have signed this blog up for referral programs with any recommended companies that offer them, so we may receive a commission if you sign up for a plan using our research. We aim to avoid letting income (or lack thereof) affect our recommendations, but we still want to be upfront about everything so you can judge for yourself. Specific details about these referral programs is shared on the CC transparency page. MMM explains more about how he handles affiliate arrangements here.

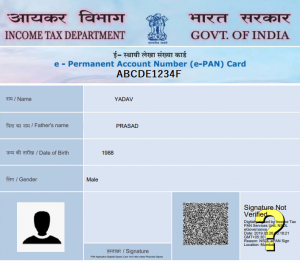

PAN or Permanent Account Number is a unique 10-digit alphanumeric code issued to each and every entity carrying out financial transactions in India. Be it an individual or an organisation, PAN is mandatory for all tax-paying entities. One can apply for a PAN through NSDL website or UTIITSL portal for PAN. PAN hardcopy is can be received on the address mentioned in the Form 49A within 45 days of application. One can, however, download the ePAN online and use it as a valid document everywhere.

Extra Saving on Online Shopping is Just One Click Away

Table of Content :

Get Your Free Credit Report with Monthly Updates

Check Now

What is ePAN?

ePAN is a virtual PAN card that contains the card holder’s PAN details. It can be downloaded either from the NSDL portal or the UTIITSL portal. It contains the card holder’s PAN and can be used for all e-verification that require PAN card to be furnished.

Following details are mentioned in an ePAN card:

- Permanent Account Number

- Name

- Father’s Name

- Date of Birth

- Gender

- Photograph

- Signature

- QR Code

It is worth mentioning that it is illegal to possess more than one PAN card. A person found in possession of more than one PAN card is liable to be imposed a fine of up to Rs. 10,000.

Steps to Download ePAN Online

ePAN can be downloaded online from NSDL and UTIITSL portal. Those applicants who had applied for PAN through the NSDL portal in the past can download ePAN from the same. If they want to download the ePAN from UTIITSL portal, they will have to apply for PAN card reprint through the UTIITSL portal first otherwise they will not be able to download the ePAN. The same goes with the applicants of UTIITSL portal.

ePAN can be downloaded free of cost by all new applicants or applicants who have applied for a modification in the PAN data within one month of the issuance of PAN. UTIITSL charges an additional fee of Rs. 8.26 (including taxes) for every download request. This payment can be done online and the applicant can download the ePAN whenever he needs it.

Get a Low Annual Fee Credit Card in Just 7 Days*

How to Download ePAN from NSDL Portal?

There are two options for downloading the ePAN through NSDL portal:

- Download ePAN using the Acknowledgement Number (https://www.onlineservices.nsdl.com/paam/MPanLogin.html)

- Download ePAN using PAN (https://www.myutiitsl.com/PAN_ONLINE/ePANCard)

NSDL does not allow users to download ePAN after one month of application, be it for a new PAN card or corrections/modifications in PAN card.

Applicants can opt out from the delivery of the PAN card hardcopy and apply only for ePAN at the time of filling the form, both new and correction. In such cases, it is mandatory to quote the email address where the ePAN will be delivered.

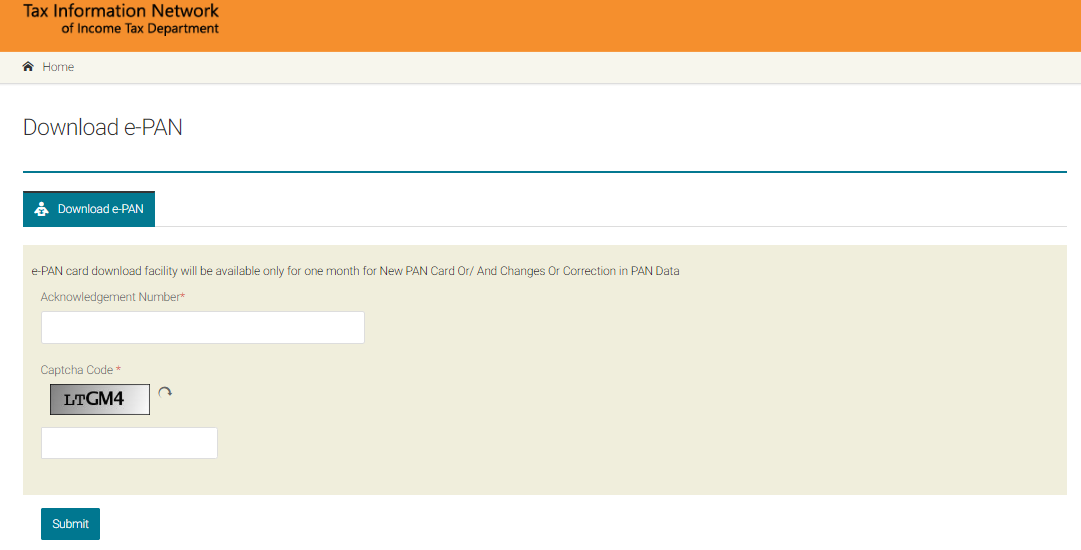

How to Download ePAN by Acknowledgement Number?

