Finance

Top 13 Best Pokémon ROM Hacks

Pokémon games stand out as being one of the largest and most well-known fandom franchises.

It provides endless characters, possibilities, storylines, and games!

So, what is a Pokémon ROM Hack?

ROM hacks are video games that have been modified by fans to create an entirely new looking and improved version of a game. No need to confuse yourself between Pokémon ROM hacks and Pokémon GBA ROM hacks, they are all the same.

Grab your Pokeballs and your trainer hat! We have compiled a list for you of the best Pokémon ROM Hacks of all time!

The 13 Best Pokémon ROM Hacks of all time

1. Pokémon Mega Power

The game is a ROM hack of Emerald but features many distinct sprites and a brand-new story. In Mega Power, the character is on a quest to make the strongest Pokémon. To achieve this, your character has performed a lot of experiments.

Unfortunately, you are running out of funds. Not to worry! A mysterious financier comes to your rescue.

You go on an adventure, but suddenly you get an epiphany. Is your financier out for your quest for knowledge? Perhaps his money will be used to manipulate your strongest Pokémon creation?

The gameplay in Mega Power is remarkably like the original. Pokémon Mega Power does contain three new areas or Regions such as Ivara, Lander, and the Sevii Islands.

There are several Generation IV, V, VI, and VII Pokémon included in the game. It also boasts of having all the Mega Evolutions available in the game.

2. Pokémon Light Platinum

This one is a hack of Pokémon Ruby with edited graphics. In Light Platinum, you get to explore the Zhery Region while meeting and battling new rivals. Players can pit their skills against the region’s awesome Gym Leaders, Elite Four, and the Champion. You can capture and train Pokémon from the Kanto, Johto, Hoenn, and Sinnoh Regions.

Be sure not to forget about the moves and items you can collect when you play this game. There are some special events that you can participate in the game as well as the Pokémon World Championship. Think of the Pokémon World Championship as the endgame content after you have dominated the Elite Four.

You can get an excellent twenty-plus hour playing Pokémon Light Platinum. That is some decent gameplay!

3. Pokémon Flora Sky

Pokémon Flora Sky is Pokémon Emerald, but with everything that you wish the original had!

There are more mountains, forests, caves, and a bunch more Pokémon in the game. There are 368 Pokémon to catch, each with animated sprites, new moves, new items, and a brand-new story.

This game is may is not perfect, but it grabbed some big-name attention. There are several things Game Freak and Nintendo have taken from this ROM hack for their next games in the series. This includes a progression system that does not require grinding.

To complete the story and progress through the areas appropriately, this hack makes you go on the form of a treasure hunt. It makes you see every nook and cranny of their upgraded Hoenn.

Every Pokémon is catchable, and some of the games’ original encounter rates are reversed: It is easier to catch a Rotom in this game, but a fair bit harder to catch a Ralts.

A brighter color pallet and an easier story to follow as you play your ROM hacks place Pokémon Flora Sky on our list.

4. Pokémon Blazed Glazed

Pokémon Blazed Glazed is another hack of Emerald. This ROM hack is an improvement over the older version, which was Pokémon Glazed. The story is the same where your character has reached the age of maturity. You are given a Pokémon of your choice, and you start on your quest.

Unfortunately, the world is in chaos at that point, and you end up behaving to be the savior of both the real and Pokémon world.

There is also a Pikachu that is stalking you for revenge, but you can deal with that in the game. Considering that Blazed Glazed is an improvement or an update, the main features of Glazed is are there. These include choosing 5 Starters, different Regions to explore, as well as Dream World Pokémon.

There are quite a few new additions as well! There are added Pokémon from Generation IV to VI, new moves added from the different games, and different Pokémon added in different locations in the game. Some may spawn in the same location, and some added to the space.

There have also been some Pokémon moves that have been updated. This means that they do not learn their default moves in this hack. Quite a few worthwhile additions!

5. Pokémon Glazed

So, you may have noticed we already listed the game Pokémon Blazed Glazed. This next one, Pokémon Glazed, is the base of that game. While Blazed Glazed is somewhat of an improvement of this one, it is undeniable that Pokémon Glazed is still a fantastic ROM game.

You get the typical story of a boy coming into age and becoming a full-fledged Pokémon trainer. Unfortunately, the world seems to be ending, so you get to take part in saving it.

When it comes to the gameplay, you get to choose from five different starters. You can explore three Regions, such as Tunod, Johto, and Rankor. You also get to have Dream World Pokémon and a plethora of Legendaries to catch in the game.

Having the chance to battle trainers and Gym Leaders again is also a welcome feature so that you get more experience and money in the long run. Definitely a ROM game worth checking out.

6. Pokémon Theta Emerald EX

By now, we are coming to realize that Emerald is a popular game of choice for hacks!

Pokémon Theta Emerald EX is an updated version of Pokémon Theta Emerald. The story is somewhat the same, which is good, basic, and standard for any ROM hack available out there. This ROM hack does improve a lot of the aspects from the earlier versions.

There are over 700 Pokémon in this game compared to the 600 plus Pokémon in the past version. This also includes more abilities, TMs, HMs, and Mega Evolutions as well as Primal Revision. They also added the Fairy-type in the game and a new Repel mechanic.

There is also an added feature that is quite cool. You can run inside the buildings! This is a remarkably simple yet super useful feature.

7. Pokémon Mega Emerald X and Y Edition

This version of the game is finally complete. Pokémon Mega Emerald X and Y Edition is a hack of Pokémon Emerald but with fundamental elements from Pokémon X and Y. The story itself is a bit mundane, but it is the typical Pokémon adventure game that has its twists and turns. Most of the games and graphics are relatively the same.

The game still appears the same as Emerald, but the new Pokémon have their sprites edited for the game!

The game prides itself on having Pokémon from Generation I to VI, but not all of them. However, all the Legendary Pokémon from all those Generations are available in the game. You just need to trek through the different regions and areas to find and catch them.

Don’t forget about the Mega Evolutions and Primal Pokémon available in the game. If you are looking to spend a bunch of hours into a variation of Emerald, then this is the one to go for!

