Finance

Stocks, Bonds, and Gold: Historical Charts Since 1800

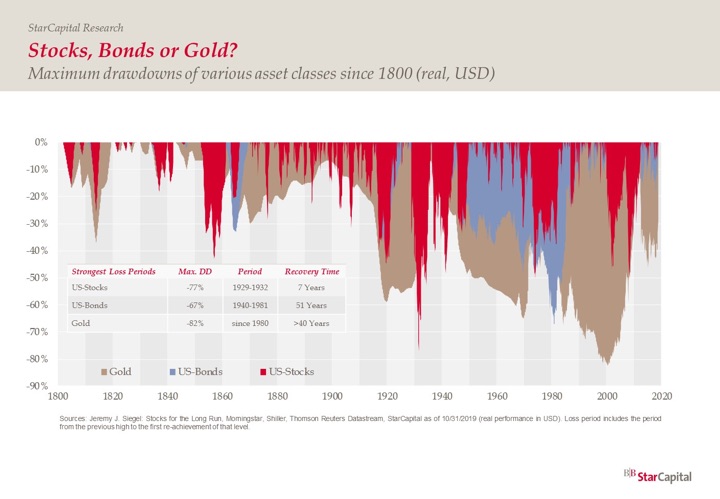

StarCapital Research has shared a series of interesting long-term charts comparing the long-term returns, drawdowns, and volatility of stocks, bonds, and gold over the last 220 years. There are also some stats on relative market valuations and forward return expectation for different countries and regions. You must accept some terms before viewing, but it is available to US individual investors.

Here is a sample chart of the return distributions of stocks, bonds, and gold since 1800, depending on holding period, along with their takeaway, via Norbert Keimling @CAPE_invest:

Conclusion: For periods of 10 years or more, stocks are safer than bonds or gold!

This is because for a 10-year holding, the worst inflation-adjusted performance of stocks (-5.9% annually) was better than the worst performance for bonds (-6.4%) and gold (-10.1%). The problem is that during a specific 10-year timeframe where stocks did that poorly, it’s quite likely that bonds or gold did great! Which means that it would still be quite difficult to keep holding stocks through such a period of poor performance. In a fearful environment, “sell stocks and wait things out” will start sounding like much wiser advice than “buy and hold”.

Of course, stocks can recover quite quickly and you might miss it while you’re waiting:

(There is also an ongoing debate about the validity of “time diversification”. Do stocks really become “safer” the longer you hold them? They can still go down 50% at any given time, so if you need to sell in the near future, they are never really safe.)

After doing this for a while, I don’t know if someone can simply read a book and “learn” how to keep the faith during the scary bits. It takes some time and making some mistakes to develop a portfolio where you understand its limitations and how long and how badly it can act in the short-term. I’m still learning.

“The editorial content here is not provided by any of the companies mentioned, and has not been reviewed, approved or otherwise endorsed by any of these entities. Opinions expressed here are the author’s alone. This email may contain links through which we are compensated when you click on or are approved for offers.”

Stocks, Bonds, and Gold: Historical Charts Since 1800 from My Money Blog.

Copyright © 2019 MyMoneyBlog.com. All Rights Reserved. Do not re-syndicate without permission.

Today, nearly all banks offer online banking. For many, the feature isn’t particularly well-developed. But in the past decade banks specializing in online banking have become more popular with each year.

The banks that are specializing in online, even providing their services on an online-only basis, are leading the pack into the future. Since there’s a real chance banks will eventually eliminate physical branches, it’s best to become comfortable with the all-online format now.

We’ve reviewed multiple banks in coming up with our list of the best online banks in the country. But the bank we feel comes out on top is Ally Bank. It’s an all-online bank – with no brick-and-mortar branch locations anywhere – but it offers full-service banking. That includes checking, savings, CDs, and auto loans. And if you want to invest where you bank, you can do it through Ally Invest.

The most important factor in choosing the best online bank is to find the one with the best features and services for you. For example, if you’re young, you may need to look for a bank that has no minimum initial deposit requirement, and charges no monthly fees. If you’re better established, you may be more interested in a bank that pays above-average interest on checking and savings. If you travel, an online bank with a large no-fee ATM network can save you a lot of money.