One can download ePAN from the NSDL portal by following the steps mentioned below:

- Visit NSDL PAN portal to download PAN card by Acknowledgement number

- Enter the Acknowledgement number issued after submitting the PAN card application and click on “Generate OTP”

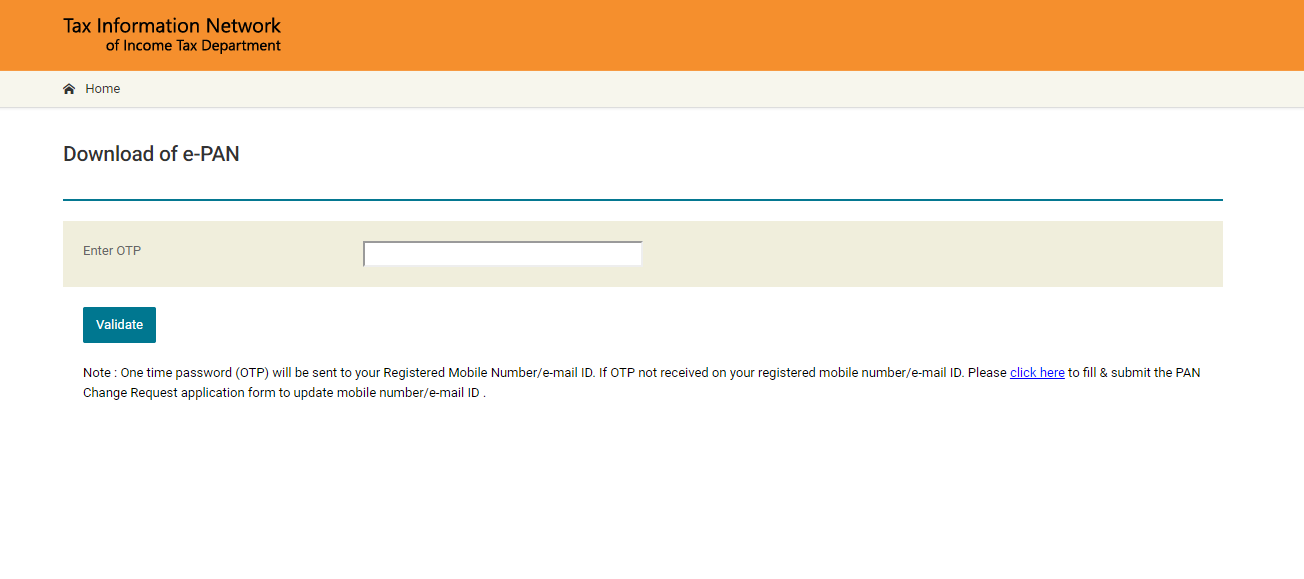

- Enter the OTP and click on the “Validate” button to download your ePAN

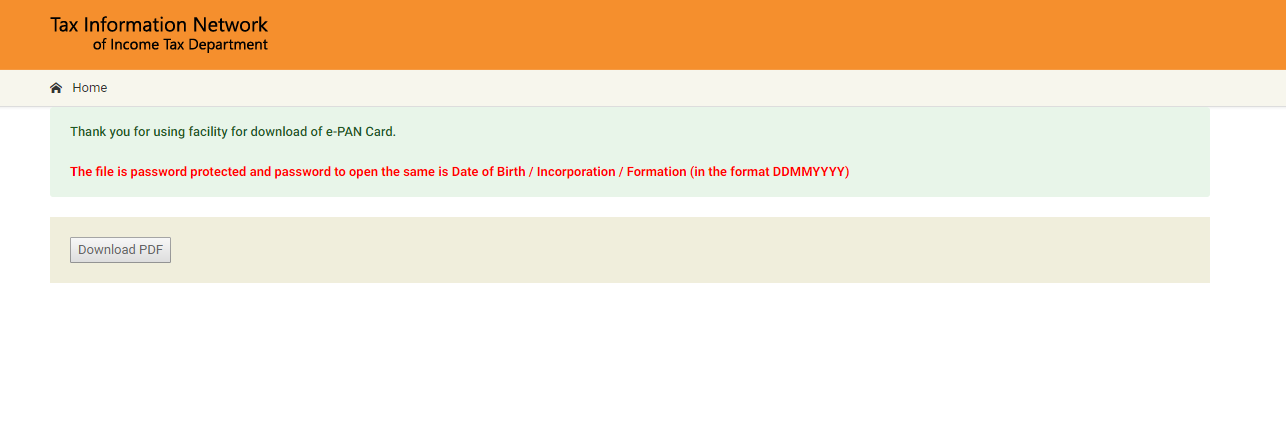

- Click on “Download PDF” to download the ePAN instantly

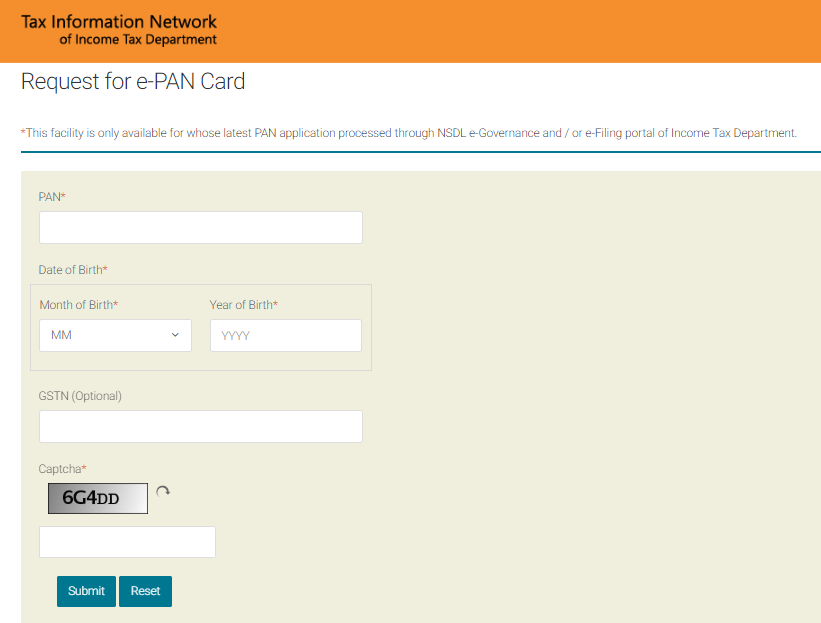

How to Download ePAN by PAN and Date of Birth?

One can download the ePAN card by mentioning the PAN and date of birth as well. Following steps should be followed for the same:

- Visit the ePAN downloading portal

- Enter details required in the form such as PAN, Date of Birth, GSTN (optional)

- Now mention the security code and click on “Submit” to download the ePAN card for free