8. Pokémon Liquid Crystal

If you felt a bit traumatized from Pokémon Dark Rising, then Pokémon Liquid Crystal will help to soothe your wounds.

It is bright, colorful, and you can play through this game at a very leisurely pace while progressing. To do so, however, would be to miss the point of this game completely.

This game allows you to revisit the Kanto and Johto regions as well as the orange islands. The game truly has an adventurer feel to it.

It will appear to be a duplicate of Gen 2 with Gen 3 graphics. However, this game serves as an apology to all the older fans, who could not keep their Pokémon as the games progressed from Gameboy Advance to Nintendo DS. That is a nice touch!

9. Pokémon Gaia

Pokémon Gaia is a ROM hack that used Fire Red as the base. The game contains somewhat of an intricate story. In the past, the old civilization worshiped gods, but earthquakes consumed the upper areas. Thousands of years later, you are now a rising Pokémon trainer being asked by Professor Redwood to help prevent another calamity of earthquakes, which will sink the Region of Orbetus.

The Pokémon come from the Regions of Kanto, Johto, Sinnoh, Unova, and Kalos. The moves and other aspects are inspired and utilized by Omega Ruby and Alpha Sapphire. Many different mechanics are used, such as the Mega Evolutions, Fairy-type, and underwater locations, to name a few.

You can also find several Hidden Grottoes and Secret Temples and use TMs repeatedly.

Gaia could pass off as a spin-off game if you truly put the work into it!

10. Pokémon Ultra Shiny Gold Sigma

Pokémon Ultra Shiny Gold Sigma is another ROM hack of Fire Red. Despite it being a hack of Fire Red, the elements and story are based on the classic Gold, Silver, and other aspects from Crystal. The story follows those games from Generation II, but there are some added plot points and other elements to the story.

You also have a Pokémon roster with over 800 of them from Generation I to VII!

The game has other features such as Mega Evolutions and the Miracle Exchange. A cool feature to mention is it removes the trading evolution. You can evolve a Pokémon normally without the act of trading them. EVs and IVs are also shown on the menu so that you can avoid complicated calculations.

Be sure to remember the day and night cycle, as well as having a dawn and afternoon time!

Are you looking to spend long hours catching a whole bunch of Pokémon? This is the game for you.

11. Pokémon Adventures Red Chapter

Red Chapter is part of the official Pokémon Adventure Collections. This ROM hack emerged third place three consecutive times in the Poke Community Hack of the Year contest from 2013 to 2015. It is also a hack of Pokémon Fire Red.

This follows the story of the Pokémon Adventure Manga. The game follows the Manga closely, containing most of the events. However, some events were changed to make them longer.

Since the game follows the manga closely, you do not get to choose your own starter Pokémon.

Good news, though! You will be able to get that later in the game.

This ROM hack features some cool things, including all Pokémon, are catchable, root fossil replacing old amber in the pewter museum, and blue and green making more appearance in the game. Additionally, maps were changed to reflect on Manga’s appearance.

The graphics and display are updated compared to Fire Red, with customizable characters and levels up to 255.

The game also involves a day and night cycle, as other Pokémon games do. Try this game today when you are a big fan of the Pokémon Adventures manga.

12. Pokémon Dark Cry

Pokémon Dark Cry has a reasonably intricate story. You wake up and realize that you are lying in a cavern, and everything was highly contrasting. You see two individuals, remaining by a dim special raised area, discussing a “Shadow Plate.” You go after your Pokémon, yet they are not there. At that point, you see a man with “R” on his shirt. You attempt to stop him, yet he strolls directly past you.

This man plays out an unusual custom. Afterward, there is a gigantic quake, and a goliath shadow approaches you. You wake up and acknowledge that this was just a dream. You take a gander at the clock and acknowledge you are late for getting your Pokémon. Later you come to understand that your dream is becoming a reality. Creepy right?

The Pokémon Dark Cry features; new region, TrionPokePaper, daily news source, side quests, and mini-games automatic trainer, level cap increase, and many more.

This Gameboy advanced hack of the Pokémon Fire Red, according to users, is said to possess near-perfect gameplay. It also contains good mapping and amazing scripting.

13. Pokémon Ash Gray

This one is a hack of Fire Red, and the story follows the very first season of the Pokémon anime. You control Ash Ketchum, and if you are a big fan of the series, you will notice that the opening pretty much mirrors episode 1. Ash wakes up late and fails to get his Pokémon and ends up having Pikachu.

Embark on a quest to follow the story as it unfolds. As a bonus, they even added parts of some of the movies into the game.

You can get all the Pokémon that Ash got during his run in the series. However, you are not restricted in using those Pokémon. It is still a ROM hack, which means that you can get some Pokémon that you would want. You do get some Pokémon when the plot progresses, but you do not have to use them.

Considering this is based on the series, the Pokémon you can get is limited to the series. This means no features such as Mega Evolution and other Pokémon that have not appeared in the series.

This makes the gameplay more of a standard Pokémon game. They also removed the HM’s. That means you can use items to do HM moves.

If you are a big fan of the anime, then this hack is exactly right for you.

Wrapping Up the ROM’s

There are so many different Pokémon ROM games to choose from; it is impossible to pick only one. We hope that this list helped you narrow down the best ones to try!

This list has ROM hacks that have good stories, good gameplay, good Pokémon rosters, and more!

Which will you try first? The possibilities are endless, and as new ROM games will be created, there will be even more to check out!

After all, nothing is better than fans being so passionate about their games that they create versions of their own.

Where Can I Get these ROM Hack Games?

There are other locations to snag these from, but here are a few to check out!

The post Top 13 Best Pokémon ROM Hacks appeared first on Your Money Geek.

Right now, the market is at all time highs, and at some point in the future, it will inevitably pull back. While investing is long term, you might have short-er term goals that require short term investments.

If you’re a young investor and don’t want to see an immediate decline in your portfolio, now’s a good time to consider short term investment options. Short term investments typically don’t see the growth of longer term investments, but that’s because they are designed with safety and a short amount of time in mind.