The Most Important Factors When Choosing an Online Bank

Working with an all-online bank is something of a learning experience if you’ve never done it before. For starters, you won’t have a local branch to go into with transactions and questions. It involves a large amount of self-directed activity, which is why you’ll need to work with an online bank that provides the tools and benefits that will allow you to bank independently.

In coming up with this list, we used the following criteria to determine the best online banks in the country:

- Number and type of accounts offered: This should include checking at a minimum, but also high-interest savings and even CDs.

- Secondary services: These can include related products, like auto loans, credit cards, business banking, investments, and financial management. Each of the banks listed below specialize in at least one of these categories.

- ATM network: ATM access is important with any bank, but it’s especially important with online banks, precisely because they have no local branches.

- Minimum initial deposit requirements: Any bank is more consumer-friendly when it has either a low minimum initial deposit requirement, or better yet, none at all.

- Low fees: Because they don’t have a network of bank branches to maintain, online banks typically charge lower fees than banks with branches. If you’re going to give up the branch advantage, you should be compensated in the form of lower banking fees.

- High interest: Same situation here. Absent the branch network, online banks generally pay much higher interest rates than traditional brick-and-mortar banks. Many online banks pay interest on deposit accounts that 20 times or more what traditional banks pay.

In compiling our list of the best online banks in the country, we specifically looked for banks that meet the above criteria.

Our Picks for The Best Online Banks

It can be difficult to declare one bank as the overall best online bank in the country. But there are many excellent online banks that specialize in very specific niches. We’ve included five of what we believe to be the best online banks in the country, and below is a list of what we believe each is best for:

Ally Bank Review

Ally Bank has grown to become one of the most popular online banks there is. What makes it almost unique among online banks is that it offers virtually full-service banking. Ally Bank offers checking and savings accounts, as well as certificates of deposit. And as the successor company to General Motors Acceptance Corporation, Ally Bank provides some of the most innovative auto financing programs in the industry, including leasing of used vehicles.

It’s no wonder the Bank appears on both our Best Online Savings Accounts and Best Online Checking Accounts lists! And if that’s not enough, you can also hold your investments where you bank. Ally Invest is part of the Ally Family, and provides commission-free trades on stocks, options, and exchange traded funds. But they also provide a robo-advisor option, if you prefer low-cost professional investment management of your portfolio.

Why it made the list

- Ally Interest Checking offers fee-free banking, with some of the highest interest rates being paid on checking accounts. The account is currently paying 0.50% APY on all balances

- You’ll have access to more than 43,000 fee-free in-network ATM machines. Up to $10 reimbursed on out-of-network ATM fees per statement cycle.

- No minimum opening deposit required.

- Ally Bank Online Savings Account currently pays 1.10% APY on all account balances.

- Ally Bank CDs earn among the highest interest rates in the industry, with rates up to 1.15% APY.

- Commission-free trading with Ally Invest.

What holds it back

- Though it’s not unusual for online banks, there’s no ability to deposit cash into your account.

- You’ll be charged a fee of $10 for every outgoing transfer from your savings account after the first six.

Chime Review

Chime is an online, mobile only bank. It’s specifically designed for those who cannot get a traditional bank account due to either poor credit history or a negative banking experience in the past. For example, if you’ve ever closed out a checking account with a negative balance – and not paid off that balance – the bank will report the overage to what is known as ChexSystems. It’s something of a credit repository for banks, providing them with your experience in previous banking relationships.

Chime can help you if you’re in this situation, because they don’t run a check through ChexSystems, nor do they run a credit report. You can open an account regardless of your past history.

When you open an account with Chime, you’ll have a Spending Account – which is your checking account – a savings account, and a debit card. The combination will enable you to fully participate in a banking relationship, even if you aren’t qualified to open a traditional account with another bank.

Why it made the list

- Chime does not check your credit or the ChexSystem for account eligibility, making it the perfect choice if you’ve been unable to open a bank account due to either poor credit or a previous negative banking relationship.

- “Roundups” on debit card transactions enable you to save money passively.