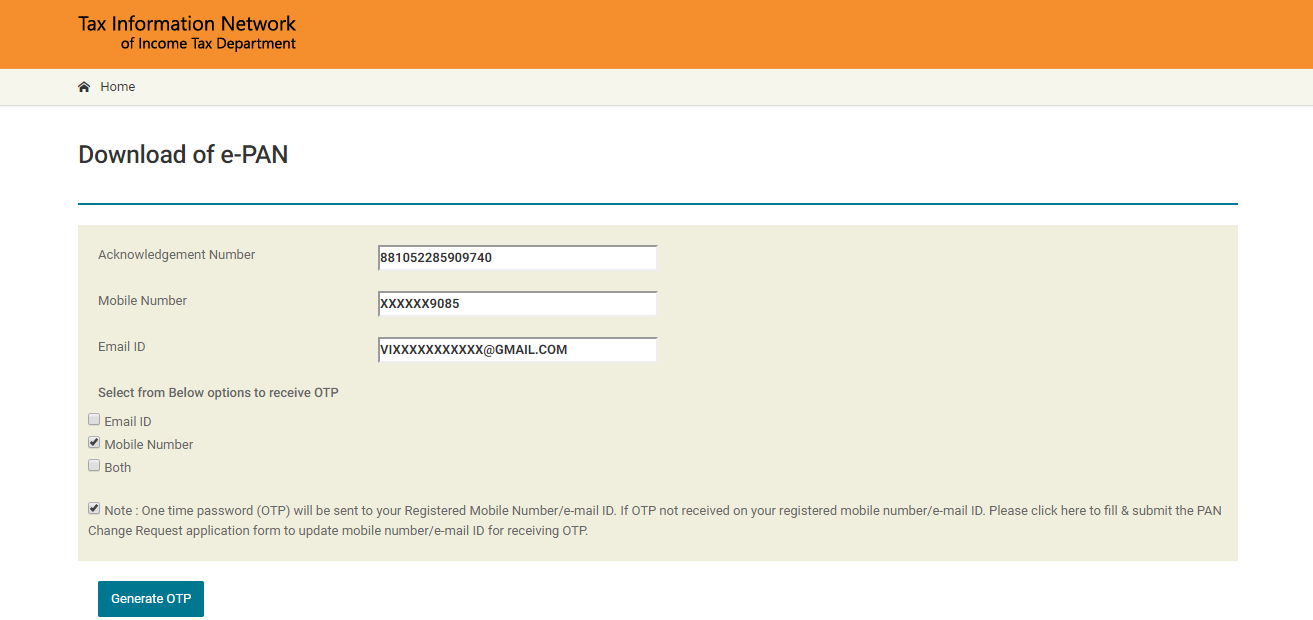

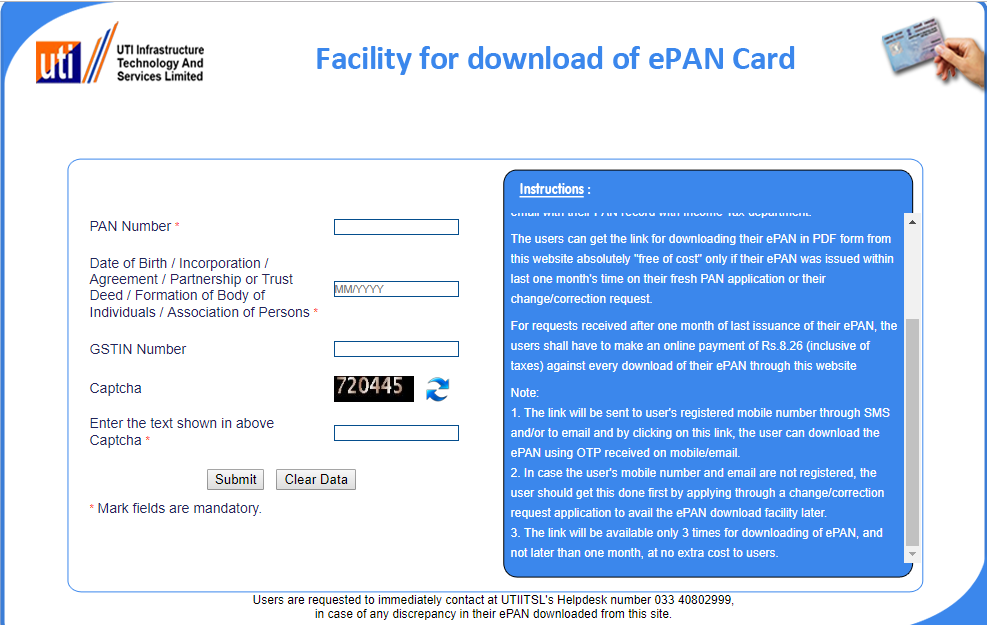

How to Download ePAN from UTIITSL Portal?

UTIITSL is an alternative portal from where applicants can apply for new PAN cards or making corrections in the existing PAN. Applicants who have applied through UTIITSL can download the ePAN online. If the ePAN is downloaded within 30 days of issuance of the PAN card, no additional fee is charged.

One can download the ePAN from the UTIITSL portal by following the steps mentioned below:

- Visit the ePAN downloading portal of UTIITSL