However, millennials honestly haven’t experienced a prolonged bear or flat market. While the Great Recession was tough, millennials have seen their net worth’s grow. However, in periods of uncertainty, it can make sense to invest in short term investments.

Also, for millennials who may be looking at life events in the near future (such as buying a house or having a baby), having short term investments that are much less likely to lose value could make a lot of sense.

If you’re a young investor looking for a place to stash some cash for the short term, here are ten of the best ways to do it.

1. Online Checking and Savings Accounts

Online checking and savings accounts are one of the best short term investments for several reasons:

- They have higher interest rates than traditional accounts

- They are completely safe: your accounts are FDIC insured up to $250,000

- You can access your money any time and don’t have to worry about losing interest as a result

However, to get the very best rates from online checking and savings account, you typically have to do one of the following:

- Contribute a certain amount to the account (say $10,000 minimum)

- Sign up for direct deposit into the account

- Use your debit card for a certain number of transactions each month

If you’re going to be doing those types of transactions anyway, signing up for one of these accounts can make a lot of sense. And to make these accounts even more attractive, interest rates have been rising the last few months making yields go higher.

Our favorite online savings account right now is CIT Bank. They offer 0.60% APY online savings accounts with just a $100 minimum deposit! Check out CIT Bank here.

Check out the other best high yield savings accounts here.

2. Money Market Accounts

Money market accounts are very similar to online savings accounts, with one exception. Money market accounts typically aren’t FDIC insured. As a result, you actually can earn a little higher interest rate on the account versus a typical savings account.

Money market accounts typically have account minimums that you have to consider as well, especially if you want to earn the best rate.

Our favorite money market account right now is CIT Bank. They offer 0.60% APY money market accounts with just a $100 minimum deposit! Check out CIT Bank here.

Check out our list of the best online bank accounts for your money.

3. Certificates Of Deposit (CDs)

Certificate of deposits (CDs) are the next best place that you can stash money as a short term investment. CDs are bank products that require you to keep the money in the account for the term listed - anywhere from 90 days to 5 years. In exchange for locking your money up for that time, the bank will pay you a higher interest rate than you would normally receive in a savings account.

The great thing about CDs is that they are also FDIC insured to the current limit of $250,000. If you want to get fancy and you have more than $250,000, you can also sign up for CDARS, which allows you to save millions in CDs and have them insured.

Our favorite CD of the moment is the CIT Bank 11-Month Penalty Free CD! Yes, penalty free! Check it out.

We maintain a list of the best CD rates daily if you want to explore other options.

4. Short Term Bond Funds

Moving away from banking products and into investment products, another area that you may consider is investing in short term bonds. These are bonds that have maturities of less than one year, which makes them less susceptible to interest rate hikes and stock market events. It doesn’t mean they won’t lose value, but they typically move less in price than longer maturity bonds.

There are three key categories for bonds:

- U.S. Government Issued Bonds

- Corporate Bonds

- Municipal Bonds

With government bonds, your repayment is backed by the U.S. government, so your risk is minimal. However, with corporate bonds and municipal bonds, the bonds are backed by local cities and companies, which increased the risk significantly.

However, it’s important to note that investing in a bond fund is different than investing in a single bond, and if you invest in a bond fund, your principal can go up or down significantly. Here’s a detailed breakdown of why this happens: Buying a Bond Fund vs. Buying A Single Bond.

If you do want to invest in bonds, you have to do this through a brokerage. The best brokerage I’ve found for both buying individual bonds and bond funds is TD Ameritrade. TD Ameritrade has a bond screener built into it’s platform that makes it really easy to search for individual bonds to buy, and gives you a breakdown of all aspects of the bond.

Also, TD Ameritrade offers a $0 minimum IRA and hundreds of commission-free ETFs.

5. Treasury Inflation Protected Securities (TIPS)

Treasury Inflation Protected Securities (TIPS) are a type of government bond that merits their own section. These are specially designed bonds that adjust for inflation, which makes them suitable for short term investments as well as long term investments. TIPS automatically increase what they pay out in interest based on the current rate of inflation, so if it rises, so does the payout.

What this does for bondholders is protect the price of the bond. In a traditional bond, if interest rates rise, the price of the bond drops, because new investors can buy new bonds at a higher interest rate. But since TIPS adjust for inflation, the price of the bond will not drop as much - giving investors more safety in the short term.

You can invest in TIPS at a discount brokerage like TD Ameritrade. Some of the most common ETFs that invest in TIPs (and are commission-free at TD Ameritrade):

- STPZ - PIMCO 1-5 Year U.S. TIPS Index

- TIP - iShares TIPS Bond ETF

6. Floating Rate Funds

Floating rate funds are a very interesting investment that don’t get discussed very often - but they are a really good (albeit risky) short term investment. Floating rate funds are mutual funds and ETFs that invest in bonds and other debt that have variable interest rates. Most of these funds are invested in short term debt - usually 60 to 90 days - and most of the debt is issued by banks and corporations.

In times when interest rates are rising, floating rate funds are poised to take advantage of it since they are consistently rolling over bonds in their portfolio every 2-3 months. These funds also tend to pay out good dividends as a result of the underlying bonds in their portfolios.

However, these funds are risky, because many invest via leverage, which means they take on debt to invest in other debt. And most funds also invest in higher risk bonds, seeking higher returns.

If you want to invest in a floating rate fund, you have to do this at a brokerage as well. TD Ameritrade is a great choice for this as well. The most common floating rate funds are:

- FLOT - iShares Floating Rate Bond ETF

- FLRN - Barclay’s Capital Investment Grade Floating Rate ETF

- FLTR - VanEck Vectors Floating Rate ETF

- FLRT - Pacific Asset Enhanced Floating Rate ETF

7. Selling Covered Calls

The last “true” investment strategy that you can use in the short term is to sell covered calls on stocks that you already own. When you sell a call on a stock you own, another investor pays you a premium for the right to buy your stock at a given price. If the stock never reaches that price by expiration, you simply keep the premium and move on. However, if the stock does reach that price, you’re forced to sell your shares at that price.

In flat or declining markets, selling covered calls can make sense because you can potentially earn extra cash, while having little risk that you’ll have to sell your shares. Even if you do sell, you may be happy with the price received anyway.