- No minimum initial deposit or balance requirement, you can open an account with no money at all.

- No monthly maintenance fees, and no overdraft fees.

- No foreign transaction fees.

- Available to consumers nationwide.

- Access 38,000 no-fee in-network ATM machines.

What holds it back

- Difficult to make cash deposits into your account.

- Chime pays interest on your account that’s no better than the national average.

- Chime charges a fee of $2.50 when you use out-of-network ATM machines.

- Limited customer service.

Radius Bank Review

Radius Bank is one of the new wave of fintech banks operating almost entirely online. I say almost, because they do have a handful of branches in the Boston area where the bank’s based. Radius Bank has designed its banking services specifically for younger users, who are mainly concerned with better managing their spending and even earning spending related rewards.

Radius Bank offers business and personal checking accounts, high-yield savings, and certificates of deposit. Credit cards are made available through partnerships with third-party sources, and the bank does not provide personal loans.

Why it made the list

- A minimum opening balance of just $100 is required, with no minimum balance required thereafter.

- There are no monthly fees on Radius Bank Rewards Checking Accounts.

- The Rewards Checking Account pays interest and unlimited 1% cash back on purchases.

- Offers its Essential Checking Account as a second chance checking account for anyone who may not be able to get a traditional bank account based on a previous less-than-satisfactory banking experience.

- Offers its Tailored Checking Account for small businesses, including freelancers and gig workers.

- Offers commercial banking, which includes business lending, cash management, merchant services, ePayment solutions, payroll services, sweep accounts, and four different checking accounts. The bank does participate in SBA lending and the Paycheck Protection Program.

- Participates in an ATM network with more than 325,000 outlets.

- Unlimited rebates for ATM fees charged by other banks.

- Offers a Refer-a-friend program paying both you and the person you refer $50 if they open a Rewards Checking Account.

What holds it back

- Radius Bank has a fairly limited product menu as banks go, since it’s tailored toward the upstart market.

- Interest rates on deposit products, while better than the national average, are not among the highest in the industry.

- No interest is paid on account balances below $2,500.

- Radius Bank doesn’t make personal loans, and credit cards are offered through partner service providers.

Empower Finance Review

Empower Finance isn’t an online bank, but a financial app available with your smartphone, that will enable you to track your finances, reduce your expenses, and find ways to save money in your pocket. It can even help you track your credit usage. You can think of it as something like a mobile app version of Personal Capital.

However, it does provide an interest-bearing checking account and debit card through NBKC Bank, currently paying 0.25% APY on all balances and no account minimums. You’ll also receive three monthly ATM fee reimbursements. Even better, there are no overdraft fees, and foreign transaction fees just 1%.

Meanwhile, the app aggregates all your financial accounts in one place. That includes bank accounts, loans, credit cards, and retirement accounts, including employer-sponsored plans like your 401(k). It will categorize your spending to help you track exactly where your money’s going using custom reports.

The Spending Tracker tool acts as a built-in budgeting system. It allows you to set limits on spending categories and get better control of exactly where your money goes. You can set the tracker to provide you with alerts anytime you’re going over budget in any spending category. It will also alert you about upcoming bills. An Automated Savings Deposit tool can transfer money into your savings account, but it does it with a twist. You can set a periodic savings goal, and Empower will analyze your cash flow, automatically saving money when you have extra funds.

But what may be most interesting about the Empower Finance app is the Empower Assistant Tool. It will analyze your accounts for potential savings, and where necessary, negotiate your bills. That may include switching to a less expensive cable and Internet plan, or even mobile phone plan. The tool can also cancel unwanted subscriptions.

Oh, and one more feature: you’ll have access to a Human Coach. That will provide personalized coaching for any financial challenge you’re facing.

Why it made the list

- Financial app that enables you to both manage and improve your finances.

- The app is free to use for the first 30 days.

- Provides tools to save money,negotiate bills and save you additional money.

- The Credit Tracker will help you keep track of how much you’re spending on credit. That can be a valuable tool if you want to lower your credit utilization ratio to improve your credit score.

- Interest-bearing checking account currently paying 0.25% APY on all balances, with no minimum balance requirements.

- Automated savings transfers.