- Enter the required details such as PAN, date of birth/incorporation, GSTIN (optional) and security code and submit the application

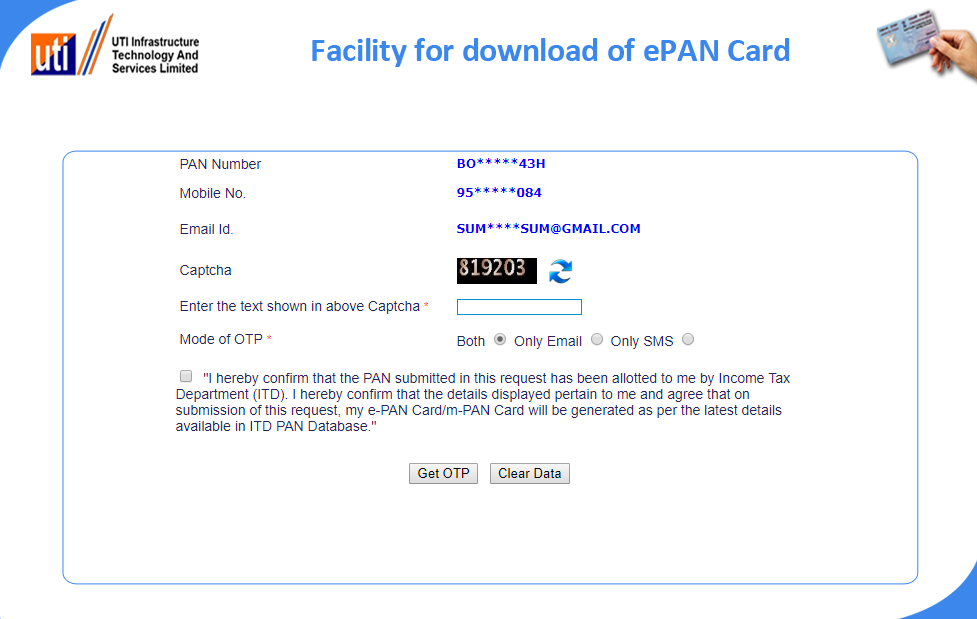

- Check whether the mobile number and e-mail ID mentioned against the PAN is correct and enter the security code and tick the declaration

- The user gets the option to send the OTP to either mobile number, email ID or both

- An OTP is sent to the selected source

- Enter the OTP and click on submit

- In case the PAN issuance period is more than one month, the user will be directed to make an online payment of Rs. 8.26

- On successful processing, the user will be able to download the ePAN online.