To invest in options, you need a discount brokerage that supports this. TD Ameritrade has some of the best options trading tools available through their ThinkorSwim platform.

Related: Best Options Trading Platforms

8. Pay Off Student Loan Debt

Do you want a guaranteed return on your money over the short run? Well, the best guaranteed return you can get is paying off your student loan debt. Typical student loan debt interest rates vary from 4-8%, with many Federal loans at 6.8%. If you simply pay off your debt, you can see an instant return on your money of 6.8% or more, depending on your interest rate.

Maybe you can’t afford to pay it all off right now. Well, you could still look at refinancing your student loan debt to get a lower interest rate and save some money.

We recommend Credible to refinance your student loan debt. You can get up to a $750 bonus when you refinance by using our special link: Credible >>

9. Pay Off Credit Card Debt

Similar to getting out of student loan debt, if you pay off your credit card debt you can see an instant return on your money. This is a great way to use some cash to help yourself in the short term.

There are very few investments that can equal the return of paying off credit card debt. With the average interest rate on credit card debt over 12%, you’ll be lucky to match that in the stock market once in your life. So, if you have the cash to spare, pay down your credit card debt as quickly as possible.

If you’re struggling to figure out a way out of credit card debt, we recommend first deciding on an approach, and then using the right tool to get out of debt.

For the approach, you can choose between the debt snowball and debt avalanche. Once you have a method, you can look at tools.

First, you need to get financially organized. Use a free tool like Personal Capital to get started. You can link all your accounts and see where you stand financially.

Next, consider either:

- Balance Transfer: If you can qualify for a balance transfer credit card, you have the potential to save money. Many cards offer a promotional 0% balance transfer for a set period of time, so this can save you interest on your credit card debt while you work to pay it off.

- Personal Loan: This may sound counter-intuitive, but most personal loans are actually used to consolidate and manage credit card debt. By getting a new personal loan at a low rate, you can use that money to pay off all your other cards. Now you have just one payment to make. Compare personal loans at Credible here.

10. Peer To Peer Lending

Finally, you could invest in peer to peer loans through companies like LendingClub and Prosper. These aren’t completely short term investments - many loans are for 1-3 years, with some longer loans now available. However, that is shorter than what you’d traditionally want to invest for in the stock market.

With peer to peer lending, you get a higher return on your investment, but there is the risk that the borrower won’t pay back the loan, causing you to lose money. Many smart peer to peer lenders spread out their money across a large amount of loans. Instead of investing $1,000 in just one loan, they many invest $50 per loan across 20 different loans. That way, if one loan fails, they still have 19 other loans to make up the difference.

One of the great aspects of peer to peer lending is that you get paid monthly on these loans, and the payments are a combination of principal and interest. So, after several months, you’ll typically have enough to invest in more loans immediately, thereby increasing your potential return.

We are huge fans of LendingClub as a CD alternative, and you can sign up for LendingClub here.

Frequently Asked Questions

Here are some common questions about short term investments.

What makes a short term investment?

A short term investment is one that has a time frame of less than 5 years. Typically, short term investments are done to be more stable - but at the end of the day, it’s all about time frame.

Are short term investments risky?

They can be. The duration of the investment does not imply less risk. While some short term investments are risk-free (like savings accounts), others are extremely risky (like peer to peer lending).

Who should consider short term investments?

Anyone who is looking for an investment duration of less than 5 years. While it’s common to think people nearing retirement may need a short term investment, any age - including young adults - can benefit.

Is debt payoff an investment?

We think so! Paying off debt is a guaranteed return, especially in the short term.

{"@context":"https://schema.org","@type":"FAQPage","mainEntity":[{"@type":"Question","name":"What makes a short term investment?","acceptedAnswer":{"@type":"Answer","text":"A short term investment is one that has a time frame of less than 5 years. Typically, short term investments are done to be more stable - but at the end of the day, it's all about time frame."}},{"@type":"Question","name":"Are short term investments risky?","acceptedAnswer":{"@type":"Answer","text":"They can be. The duration of the investment does not imply less risk. While some short term investments are risk-free (like savings accounts), others are extremely risky (like peer to peer lending)."}},{"@type":"Question","name":"Who should consider short term investments?","acceptedAnswer":{"@type":"Answer","text":"Anyone who is looking for an investment duration of less than 5 years. While it's common to think people nearing retirement may need a short term investment, any age - including young adults - can benefit."}},{"@type":"Question","name":"Is debt payoff an investment?","acceptedAnswer":{"@type":"Answer","text":"We think so! Paying off debt is a guaranteed return, especially in the short term."}}]}Final Thoughts

Finding short term investments can be tough. It’s a bit counter intuitive to invest, but only for a short period of time. As a result, you’ll typically see investments with lower returns, but also have lower risk of loss.

What are your favorite short term investments?

The post The 10 Best Short Term Investments appeared first on The College Investor.

Since the Dawn of Mustachianism in 2011, the same question has come up over and over again:

I see your point that index fund investing is the best option. But when you buy the index, you’re getting oil companies, factory farm slaughterhouses and a million other dirty stories.

How can I get the benefits of investing for early retirement without contributing to the decline of humanity?”

And in these nine years since then, the movement towards socially responsible investing has only grown. Public pension funds have started to “divest” from oil company stocks, and various social issues like human rights, child labor, climate change or corporate corruption have bubbled to the surface at different times.

And all of this has led to the exploding new field of Socially Responsible Investing (SRI), and a growing array of new ways to do it.

So it seems that this is not just a passing trend - people just might be starting to care a bit more. And since capitalism is just an expression of human behavior, the nature of capitalism itself may be starting to change.

This leads us naturally to the question:

What can I do with my money to help fix the world? And even better, is there a way I can make money in the process of fixing it?

The answer is a good, solid “Probably.”

As long as you don’t get too hung up on getting every last detail perfect, because just like real life, investing is a haphazard and approximate and unpredictable thing. But by understanding the big picture, you can make slightly better decisions on average, which lead to slightly better results. And slightly better results, stacked up consistently over time, can lead to a much better life, or even a much better world.