- Access to a Human Coach to help you with financial questions.

What holds it back

- Empower Finance is mostly a financial app, but it comes with a checking account (no savings or other banking services).

- After the 30-day free trial period, there is a $6 monthly fee to use the app.

Capital One Review

Capital One is another top online bank, also making both our Best Online Savings Accounts and Best Online Checking Accounts lists. But Capital One is unique to other online banks on this list, in that they actually have physical bank branches in many locations. In fact, they have over 750 in total. In addition to offering top-of-the-line checking, savings, and CDs, Capital One also has one of the most popular lineups of credit cards in the industry.

At the core of Capital One banking are the Capital One 360 accounts. They’re available in both checking and savings.

360 Checking comes with no fees and no account minimums. You’ll also have access to more than 40,000 fee-free ATM machines across the country. And the account is currently paying 0.10% APY on all account balances.

360 Performance Savings similarly has no account minimums and no monthly fees. They’re currently paying 1.00% APY on all account balances.

Why it made the list

- Capital One has no minimum deposit requirements and charges no fees on their primary checking and savings accounts.

- The bank has more than 750 branch locations, in addition to operating as an all-online bank.

- Customer service is available 24 hours a day, seven days per week.

- The Bank pays interest rates well above average on its checking and savings accounts.

- Access to more than 40,000 fee-free ATM machines across the country.

- Capital One provides some of the most attractive credit card offers in the industry.

What holds it back

- While Capital One pays interest rates well above industry averages, they’re not the highest available.

- Though they have branches available, the network isn’t as comprehensive as many of the large regional and national banks.

What You Need to Know About Online Banking

To take best advantage of the many benefits provided by online banks, like high interest rates and low or no fees, you’ll need to be prepared for the following:

No bank branches: Online banking will work best for you if you rarely or never go into a bank branch. If the opposite is true, you should maintain an account with a bank that has branches.

You need to be at least somewhat Internet savvy: You must be comfortable working on an online platform. You’ll need to be able to navigate a website and run transactions, like online bill payments and transfers, with little or no help from the bank.

You’ll need a smartphone and a good Internet connection: Access to your account will depend on one or the other, preferably both. If you live in an area where the Internet connection and Wi-Fi are limited or weak, online banking may not work for you.

Determine the level of customer service you need: To keep expenses to a minimum, online banks not only work without branches, but often with limited personnel. If you need frequent access to customer service, work with an online bank that has 24/7 customer service.

Online banks are often highly specialized: One bank may specialize in no-fee checking, while another may pay very high interest on savings. It’s possible you’ll need relationships with more than one online bank to take advantage of all they have to offer.

The ATM network is even more important: Since you won’t have the benefit of physical bank branches, you’ll need reliable access to an extensive no-fee ATM network. The no-fee factor will be even more important if you frequently make cash withdrawals.

Most online banks are not suitable to business banking: Online banking is evolving quickly. But only a handful of online banks offer business banking. Radius Bank is one that does and that’s one of the reasons we included it on our list of the best online banks in the country.

Before choosing an online bank, carefully evaluate your banking preferences and routines, and choose the bank that will work best for you.

Summary: The Best Online Banks in the Country

| Bank | Best For… | Accounts Offered | Interest Paid On… | No Fees On… | ATM Network |

| Ally Bank | Full service banking and best all-around | Checking, savings, CDs, investing | Checking, savings, CDs | Checking and savings | 43,000+ |

| Chime | Consumers who don’t qualify for traditional bank accounts | Checking and savings | N/A | Checking and savings | 38,000+ |

| Radius Bank | Younger consumers and business banking | Checking, savings, CDs, business accounts | Savings and CDs, plus 1% cash back on purchases through checking | Checking and savings | 325,000+ |

| Empower Financial | Personal finance management | Checking account | Checking account | Checking account | Out-of-network only |

| Capital One | Online banking with physical bank branches | Checking, savings, CDs | Checking, savings, CDs | Checking and savings | 40,000+ |

The post The Best Online Banks in the Country appeared first on Good Financial Cents®.

If you’ve been looking to join a credit union instead of a bank or want to add a credit union account for your checking and savings, PenFed is worth checking out.