Get Your Free Credit Report with Monthly Updates

Check Now

FAQs on Downloading ePAN Card

Q. How to download my old PAN card by the PAN Number?

Ans. You can download your old PAN Card by availing the facility of duplicate PAN Card download through ‘Reprint PAN Card’ option provided by the Income Tax Department of India from either NSDL or UTITTSL Portal.

Q. I lost my PAN Card, but I remember my PAN Card Number. Can I download a copy from the Internet and from which website?

Ans. Yes, in case you have lost your PAN Card and you remember your PAN Card Number, you can download PAN Card soft copy from the official website of either NSDL or UTIITSL. However, e-PAN Card download by coupon number can be done via UTIITSL Portal and duplicate PAN Card download by acknowledgement number can be done through NSDL Portal.

Q. How can I reprint my PAN Card?

Ans. To reprint your PAN Card, you need to visit the official website of TIN-NSDL for old PAN Card download by applying for duplicate PAN Card download. To know the process in detail, click here.

Q. How to download an e-PAN Card without a PAN Number?

Ans. To download an e-PAN without a PAN Number, a duplicate PAN Card download can be done through the ‘Know your PAN’ facility from the official website of Income Tax Department i.e. www.incometaxindia.gov.in

Q. Is there any facility to download e-PAN Card without Acknowledgement Number?

Ans. Yes, you can download e-PAN Card without Acknowledgement Number by entering your PAN Number, Aadhaar Number (only for Individuals) and other details like Date of Birth, GSTIN (optional) and you have applied for e-PAN for more than 30 days through NSDL e-Governance and / or e-filing portal of Income Tax Department.

Q. Is there any PAN card download app?

A. No, there is no PAN card download app. One has to either visit NSDL website or UTI Infrastructure Technology And Services Limited website to download ePAN.

Q. What is the fee charged for downloading ePAN card?

A. An applicant can download the ePAN card for free for the first month of issuance of the new/modified PAN card. After that, UTIITSL applicants will have to pay a fee of Rs. 8.26 for each ePAN card download.

Q. Is ePAN a valid document?

A. ePAN is equally valid as a regular PAN card. Both are the same documents and are just issued through different media.

The post How to Download and Print ePAN Card Online appeared first on Compare & Apply Loans & Credit Cards in India- Paisabazaar.com.

(The following is a transcription from a video Linda and I recorded. Please excuse any typos or errors.)

All right. Today, we’re talking about 10 incredibly useful hacks to stick with your budgets. And, I’m really excited to share them with you.

We have really honed in on what it takes to have a budget that you can enjoy, that makes you feel good about life.

We’ve done it wrong so much that we’ve just learned how to do it right, and how to have fun in the process.

If you haven’t gotten Our Free Budgeting Worksheet, I’ve spent a lot of time making this thing and I think it’s awesome.

It’s a good first step to see how your income and expenses stack up. It’s just a good way to get started with your budget.

You can just pick that up by clicking here, and you’ll be on your way to starting your budget!

Now let’s get to these 10 amazing hacks to help you stick with your budget…

10. Make Savings Automatic

Bob: One of the biggest mistakes that most people make is they spend their money and then they try to save or give afterwards. You have to do it the opposite way, the things that are most important to you: giving money, savings, whatever those are, that needs to come first. If you don’t do it that way, if you don’t have some automatic thing in place, the reality is, we all know this.

Linda: It’s not going to happen.

Bob: We all know this, it’s probably not going to happen. You’re going to get to the end of the month, there’s not anything there. And so, that’s why making it automatic is incredibly important.

9. Reward Yourself

Bob: Or if you’re a Parks and Recreation fan, we could call it, treat yo self.

Linda: Treat yo self. This comes across though, as like, “I’m just going to treat myself all the time,” which is something I would do, but we’re not talking about that. Right?

Bob: Yeah. But the key in terms of sticking to your budget, you need rewards. You need incentives to stay the course. And so, yeah, when we were paying off our debt, this was a big part of that. Our budget was a big piece of us being able to pay off our debt. But in order to reach that goal, we had to have milestones. It was too big of a thing, it was too much, it was too long of a road for us to walk without some rewards. And so, we made sure to keep them in there and because we did, we were able to stick with it. Right?