This is true in all of the main areas we care about - personal wealth, fitness and health, even relationships and happiness. And while your money and investments are certainly not the most important thing in life, they are still worthy of a bit of easy and effective optimization.

So anyway, the first thing to understand with SRI is, “what problem am I trying to solve?”

The answer is, “You are trying to make your investing (especially index fund investing) have a better impact on the world.”

On its own, index fund investing is ridiculously simple. You just get an account at any brokerage like Vanguard, Etrade, Schwab or whatever, and dump all your money into one exchange-traded fund: VTI.

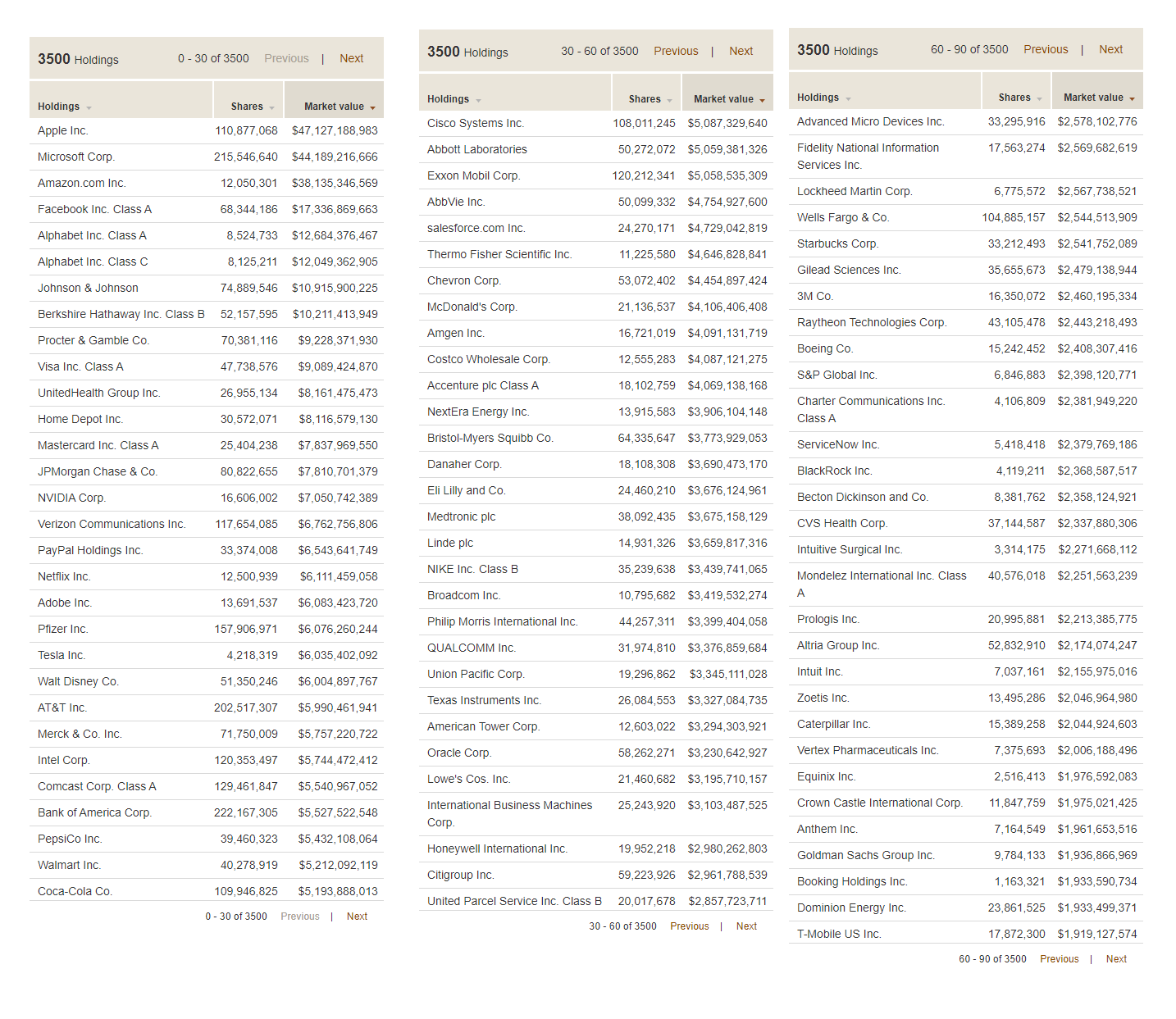

When you do this, you are buying a stake in 3500 companies at once(!), which is both impressive and overwhelming. How do you even know what you are holding?

Well, this is all public information, and easily available with a quick Google search. For example, here’s a list of the top 90 holdings in VTI (click for larger):

As you can see, the biggest chunk of money is allocated to today’s tech darlings, because this index fund is weighted according to market value, and these are the most valuable companies in the US today.

Through a convenient coincidence, the total value of the VTI fund happens to be just under $1 trillion dollars, which means you can just throw a decimal point after the ten billions digit of market value to get a percentage. In other words, about 4.7% of your money will go towards Apple stock, 4.4 towards Microsoft, and so on. Together, these top 90 companies are worth more than the remaining 3,410 companies combined, so these are what really drive your retirement account.

And within this list, you will see some of the usual suspects: Exxon and Chevron (oil), Philip Morris (tobacco), Raytheon and Lockheed (bombs), and so on.

But what about the less-usual suspects? For example, I happen to think that sugar, and especially sugar-packed beverages like Coke, is the biggest killer in the developed world - a major contributor to 2 million of the 2.8 million deaths each year in the US alone. Should I exclude that from my portfolio too?

And what about drug and insurance companies - aren’t they behind the political stalemate and high costs of the US healthcare system? Comcast funded some election disinformation campaigns here in my home town in the early 2010s, should I exclude them too? And if you’re part of a religion that is against charging interest on loans, or in favor of pasta and Pirate costumes, or against a spherical Earth, or any number of additional ornate rules, you may have still more preferences.