While they don’t have the highest checking and savings APYs, they are reasonable and competitive for a full-service credit union. In fact, PenFed made our list of the top 5 credit unions nationwide of 2020.

PenFed’s mobile app allows you to do all of your banking online or on the go through their mobile app, no matter where you are in the U.S. and even some locations outside of the U.S. In this article, we’ll review PenFed’s checking and savings products.

Quick Summary

- Competive interest rates

- Large nationwide ATM network

- Minimum balance required to avoid checking account fees

|

PenFed Checking And Savings Details |

|

|---|---|

|

Product Name |

PenFed Credit Union |

|

Account Types |

Checking, Savings, Money Market, Certificates |

|

APY |

0.05% to 0.90% APY |

|

Min Deposit |

$5 |

|

Promotions |

None |

Who Is PenFed?

Pentagon Federal Credit Union is a full-service credit union. They were created in 1935 and have $25 billion in assets. PenFed is headquartered in McLean, Virginia. They used to restrict membership to a relationship with the military or federal government but have recently opened up to everyone.

PenFed services all 50 states, including the District of Columbia, Guam, Puerto Rico, and Okinawa (Japan). They are federally insured by NCUA and are an Equal Opportunity Lender. In addition to PenFed checking and savings accounts, members can also access home, car, credit card, and student loan products.

See our review of PendFed’s student loan refinancing product.

What Do They Offer?

PenFed has one checking account and four savings products. They have a network of 68,000+ ATMs. You can bank online or through their mobile app. PenFed has nearly 50 branches across 16 states and the District of Columbia, Guam, Puerto Rico, and Okinawa.

The PenFed website shows its accounts earn interest (APY) and dividends. The terminology can make it sound as though you get the APY plus dividends. That isn’t the case. Dividends are simply being used interchangeably with interest (APY).

Access America Checking Account

You’ll need to deposit $25 to open a checking account with PenFed. PenFed checking accounts do earn a little interest — 0.20% to 0.50% depending on account size as shown below.

- 0.20% APY on a daily balance of less than $20K

- 0.50% APY on a daily balance of $20K or more up to $50K

In addition to the listed APYs, you can also earn dividends with a monthly direct deposit of $500 or more. As well, to avoid the $10 monthly fee, you’ll need a daily balance or monthly direct deposit of $500 or more. Overdraft protection is available but is subject to approval.

Premium Online Savings Account

The Premium Online Savings Account pays 0.90% APY on balances up to $250,000 and only requires a $5 deposit. There are no monthly fees. However, there also is no ATM access.

Be aware that savings accounts have more restrictions than checking accounts. Due to federal law, you can only withdraw money from your account up to six times per month. You’re allowed up to $10,000 per day in deposits and a total of $50,000 for the month.

Regular Savings Account

The Regular Savings Account pays only 0.05% APY on all balances. But in exchange for giving up that interest, you gain ATM access. However, if you can get by with transferring money to your checking account before making a withdrawal, the Premium Savings Account is clearly the way to go.

Money Market Savings Account

The Money Market Savings Account requires $25 to open and doesn’t lose ATM access. There are no monthly fees and you get free checks upon request. The account pays interest through several tiers that are dependent on your balance:

- 0.05% APY — $10,000 or less

- 0.10% APY — between $10,000 and $99,999

- 0.15% APY — $100,000 or more

See how this compares to the top money market accounts here >>

Money Market Certificates

You’ve probably heard of a certificate of deposit (CD). Credit unions call these simply “certificates,” but they are basically the same.

PenFed has several certificates to choose from. All require a $1,000 deposit to open. Just like a CD, your money must remain in the certificate until maturity or you’ll pay an early withdrawal penalty. Dividends are compounded daily and paid monthly.

The following certificates are available:

- 6 Month — 0.40%

- 12 Month — 0.70%

- 15 Month — 0.70%

- 18 Month — 0.70%

- 2 Year — 0.75%

- 3 Year — 0.80%

- 4 Year — 0.85%

- 5 Year — 1.00%

- 7 Year — 1.05%

Mobile App

The mobile app for PenFed checking and savings includes all of the features you’d expect from full-service credit unions. You get instant check deposits, bill pay, ability to send money to almost anyone, account management, and the ability to transfer funds between your PenFed accounts.