Linda: Yeah. And I think this was especially key for me because he was watching the numbers of our debt go down, down, down. And he was really, really involved. But for me, I was more on the sidelines. And if I wouldn’t have had this incentive, it would have been really difficult for me to keep going. I think I would have just gotten discouraged and given up. So, I think this was extremely key for me since I was not as involved.

Bob: Yeah. Definitely.

8. Budget With Accountability

Bob: I’ve had the unique advantage of being able to try out and test out a whole bunch of different budgeting methods, budgeting softwares and tools and spreadsheets, and all this stuff over the years. I’ve been a financial blogger for almost 13 years, and I have reviewed almost everything out there, and I’ve tried out so much of the stuff. Because we’ve actually tried it ourselves.

The thing that I’ve come to realize is that most budgeting methods don’t actually hold you accountable. There’s this false sense of accountability. And so, the only tool that I’m aware of that ever actually hold you accountable are cash envelopes, if you do that and put cash in envelopes and do that type of budgeting.

Linda: Yeah. And that wasn’t going to work for us because we use plastic sometimes because we online shop or whatever.

Bob: Yeah. Then the other option is The Real Money Method. And this is kind of our hack to do that, to have a budgeting method that actually holds you accountable. So, we have an entire course teaching this method in which you’re welcome to check out if you’re interested. But the bottom line is that for most of us to stick with a budget, we need accountability. We need a budget that’ll hold us accountable. And so, if you’ve ever failed with budgeting, this might be the reason why. So, just find something that will hold you accountable.

7. Don’t Save Your Credit Card Info On Any Site Where You Shop

Bob: This is a good hack. This, yeah, because adding that friction, I think that would definitely, yeah. It just doesn’t seem like much, but having to spend the extra minute or two to go through with the purchase to type all that in, it just slows you down.

Linda: All right. So, I think you’ve told me about this before, where there’s something almost physical that happens in your body when you pay for something and you have to hand over cash.

Bob: Because it’s just real money and you get to feel it.

Linda: Yeah. And you’re like, “There’s my money and it’s leaving.”

Bob: It’s disappearing, yeah.

Linda: But when you write a check, you told me it’s less, but it’s still more of a process that you still feel like…

Bob: A little bit less real, yeah.

Linda: And then, less when you are swiping your credit card.

Bob: Yeah.

Linda: I think you told me this years ago, really before online shopping was as big as it is now. And I can only imagine how little you feel that when it’s like click, click, and it’s, “I bought it.”

Bob: Yeah.

Linda: It’s done.

Bob: I mean, that’s what Amazon has done. It’s like literally-

Linda: Oh, my gosh.

Bob: Add To Cart, boom. Done.

Linda: Well, and you can even hit Buy It Now. And it’s like click, you’re done.

Bob: Yeah. You’re right. It’s one click. So, it’s brilliant on their part. But the point is, is that adding that friction will overall reduce the spending that we make. So yeah, it’s an important move to make.

6. Only Use Gift Cards To Shop On Amazon

Linda: Number six ties right into what we were just talking about. Only use gift cards to shop on Amazon.

Bob: This is an interesting idea that the author had to basically go to the grocery store, buy an Amazon gift card for $100 or whatever, and then load that on your account and then make purchases with that. And so, this kind of takes that friction to a whole new level in that you need to go to the store and buy an Amazon gift card. But at the same time, it kind of undoes the previous thing we were just talking about because the gift card is loaded in there and it’s still pretty easy to buy. So, it’s kind of like, yeah, I don’t know. It might work for some people, but something to consider.

5. Never Buy Anything That You Put In An Online Shopping Cart Until The Next Day

Linda: Number five, never buy anything that you put in an online shopping cart until the next day.

Bob: This is a good idea. I can’t tell you how many times I’m struggling with some annoying problem around the house and I need to go buy this. I’m like, “I need to go buy this thing to fix it,” whatever it is. And I’ll put the thing in a cart and just because I forget to go buy it and I’ll come back a couple of days later, I’m like, I actually solved that problem already. Or it’s not even that big of a problem. It seemed like a big problem in the moment, but it really isn’t that big of a problem. And it is amazing. We’ve all heard this, just sit on a purchase for a little bit and then, half the time, you don’t want to make it later on. But I like this idea of throwing it in the cart. That way, you won’t forget about it. And you can check in a couple of days.

Linda: Yeah.

Bob: And see.

Linda: Well, and I think this is really key for stuff that you just want.

Bob: Yeah, especially.

Linda: Because I mean, so many times, you’re just trying to numb yourself. You’re like, “I’ve had a bad day, so I’m going to go online shop.” And I know that’s what I do. So, just sitting on that, having it in your cart kind of gives you a little bit of satisfaction, and then being able to sit on it for a little bit, I think really helps. And then you can make a decision when you’re a little bit more clearheaded.