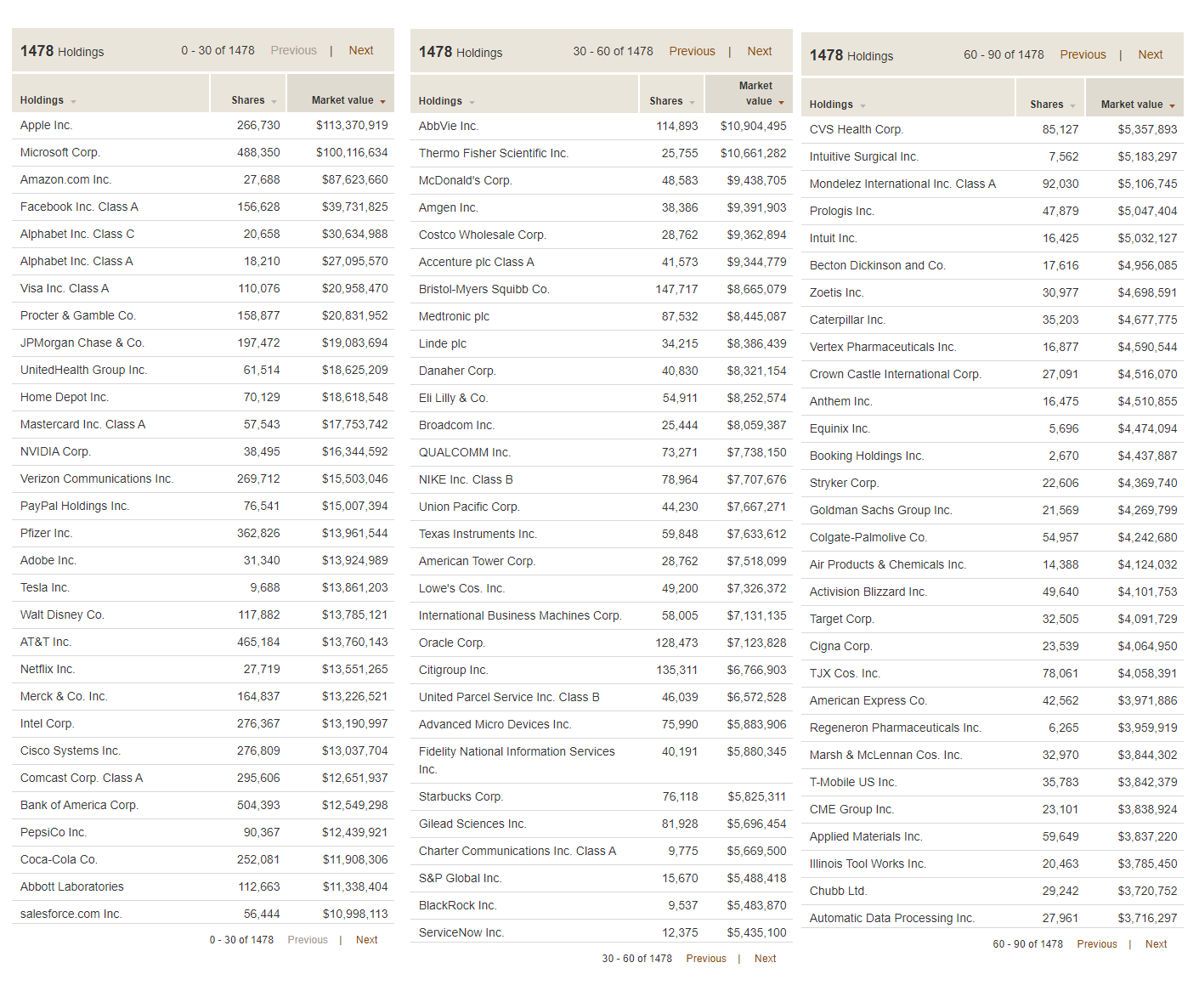

The higher your desire for perfection, the more difficult this exercise will become. However, if you are like me and you just want to get most of the desired result with minimal effort, you might simply have a look at the Vanguard fund called ESGV.

ESG stands for “Environmental, Social and Governance”, and in practice it just means “We have tried to avoid some of the shittier companies according to some fairly simple rules.”

And the result is this:

The first thing you’ll notice is that it’s almost the same. In fact, the top five holdings - Apple, Microsoft, Amazon, Facebook, Alphabet (Google) and Netflix not far behind, collectively referred to as the FAANG stocks - are completely unchanged - and this means that there will be plenty of correlation between these funds.

It’s also the reason that the stock market as a whole has recovered so quickly from this COVID-era recession: small businesses like restaurants and hair salons have been destroyed by the shutdowns, but big companies that benefit from people staying at home and using computers and phones are making more money than ever. The stock market isn’t the whole economy, it’s just the publicly traded companies, which are the big ones.

But let’s look at the biggest differences between the normal index fund versus the social version.

The following large companies listed on the left are missing in the ESGV fund, in order of size. And to make up the difference, the stake in the companies on the right have been boosted up to take their place in your portfolio.

The omission of Berkshire Hathaway was a bit of a shocker, as it is run with solid ethical principles by Warren Buffett, one of the worlds most generous philanthropists. And in fact the modern day nerd-saint Bill Gates is on the Berkshire board of directors, another person whose work I follow and respect greatly.

(side note: Apparently the company fails on the “independent governance” category. And Buffett disputes this category, but in his characteristic way has decided to say, “Fuck it, I’ma just keep doing my own thing with my half-trillion dollar empire over here and you can have fun with your little committee” - I’m paraphrasing a bit but he totally did say that.)

Furthermore, both funds hold the factory meat king Tyson foods, while neither holds Roundup-happy Monsanto, because it was bought by the German conglomerate Bayer AG a while back. Nextera is a giant electric utility in the Southeastern US that claims to be the world’s largest generator of renewable energy. Some do-gooders are against nuclear power, while others (including me) think it’s the Bee’s Knees and we should keep advancing it. And all this just goes to show how nobody will agree 100% on what makes a good socially responsible fund.

But What About The Performance?

In the past, some investors were nervous about giving up oil companies in their portfolio, because while it was a dirty substance, it was also what made the world go round - which meant it was a cash cow.