Are There Any Fees?

The majority of PenFed’s accounts don’t come with fees. However, its Access America Checking Account has a $10 month fee if certain minimums are not met. To avoid the fee, you’ll need to keep a minimum balance of $500 or set up a $500 monthly direct deposit.

How Do I Open An Account?

You can visit Penfed.org or a local branch if you have one near you to apply for membership. If approved, you’ll need to deposit at least $5 to open an account.

Is My Money Safe?

Yes, money deposited with PenFed is federally insured by the NCUA. Like FDIC insurance for banks, NCAU insurance protects up to $250,000 of credit union member deposits per account.

Is It Worth It?

If you’re looking to open a checking or savings account with a credit union, PenFed is a full-service credit union that pays up to 0.50% on checking account deposits and up to 1.00% on savings. It has about 50 branches in 13 states, plus a few outside of the U.S. and includes NCUA protection. For those reasons, PenFed checking and savings is certainly worth considering.

But if you won’t be able to meet the requirements for waiving PenFed’s monthly checking account fees, you might want to look at these free checking accounts instead. And if you’re comfortable with managing your checking or savings accounts with minimal support, you might be able to earn higher rates with an online bank. These are our favorite online banks for 2020.

PenFed Checking And Savings Features

|

Account Types |

Checking, Savings, Money Market, Certificates |

|

Minimum Deposit |

|

|

APY |

Checking:

Regular Savings: 0.05% APY Premium Online Savings: 1.00% APY Money Market Savings

Certificates

|

|

Maintenance Fees |

|

|

Branches |

~50 across 13 states |

|

ATM Availability |

68,000+ fee-free ATM network |

|

Customer Service Number |

1-800-247-5626 |

|

Customer Service Hours |

|

|

Mobile App Availability |

iOS and Android |

|

Bill Pay |

Yes |

|

NCUA Charter Number |

00227 |

|

Promotions |

None |

The post PenFed Checking And Savings Review: Full Service And Solid Rates appeared first on The College Investor.

“Success can get you to the top of a beautiful cliff,

but then propel you right over the edge of it.”

As a Mustachian, there’s a good chance that you are a bit of an overachiever.

Maybe you fought hard to get exceptional grades in school, or perhaps you have always dominated in your career or your Ultramarathon habit or your hobbies - or maybe all of the above.

In the big picture, this usually leads to having a “successful” life, because of this basic math:

Traditional Success

=

How much work you do

x

How much society happens to value your work

The Nitty Gritty of Traditional Success

Now, lest the Internet Privilege Police head straight to Twitter to start writing out citations, Traditional Success is not a measure of your worthiness as a human being. We’re just talking about the old-fashioned, Smiling 1950s Man definition of success.

And since we’re all scientists here, we could break the “Work” side of it down a bit further:

And thus, you could say that on average, doing more stuff produces more traditional success.

But then what?

This is the point where a lot of smart, driven, born-lucky people drive themselves up the Winding Road of Challenge and then right off the edge of the Cliff of Success.

If you’re still on the way up, or stuck at the bottom, it is difficult to even imagine the idea of “too much success”. But it’s a real thing, and it happens much more quickly than the modern overachiever would like to admit. Observe the following cautionary tale:

Diana is the director of engineering in a Silicon Valley tech startup. The work is intense, but they are almost over the hump - the company went public last month, and she owns shares that are worth over $10 million at today’s share price. They will vest over the next five years, so she just needs to grind this out and then she will be set for life.

Sounds great, right?

Except this is Diana’s third smashing success. She was already set for life after the second company was acquired, and even before that, her first decade as a rising star at a large company had already left her with over $2 million of investments and a paid-off house in hella expensive Cupertino, California. She had more than enough to retire, twenty years ago!

To many people who are less fortunate, the present situation would still sound like great fortune, and in some ways, it is. Becoming a Director of Engineering is (usually) far better than a punch in the face.