Bob: Yeah.

4. Read The One-Star Reviews For The Products Before You Buy Them

Linda: Okay, I really like this one. Read the one-star reviews for the products before you buy them.

Bob: This is a great idea. Because it definitely gives you a whole different perspective on the product.

Linda: Yeah.

Bob: And yeah, and you just might not be as interested when you see all the negative things about it.

Linda: Right.

Bob: Now, I do this for really, most products I buy, because I want to see what people are saying the bad is.

Linda: Yeah. You don’t want to buy a product that’s going to be terrible and it’s not what you want.

Bob: Well, yeah, if you have 20 people in a row saying that whatever, “it stopped working after three months,” it’s like, all right, there might be a trend here. So, just from a smart shopping perspective, I think this is good, but it also will help you. Yeah, I think it will deter you from buying more things if you’re looking at the bad.

3. Don’t Go To The Grocery Store Hungry

Linda: All right. Number three, this one is classic.

Bob: But it works. It works.

Linda: Don’t go to the grocery store hungry.

Bob: Yeah. It just really, really works. It’s such a big difference when you, yeah, when you’re…

Linda: When you’re full and you’re not hungry.

Bob: Yeah.

Linda: You should go to the grocery store only full. It’s where you’re just like, “None of this sounds good.”

Bob: No, this is what you should do. You should go to the grocery store after a Thanksgiving meal, when you’re so bloated and just be like, “I don’t want any food.” You’re tired. That’s when you go to the grocery store.

Linda: You won’t be buying much. But then, you’ll regret it later because you’ll be like, “Why is there no food in the house?”

2. Only Make Major Purchases In The Morning

Linda: Number two, only make major purchases in the morning.

Bob: Yeah. I think this is really interesting. I remember, I think Tim Ferriss was talking about decision fatigue, and this idea that we only have a limited number of decisions that we can make any given day. And after that point, we’re just tapped out and we can’t actually make any more decisions.

Linda: Yeah.

Bob: And so, what happens is, so many of us in busy lives, we get to the end of the day and we’re just worn down and we don’t have good decision-making abilities. Whereas at the beginning of the day, we’re fresher. And we have, if you think of it in terms of a bank account, we have a lot more decisions sitting there that we can tap into. So, making these purchases, especially big purchases in the morning when we’re stronger, it’s just a better approach.

1. Choose A Major Category Each Month To Attack

Linda: Okay. Number one, choose a major category each month to attack.

Bob: I think this is a good idea. I think too many people try to solve 10 problems at once. And I think focusing your energy on just one, find one category in your budget that you’re struggling with, even though you might be struggling with four or five of them, find one, focus your energy on solving that particular one, whatever that is. If it’s groceries, if it’s household goods, whatever that category is, try to solve that one.

Linda: Yeah. And we’ve talked about this before, where you should not base your budget around what your personal goals are. You need to base it around where you actually are in your life. So, if you were going to Starbucks every day and you want to change that, do that one month. And then, once you’ve got that down, work on the next habit. Don’t try and do it all at once, because you’re going to blow your budget. It’s not going to work. And you’re just going to be mad.

What Budgeting Tip Would You Add To This List?

Yeah. So, those are our top 10. I’d love to hear yours in the comments.

Don’t Forget The Free Budgeting Worksheet!

Like I mentioned at the beginning, if you are new to budgeting, or if you just need a little help, be sure to get our free budgeting worksheet.

Source article that inspired this video/article: 13 incredibly useful budgeting hacks to help you stick to your budget.

Finding the best interest rates is a lot easier today than it was even a few years ago. Here at Dough Roller, we track rates on everything from checking and savings accounts to mortgages to CDs. It occurred to me, however, that there was no one single page on the site where you could find the top rate for each type of account. So we created this page, updated monthly, to track the highest (or lowest) rates available.

Deal of the Day: Chase is now offering a $200 cash bonus when opening a Total Checking Account. No minimum deposit and all deposits are FDIC insured up to the $250,000 per depositor maximum.

We focus on those financial institutions that have low fees, great rates, and are typically available anywhere in the U.S. You can find local banks and credit unions that offer comparable rates, but their availability is limited geographically.

Best Interest Rates for November 2019

November 2019 Interest Rates Update: There were a few rate changes over the past month:

- Betterment Everyday

Cash Reserve account is at 2.04% APY.

Cash Reserve account is at 2.04% APY. - Wealthfront Brokerage Cash Account Rate is at 2.07% APY.

- First Security Bank’s Kasasa Cash account is at 2.51% APY on balances up to $50k; their Kasasa Saver account is at 1.31% APY on balances up to $50k.