Now, however, oil is on its way out as renewable energy and battery storage have crossed the cost parity threshold - meaning it’s cheaper to make power (and vehicles) that don’t use oil. In its place, technology is the new cash cow, and tech is heavily represented in the ESG funds. The result:

As you can see, the performance has been similar but the ESG fund has done significantly better in the (admittedly short) time since it was introduced at Vanguard.

Of course, we have no idea if this will continue, but the point is that at least our thesis is not a ridiculous one - environmentally sustainable companies do have an advantage, if the world gradually starts to care more about these things. And if you look at the share price of Tesla and other companies that surround it in electric transportation and energy storage, you will see that there are many trillions of dollars already lining up to benefit from this transition. And the very presence of so much investment money creates a self-fulfilling prophecy, as Tesla is now building or expanding five of the world’s largest factories on three continents simultaneously.

So What Should You Do? (and what I do myself)

First of all, it helps to remember a fundamental piece of economics: your spending dollars will probably have a much bigger impact than your investment dollars. This is because you are sending a direct message to the world rather than an indirect one:

When you buy a new gasoline-powered Subaru (or a tank of gas for your existing guzzler) or a steak at the grocery store, or a plane ticket, you are telling those companies directly that consumers want more of these products, so they will produce more of them immediately.

When you buy shares in Exxon, you are only subtly raising the demand for those shares, which raises the average price, making it ever-so-slightly easier for Exxon to maybe issue more shares in the future. In other words, you are making it easier for them to access capital. But capital is only useful if there is demand for their products. And with oil there is a nearly constant surplus, which is why OPEC and other cartels need to work together to artificially restrict supply, just to keep prices up.

Plus, as a shareholder you are theoretically eligible to place votes and influence the future direction of companies - even companies that you don’t like. If you look up the field of “shareholder activism”, you’ll see this is a tradition that goes way back.

So I have tried to take a few simple steps on the consumer side myself, and I find it quite satisfying: Insulating the shit out of all of my properties, building a DIY solar electric array on one of them, and buying one electric car so far to eliminate local gas burning. And a few electric bikes including a super fast one I made myself.

Each one of these steps has provided a very high economic return, percentage-wise, but that still leaves a lot of money to account for, which brings us back to stock investing.

As someone who loves simplicity, I have done this:

- Bought almost entirely VTI (or similar Vanguard funds) from 2000-2015

- Started experimenting with Betterment in 2015, liked it, and have been adding a percentage of my ongoing savings to that account to that since then. (Note that Betterment now also offers a socially responsible portfolio option.)

- Switched the dividend re-investing of my old Vanguard VTI over to Vanguard ESGV, to avoid “wash sales” in making the most of Betterment’s tax loss harvesting feature.

- Bought some shares of Berkshire Hathaway separately, and also make a few sentimental investments in local businesses, including the MMM HQ Coworking space.

But you could choose to be more hardcore in your ESG/SRI investing:

- Buy your own basket of stocks based on the index, but with different weighting based on your own values

- Spend more money on other things that generate or save money (a bigger solar array on your house, better insulation, electric car, an ebike to reduce car trips, etc.)

- Invest in local businesses of your choice, rental real estate, community solar projects, or other things which generate passive income - publicly traded stocks are just one of many ways to fund an early retirement!

Like most areas of life, investing is not something you have to do perfectly in order to succeed - even socially responsible investing. If you apply the 80/20 rule to get the big picture right, you have probably found the Sweet Spot and you can move on to the next area of life to optimize.

In the Comments:

What is your own investment strategy? Have you thought at all about this ESG / SRI stuff? Did this article bring anything new to the table?

Given what we have seen in broad North American stock market indexes over the past six months, you could make the statement that COVID-19 doesn’t affect markets.

From the bottom in late March until recently, markets have risen steadily despite a backdrop of increasing global COVID cases. The explanation offered repeatedly along the way has been that the economy and the stock market are two different things. Besides, with lower interest rates investors would be foolish to bet against the Federal Reserve. On top of that, all of the significant government financial intervention would protect us from the worst impacts.

All of these comments are and have been true. I have said them myself and believe them. The question is can stock markets continue to rise when COVID-19 isn’t slowing down and may very well be getting worse? The answer is that it is increasingly unlikely.

Back in July, we hosted a webinar with an epidemiologist. At the time, they said it was “almost inevitable” that there would be a second wave of COVID-19. The rationale was threefold:

First, COVID-19 is an active virus with no vaccine or significant treatment, so it is unlikely to just “go away.”

Second, while a first wave saw new cases slow meaningfully, it wasn’t eliminated. Reopening happened while there were still new cases every day. This almost guarantees a second wave, as behaviours returned that increase the spread of COVID-19.

Third, the history of past pandemics shows that a second wave is almost always the case.