But Diana is now 52 years old, with a collection of increasingly severe back and neck problems and a few medical prescriptions piling up. She has two grown children in their twenties, but wishes she had been able to spend more time with them as they grew up. She has all the money in the world, but still almost no free time, and this next five years is starting to look like an eternity.

What happened here?

Diana is in good company, because many of our hardest-working people fall into this same trap. They have the talent and the great work habits figured out, but they are still missing one last concept - the idea of the sweet spot.

Diana could have stopped after the first company, or the second, but her career success took on a momentum of its own, so she kept doubling down without stopping to consider why she was doing it - and what she was giving up in exchange.

Once you learn to see the phenomenon of the sweet spot, you will start noticing it everywhere. And it is an amazingly useful thing to start watching and fine-tuning to get the most out of your own life.

Fig.2: What is the ideal amount of Anything?

The Sweet Spot of Physical Training

When a non-runner starts running, they will see immediate benefits. In the process of going from being unable to jog across a parking lot, to being able to easily jog a brisk mile, your entire body will transform for the better. Muscles and bones get stronger, heart and lungs expand and reach out to give your body a healthy embrace, brain functioning and mood and hormones smooth out and normalize.

When a non-runner starts running, they will see immediate benefits. In the process of going from being unable to jog across a parking lot, to being able to easily jog a brisk mile, your entire body will transform for the better. Muscles and bones get stronger, heart and lungs expand and reach out to give your body a healthy embrace, brain functioning and mood and hormones smooth out and normalize.

Training your way up to become a two mile runner still brings great benefits - just slightly smaller. The fifth through twentieth mile turn you into a hyper efficient machine, but some people start seeing joint injuries as they rise through the ranks.

And by the time you reach the fringe world of 100-mile runners, serious injuries and surgeries are completely normal - as well as unexpected organ failures in otherwise young, healthy people. The sweet spot for daily running for maximum health is somewhere the middle.

All around us, seemingly unrelated things follow this same pattern, from career work to physical exertion to parenting strategy.

Fame and Fortune - be careful what you wish for

Fame definitely has a sweet spot. Building up a good reputation in your community can open the door to better friendships, jobs, relationships, and more fun in general.

But as that reputation expands outwards to become fame, you get the “reward” of constant coverage in gossip magazines and waking up to find photographers and news reporters on your front lawn. At the extreme end, you need to mobilize a team of armored vehicles and line your route with snipers every time you leave your well-guarded compound.

Even money, our humble and ever-willing servant is subject to this phenomenon. It certainly helps us meet our basic needs, but there is a certain point at which Mo Money can become Mo Problems.

The first bit of monetary surplus can be fun as you can afford a nice house and good food. Then the next chunk seems fun but also causes distractions as you rack up second and third houses and ever-more elaborate possessions and vacations that take a lot of energy to keep track of.

And from there it goes downhill as tabloids start keeping track of your wealth and scrutinizing your choices, hundreds of people mail in pleas for your generosity, and you end up with a full-time job just making sure that the surplus goes to good use. This life arrangement can still be enjoyable for some people, but I would definitely not wish it upon myself.

On and on this pattern goes. A curve with a sweet spot in the middle. The optimal amount of calories to consume in a day. The volume at which you will enjoy your music most. The right brightness of light to illuminate a room. The number of friends with whom you can have a meaningful relationship.

Why does it occur in so many places? I believe it is because this is how our brains are wired in the first place.

Humans are a ridiculously adaptable creature, but we do still come with limits.

And when you respect those limits and fine-tune your life within the sweet spot for all of the main pillars for happy living, you end up with the best possible chance at living a happy, prosperous life.

Interest rates are still at WTF-low levels, so if you haven’t already done so, I recommend checking your current home mortgage and student loan rates. Either at your local credit union, or online via a service like Credible.

Click Here to open that up in a new tab, and keep reading.

Note: This is an affiliate link, to learn why I use these even when I am supposedly retired, read this.

The Curse Of the Overachievers - Revisited

So now you see the problem - overachievers like us tend to get really good at a few things like a career or an athletic pursuit often specializing so much that we neglect other things like overall health or personal relationships.