- First Foundation Bank’s Online Savings Account offers 2.40% APY with $1k minimum deposit of new money.

- BrioDirect is offering a High-Yield Savings account at 2.30% APY with $25 minimum deposit.

- Vio Bank’s High Yield Online Savings account is at 2.27% APY with $100 minimum opening deposit.

- Fitness Bank is offering a 2.75% APY savings account rate for balances over $100 when step requirements are met.

- Prime Alliance Bank is offering a 60-month CD at 2.48% APY and a 48-month CD at 2.38% APY, both with $500 minimum deposit.

- First National Bank of America is offering a 12-month CD at 2.35% APY and a 60-month CD at 2.55% APY, both with $1k minimum deposit.

The average 30-year fixed mortgage rate comes in at 3.78%.

With that said, here are some of the best interest rates we’ve found for November 2019:

Best Bank Account Rates

![]() Savings Accounts: The top savings account rate goes to Vio Bank at 2.27% APY ($100 minimum deposit) (see table below). Several banks come in a close second, including UFB Direct at 2.15% APY , Popular Direct at 2.15% APY ($5k minimum), CIT Savings Account at 2.10% APY ($100 monthly deposit or $25k minimum balance) and BMO Harris Bank Money Market Account at 2.05% APY ($5k minimum). These represent some of the highest rates on a nationally available savings account.

Savings Accounts: The top savings account rate goes to Vio Bank at 2.27% APY ($100 minimum deposit) (see table below). Several banks come in a close second, including UFB Direct at 2.15% APY , Popular Direct at 2.15% APY ($5k minimum), CIT Savings Account at 2.10% APY ($100 monthly deposit or $25k minimum balance) and BMO Harris Bank Money Market Account at 2.05% APY ($5k minimum). These represent some of the highest rates on a nationally available savings account.

Here’s a comparison table we update daily with current competitive rates:

Best CD Rates: The rates on certificates of deposit vary based on the term. The longer the term, the higher the rate. Keep in mind that penalties may apply if you close the CD before the end of the term. For a 1-year CD, the best rate we could find is from First National Bank of America at 2.35% APY ($1k minimum).

Checking Accounts: Most checking accounts do not pay interest. For online banks, however, you’ll find plenty of options where you can earn some interest on your funds. There are two things to keep in mind. First, many banks offer higher interest rates only if you keep a lot of money in your checking account. Second, the rates are lower than a savings account or CD.

Some top paying checking accounts that we like include FNBO Direct, which currently pays 0.65% APY. For those with at least $15,000 in checking, you can earn 0.60% APY from Ally Bank. I list Ally second because most people don’t keep that much cash in checking, but it’s an option for those who do. These rates are unchanged from previous months.

Bonus: I also keep a running list of popular checking account promotions you can check out.

Mortgage Rates

Mortgages: Listing the “best” mortgage rate is really impossible. Rates change throughout the day, vary by state, and are highly dependent on a number of factors including your credit score, debt-to-income ratio, and down payment. That being said, the average rate for a 30-year fixed rate mortgage is up this month to 3.78% according to Freddie Mac (from 3.64% last month). The average rate on a 15-year fixed mortgage is up to 3.19% (from 3.16% a month ago).

You can find competitive mortgage and refinance rates at LendingTree or on the table below:

Related: Compare mortgage rates online

Best Credit Card Interest Rates

Credit Cards: The longest 0% introductory period stands at 15 months on both purchases and balance transfers. You can find a current list of the best 0% credit card offers here.

If you find better rates on any of the above financial products, please let us know in the comments below.

Note that the above rates were as of October 31, 2020. Rates are subject to change, so please confirm the rates directly with the financial institution.Find the best interest rates on bank accounts, mortgages, and credit cards as of %%currentdate%%. Includes rates on savings and checking accounts, and CDs.

The post The Best Interest Rates for August 2020 appeared first on The Dough Roller.

-

Business3 weeks ago

Business3 weeks agoBernice King, Ava DuVernay reflect on the legacy of John Lewis

-

World News3 weeks ago

Heavy rain threatens flood-weary Japan, Korean Peninsula

-

Technology2 weeks ago

Technology2 weeks agoEverything New On Netflix This Weekend: July 25, 2020

-

Finance3 months ago

Will Equal Weighted Index Funds Outperform Their Benchmark Indexes?

-

Marketing Strategies7 months ago

Top 20 Workers’ Compensation Law Blogs & Websites To Follow in 2020

-

World News7 months ago

World News7 months agoThe West Blames the Wuhan Coronavirus on China’s Love of Eating Wild Animals. The Truth Is More Complex

-

Economy9 months ago

Newsletter: Jobs, Consumers and Wages

-

Finance8 months ago

Finance8 months ago$95 Grocery Budget + Weekly Menu Plan for 8