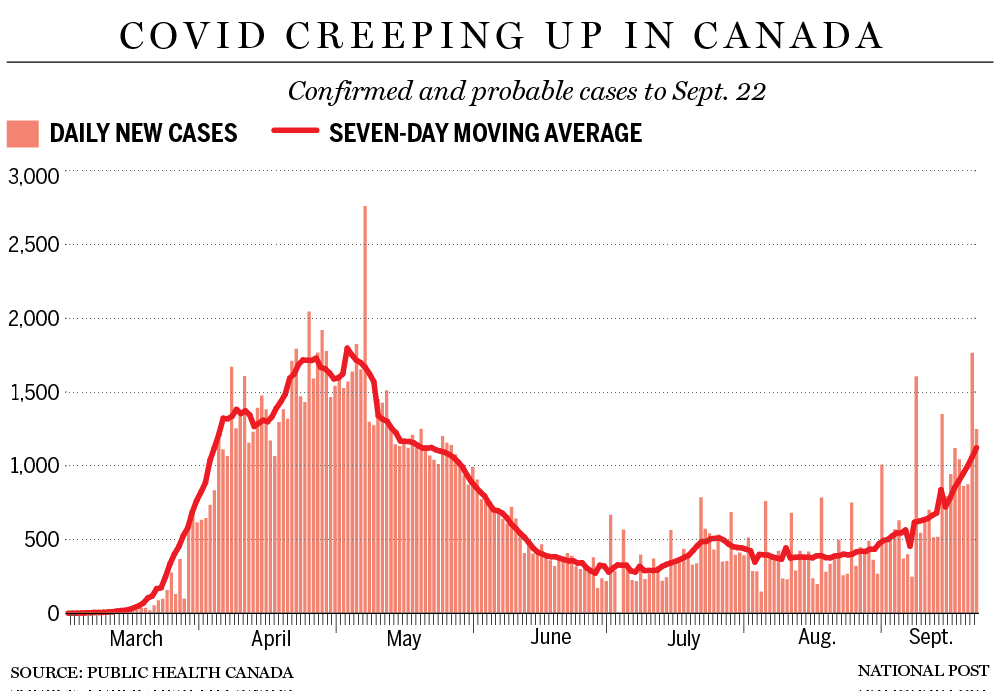

If we look globally, the number of new cases has continued to grow, with daily new cases regularly in the 250,000 to 300,000 range. Globally, there isn’t a second wave because the first wave never ended. Having said this, on a regional basis we are definitely seeing examples of second waves.

To get some sense of what we might face in Canada, it can be instructive to look at Europe, where numbers have meaningfully increased in the past month. If you look at Spain, they went from 10,000 new cases a day in March, to 400 new cases a day in June. Earlier this month they were back at 10,000 new cases a day. There can be no better definition of a second wave than those numbers. The good news is that the death rates have been much lower in this second wave (so far), with numbers 10 per cent to 20 per cent of what they were during the very dark days of March.

The policy response in Spain has been much more muted than the first time around. There is definitely a strong reluctance to shutting down the economy again. There is also a strong reluctance from some citizens and local governments to follow tough rules after going through such a hard time earlier in the year.

In Canada, the number of new COVID-19 cases has grown meaningfully this month. The chart is looking more and more like Spain, although we never had as many cases at the top. Hopefully death rates in Canada will remain much lower than at their peak. How will Canada react to this second wave? Time will tell, but based on our culture and reaction to date, there will probably be a little more willingness to accept tough measures from the government, and to shut some parts of the economy down if deemed necessary.

So what does this all mean for stock markets?

We still have exceptionally low interest rates, which have been a significant driver of strong stock markets. We still have major government spending (which seems to have no end in sight) to help backstop individuals and many companies as they deal with economic challenges. The one thing that we have today that is of concern is that stock markets are currently trading at very high historic valuations. This doesn’t leave you with a lot of room for error. A second wave of COVID-19 in major economic markets could certainly be cause for error. Global trade fights could be cause for error. U.S. political and social battles could be a cause for error. This all makes us cautious even after a dip in markets, like the one we saw on Monday.

When we talk about expensive or cheap stock market valuations, it is usually a form of price-earnings ratio. Essentially, this means that a company’s overall value is a multiple of its earnings or profitability. A more refined version called the Shiller P/E Ratio was developed by economist Robert Shiller.

Historically, a Shiller P/E ratio of 30 or higher has been a very expensive number. In times with very low interest rates, it would make sense that these numbers would get higher, but even over the past three years, this ratio has ranged between 25 and 33. It exceeded 32 at the beginning of September. At the same time, there is concern that corporate earnings growth cannot be maintained if we have more slowdowns caused by COVID-19 around the world. The Shiller P/E ratio is now back just under 30, but in this overall environment, we believe there is room for it to fall a little further.

After Monday’s sell-off, the U.S. tech-heavy Nasdaq was down 13.8 per cent from its level on Sept. 2. The broader-based S&P500 is down 10.6 per cent. The Dow Jones Industrial Average is down 8.2 per cent and the TSX is down 5.3 per cent.

We do not believe the declines are over. For markets to get back to where they were on June 1, the TSX would have to pull back another four per cent, while the Nasdaq would have to tumble another 11 per cent.

It is certainly possible that the declines don’t go that far, but we think there is a decent possibility that they will in the coming weeks. Indices are now back very close to the mid-July levels that we believed were expensive at that time.

As a firm, we do have some cash to invest at the moment, but we are now only dipping our toe in the pool in certain sectors. We are buying a little in utilities and consumer discretionary that we believe are cheap at these prices, but mostly staying on hold. Overall, we will likely be spending a meaningful amount of this cash between now and the end of the year, but mostly as we see some further declines.

We do see some good homes for cash in private credit investments that can take advantage of the high borrowing costs for corporations. Our focus for these investments is through the TriDelta Alternative Performance Fund, where we are aiming for returns in the eight per cent to 10 per cent range. Private credit investments have been quite solid throughout 2020.

We also see some opportunities in fixed-rate preferred shares, with Canadian dividend yields over five per cent and some price stability, and in gold as an alternative asset class given that cash is paying almost nothing and there are increasing concerns about the valuations and even stability of many major currencies.

As for stocks, we are getting a little closer, but mostly still keeping our powder dry.

Ted Rechtshaffen, MBA, CFP, CIM, is president and wealth adviser at TriDelta Financial, a boutique wealth management firm focusing on investment counselling and estate planning. You can contact Ted directly at

.

-

Business2 months ago

Business2 months agoBernice King, Ava DuVernay reflect on the legacy of John Lewis

-

World News2 months ago

Heavy rain threatens flood-weary Japan, Korean Peninsula

-

Technology2 months ago

Technology2 months agoEverything New On Netflix This Weekend: July 25, 2020

-

Finance4 months ago

Will Equal Weighted Index Funds Outperform Their Benchmark Indexes?

-

Marketing Strategies9 months ago

Top 20 Workers’ Compensation Law Blogs & Websites To Follow in 2020

-

World News8 months ago

World News8 months agoThe West Blames the Wuhan Coronavirus on China’s Love of Eating Wild Animals. The Truth Is More Complex

-

Economy11 months ago

Newsletter: Jobs, Consumers and Wages

-

Finance9 months ago

Finance9 months ago$95 Grocery Budget + Weekly Menu Plan for 8