And our society notices and rewards us for the success, which just reinforces the behavior, so we take things to even higher extremes, often without stopping to think about the reason behind it.

Okay, So What Now?

Once you see the pattern of the sweet spot, it is impossible to un-see it. So it becomes pretty easy to float up and look at your entire life from above, like an outside observer.

And from up there, you can see the areas where you have enough, and places where you may have already gone overboard, and the corresponding things that you have left neglected as the price of that success.

Over the past year I’ve been looking at my own life from this perspective, coming up with quite a few of my own diagnoses:

Money: enough. Additional windfalls don’t seem to bring me any lasting joy, but I also don’t have so much money that it makes me nervous. It’s enough to feel safe and empowered, and that’s all I need. Meanwhile, giving away money has brought me lasting happiness, without creating a feeling of shortage or regret.

Career Success (blog): It Varies. When I was really working on this MMM job in the mid-2010s, it started to take over too much of my life. Emails, opportunities, travel and public attention all reached levels where I actually started to have less fun. So I tried dialing it back, as any long-term readers will have noticed. And sure enough, life improved. But then I went too far and started feeling a loss from letting this valued hobby slip away. I’ve been trying to get back into the groove, which revealed another problem - detailed at the end of this list.

Friendships: Not Enough. I have found myself not being able to keep up with close friends, and had difficulty making or keeping plans, partly out of feeling overwhelmed with life details in general. Still, the opportunities abound here in my local community, and the people are wonderful. So I have the opportunity to keep working at this.

Health and Fitness: Enough. Since I was about fourteen years old, eating well and getting a lot of varied exercise has always been a kind of non-negotiable pillar for me. Nothing extreme, but just very consistent. I think this has been paying off as I feel healthy every day and have never had any physical or health problems in these 30+ years since.

Parenting and Kids: Enough (an A+!) Since 2005 I made “being a Dad” my primary goal in life, quitting my career to do so. It’s the only thing I can truly say I have done the best I could at, and I’m really proud of that. But part of this success came from only having one kid - both of us parents knew we couldn’t handle any more, given the overall conditions of life back then. So for us, the sweet spot was One Child - and absolutely no regrets in that department.

Personal Projects and Daily Habits: Not Enough. I get great satisfaction from working on challenging things and making progress. But far too often, I just can’t get it together and I squander entire days on accidental distractions. Planning to go out for a day of work can lead to searching for lost sunglasses which can lead to finding a lost to-do list which can lead to opening the computer to look something up and several hours disappearing. On and on these tangents can go, often leading to me not getting my primary, happiness-creating goals for the day accomplished.

I discovered that I have a pretty severe and textbook case of Adult Attention Deficit Disorder, which gets magnified if there are any sources of stress in my life. So I’m working on that (keeping stress down and also targeting habits, diet, exercise and even trying some medication), which will hopefully improve all other areas of life as well.

What am I missing? I’m still working on thinking it all through, so this list will surely grow.

Your Turn

Your life surely has a completely different array of surpluses, shortages and sweet spots than mine. Your assignment is therefore to write them all out tonight, and see where you stand in each area, and decide what to change. Many of the changes are quite easy to make, and yet the results are nothing short of life-changing.

In the comments: what are your own areas of surplus and shortage? And what’s your plan to help restore balance to your life?

-

Business3 weeks ago

Business3 weeks agoBernice King, Ava DuVernay reflect on the legacy of John Lewis

-

World News3 weeks ago

Heavy rain threatens flood-weary Japan, Korean Peninsula

-

Technology2 weeks ago

Technology2 weeks agoEverything New On Netflix This Weekend: July 25, 2020

-

Finance3 months ago

Will Equal Weighted Index Funds Outperform Their Benchmark Indexes?

-

Marketing Strategies7 months ago

Top 20 Workers’ Compensation Law Blogs & Websites To Follow in 2020

-

World News7 months ago

World News7 months agoThe West Blames the Wuhan Coronavirus on China’s Love of Eating Wild Animals. The Truth Is More Complex

-

Economy9 months ago

Newsletter: Jobs, Consumers and Wages

-

Finance8 months ago

Finance8 months ago$95 Grocery Budget + Weekly Menu Plan for 8